Blog

Season's Greetings, Happy New Year 2023

Season's Greetings, Happy New Year 2023

Happy New Year

Stay awesome in the coming year.

May many fortunes find their way to you.

May the joy and happiness around you today and always

May the new year bless you with health, wealth and happiness

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

最新劳工法令

最新劳工法令, 明年1月1日落实

马来西亚劳工法令条规,你了解多少?

观看视频 #rojaklah https://vt.tiktok.com/ZS8jsaUaL/

阅读英文版 from 我们的 KTP 博客 blog

https://www.ktp.com.my/.../key-amendments-to.../11sept2022

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Insolvency Test for A Company

Insolvency Test for A Company

In terms of the “solvency test”, solvency relates to the assets of the company, which are fairly valued, equal or exceed the liabilities of the company.

What does it mean to be insolvent?

It is a state of financial distress where a company is unable to pay its bills.

What are the warning signs of insolvent companies?

-

Inability to pay your debts.

-

Poor profitability.

-

No access to finance.

-

Unpaid creditors beyond normal credit terms.

-

Unable to raise further equity funding.

What is the company insolvency test?

-

Cash flow test

-

Ratio test

The purpose is to analyze:

-

Existing debt of company

-

The dates any company income will be received

-

The date each debt will be due for payment

-

The company’s present and expected cash resources

-

Whether the company’s debts are payable in the near future

Ratio Insolvency Test

Quick Ratio = Projected Cash + Account Receivable / Current Liabilities

Reveal the reliability of the company’s repayment of short-term debts with current assets and inventory.

Solvency ratio = Projected Net Profit + Depreciation / Current Liabilities

It is to measures the ability of a company to meet its short-term debts.

Current ratio = Projected Current Assets / Current Liabilities

It is commonly used as a quantification of short-term solvency and give a sense of the efficiency of a company’s operating cycle or its ability to turn its product into cash.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Personal Tax Relief 2022

Personal Tax Relief 2022

Overview

Year 2022 is approaching to its end and now is the time for you to keep and plan on your personal tax.

Do you know what personal deduction can be claimed for year 2022?

With that, here’s the full list of tax reliefs for YA 2022.

Key takeaways:

You will know the Tax Relief and consequences for non-compliance as follows:

1. What types of Personal Tax Relief for YA 2022?

2. What types of donation allowed for deduction?

3. What types of documents are required to be kept?

4. How many years to keep the documents?

5. What are the consequences of non-keeping proper records?

Summary of learning

1. What types of Personal Tax Relief for YA 2022?

- Please refer to the link https://bit.ly/3R1Y6fU to get the full listing.

2. What types of donation allowed for deduction?

-

Gift of money to the Government/ approved institutions;

-

Contribution in fighting against the COVID-19 pandemic; or

-

Gift of money / cost / value of gift of medical equipment to any healthcare facility approved by the Ministry of Health or etc

-

For full information on tax allowable donation for deduction, please refer to the link https://bit.ly/3R1Y6fU.

3. What types of documents are required to be kept?

Receipts and supporting documents for the tax deduction claimed must be kept for future reference and inspection if required from LHDNM.

4. How many years to keep documents?

Must be kept for a period of seven (7) years after the end of the year in which the return form is furnished to LHDNM.

5. What are the consequences of non-keeping proper records?

A RM300.00 – RM10,000.00 fine or imprisonment for a term not exceeding twelve months of both.

Source

a) Public Ruling No. 5/2021 – Taxation of A Resident Individual Part I - Gifts Or Contributions And Allowable Deductions

https://phl.hasil.gov.my/pdf/pdfam/PR_05_2021.pdf

b) Public Ruling No. 5/2000 – Keeping Sufficient Records for Individuals & Partnerships

https://phl.hasil.gov.my/pdf/pdfam/PR5_2000_Rev.pdf

c) Public Ruling No. 6/2000 – Keeping Sufficient Records for Persons Other Than Companies Or Individuals

https://phl.hasil.gov.my/pdf/pdfam/PR6_2000_Rev.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

What is Use of Right Assets in Accounting?

What is Use of Right Assets in Accounting?

Background

MFRS 117 introduces the treatment of both finance lease and operating lease, but operating lease is treated as an off-balance sheet lease.

MFRS 16 superseded MFRS 117 and introduced the “right to use” approach, which requires lessee to recognize the rights and obligations arising from the lease arrangement in the balance sheet with the effect from 01.01.2019 in order to standardize the treatment for both finance and operating lease.

Definition of Right-of-Use Asset - MFRS 16

-

Lessee has the rights to control the use of an identified asset for a period of time. [Para 9]

-

Lessee able to obtain all of the economic benefits generated from the use of assets. [Para 9]

-

Lessee able to decide how and for what purpose the asset is used [Para 9]

-

Lessee has the obligation to make payment for the identified asset [Para 9]

-

Risk and reward of the ownership for the asset is still mainly retained with the lessor. [Para 65]

Exemption of MFRS 16 – Para B6

-

Short term lease (Less than 12 months) and contain no purchase option.

-

Lease for asset with a low value when new

Initial measurement:

(i) Cost of the right of use asset should include [Para 24]:

-

Lease liability

-

Prepayment of lease payment – lease incentives

-

Initial direct costs

-

Dismantling costs

(ii) Lease liability [Para 26]:

-

Present value of lease payments

Subsequent measurement:

(i) Right of use assets [Para 30]

-

Cost – accumulated depreciation – accumulated impairment loss

(ii) Lease liability [Para 36]

-

Recognise lease interest and payment

Tax implications:

Lessee:

-

Not entitled to claim the capital allowance on the leased assets [Public Ruling No. 5/2014 - Para 11.3]

-

Depreciation charged is non-tax deductible

-

Interest expenses is tax deductible if fulfilled the condition of Section 33 (1) of Income Tax Act 1967

Sources:

-

MFRS 16

-

Section 33 (1) of Income Tax Act 1967

-

Public Ruling No. 5/2014

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Book-keeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource book-keeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

SSM Heavy Fines on Company, Sole Proprietor and Partnership

SSM Heavy Fines on Company, Sole Proprietor and Partnership

Update any changes in company information promptly

Recently we came across an interesting press release published by SSM on 26 October 2022 where the Registrar of Business (ROB) imposed a fine of RM4,000 on the owner of a sole proprietor as a result of giving a false business address.

This serves as a reminder to the public that prosecution will be taken against any person who is found to have given false or misleading statements and information to SSM. SSM is always consistent in regulating compliance with the law and ensuring the corporate community is aware of its responsibility and business ethics.

In this newsletter, we would like to emphasize and spread awareness to our client and the public that it is important to update the business or company’s particular promptly once there are any changes in the details.

Why it is important?

To avoid any heavy penalty imposed by SSM.

Accordingly to the following act governed under SSM, it is a requirement for the business owner or company’s directors to update any changes in the particular such as a change in residential address, or renewal passport number for foreign director and shareholder.

-

ROB Act, 1956 – Section 5B

-

Companies Act (CA), 2016 – Division 8 Registered Office and Registers - Section 51 and 58

When need to notify on the changes?

-

ROB - within 30 days from the date of changes

-

ROC - within 14 days from the date changes.

What are the penalty and fines if failure to comply?

a) Late filing fees are applicable as follows:

Private company:

- Not more than 3 months – RM 50.00

- More than 3 months but not more than 6 months – RM100.00

- More than 6 months but not more than 12 months – RM150.00

- More than 12 months – RM200.00

b) Compound upon conviction

ROB - not exceeding RM10,000 or to imprisonment for a term not exceeding 1 year or both

ROC -

i) Section 51 - not exceeding RM20,000

ii) Section 58 - not exceeding RM50,000

Final Words

In conclusion, the business owner and company directors’ must update any changes of information to SSM. The information provided to SSM must be true and correct to avoid any unnecessary penalty imposed by SSM.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Book-keeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource book-keeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Common Mistakes in Reinvestment Allowance

Common Mistakes in Reinvestment Allowance

Reinvestment Allowance is a red flag to IRBM so Reinvestment Allowance is always scrutinized by our IRBM during tax audit/investigation.

What is reinvestment allowance?

Reinvestment allowance (RA), as the name suggests, is an incentive to encourage companies to reinvest and expand their businesses. It is only granted after the company has been in business for a certain period of time, and only to companies resident in Malaysia.

How good is reinvestment allowance?

The allowance is given for 15 years from the first year of claim. The allowance is computed at 60% of QCE incurred and can be utilised against 70% of statutory income

Latest development in reinvestment allowance

Budget 2021 has announced that a special Reinvestment Allowance (RA) will be given for eligible manufacturing and agricultural projects in Years of assessment (YA) 2020 to YA 2022.

This means that eligible companies that have fully utilized their 15-years RA can enjoy additional RA claims for 3 years (YA2020 to YA2022).

Common mistakes in claiming reinvestment allowance

-

The purchase invoice is the only supporting document available. The absence of a project paper, feasibility study, business plans, budgets, directors resolutions, and other relevant documents supporting the project;

-

Mismatch between the company incurring the investments and the company using the plant and machinery;

-

Claim RA on assets incurred for the benefits of related companies/directors.

-

Claim RA on non-qualifying activities.

-

Claim RA on the transfer of assets from related parties who have previously claimed RA on the same assets.

-

The absence of payment records to support the qualified assets.

-

Supporting documents are not kept for at least 7 years.

-

Clain RA concurrently with other tax incentives (like PS, ITA & etc).

-

No written/ pictorial production flow on the qualifying project

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Book-keeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource book-keeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

SSM Discount On Compound 2022

SSM Discount On Compound 2022

6 common mistakes under Companies Act 2016 for Private Company “Sdn Bhd” (Part 2)

-

Failure to display on invoice or any documentation – Penalty: Subject to SSM general offence penalty

-

Failure to display on signboard – Penalty: Subject to SSM general offence penalty

-

Late submission of Annual Return - Penalty: Max RM50,000

-

Late preparation of Audited Financial Statement – Penalty: Max RM500,000 + imprisonment max 1 year

-

Late circulation of Audited Financial Statements – Penalty: Max RM50,000

-

Late submission of Audited Financial Statement – Penalty: Max RM50,000

SSM Discount On Compound 2022

-

Reduction rate :

Up to 90% applies to all offences except for out of court settlement or Inquiry Paper

-

Reduction period :

Until 31 December 2022. Any Compound that remains unpaid after this period will return to the original amount.

How To Get The Discount

Step 1 : Check compound status by:

a) Email to ar_compliance@ssm.com.my; or

b) online via e-Kompaun or EzBiz; or

c) visit any SSM office or call SSM Centre at 03-7721 4000

Step 2 : Prepare an appeal letter to SSM

Step 3 : Purchase Bank Draft, Debit/Credit Card, Money Order or Postal Order to the name of SURUHANJAYA SYARIKAT MALAYSIA

Step 4 : Deliver to any SSM branch for settlement of the compound with SSM receipt

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Reinvestment Allowance Excluded List

Reinvestment Allowance Excluded List

Why my ex-tax agent can claim Reinvestment Allowance on my bakery business in a shopping mall?

A incoming new client, a bakery in shopping mall, challenge us to follow their ex-tax agent past practice on claiming reinvestment allowance recently.

We are stunned but show them PU (A) 23 2012 on the excluded activities and a tax case Lavender Confectionery and Bakery.

Excluded List

The following activities are excluded from the definition of “manufacturing” as per PU (A) 23 2012

-

Ice making

-

Herb or spice-related activities

-

Folding and shaping papers box, cardboard, plastic bag & envelop

-

Laminating

-

Quarrying, Mining, and Extraction of mineral

-

Processing of photograph, picture, slide and film

-

Baking except in a factory

-

Distillation of filtration of water

-

Treatment of waste water and solid waste

-

Mixing and blending of petroleum product

What can taxpayer do now?

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

How to pass the SIRIM verification requirement of the machine for Automation Capital Allowance (ACA)

How to pass the SIRIM verification requirement of the machine for Automation Capital Allowance (ACA)?

Overview

Under the National Budget 2015, the Automation Capital Allowance (ACA) incentive was released to encourage the quick adoption of automation in the manufacturing sector.

The application for the ACA is jointly assessed by both MIDA (non-technical assessment) and SIRIM (technical assessment). The Company that needs to claim the incentive must meet both requirements from MIDA and SIRIM.

On this topic, we will mainly focus on the requirement of the SIRIM for the verification of machines for ACA.

Key takeaways:

You will understand: -

1. What is the general eligibility of the machine?

2. What type of machine is considered automated?

3. What is the productivity enhancement need to be achieved?

4. Other contributing factors for productivity enhancement?

Summary of learnings:

1. What is the general eligibility of the machine?

(I) The machine is used directly in the process of carrying out the services.

(II) The machine is more advanced than the current technology used by the company.

(III) The machine should be used at least 1 month after installation/commissioning.

(IV) The machine is consisting at least one of the:

-Areas of automation / automated system and,

-Automation components

Note: the details of the automated system and components can be found in the next paragraph.

2. What type of machine is considered automated?

The machine shall consist of at least one of the following areas of automation / automated system:

(I) Material handling system

(II) Warehousing

(III) Processing equipment

(IV) Testing equipment

(V) Measurement system

(VI) Packaging equipment

(VII) Others (to specify)

The machine shall also consist of at least one of the following Automation components:

(I) Motion Controllers

(II) Pneumatic / Hydraulics

(III) Programmable Logic Controller (PLC)/Programmable Automation Controller (PAC)

(IV) Computer/Industrial Software including CAD/CAM/CAE/PLM

(V) Computer Numerical Control (CNC), High Speed, Multi Axes

(VI) Robot and Robotic System

(VII) Industrial Networking & Communication

(VIII) Visual system

(IX) Others (to specify)

3. What is the productivity enhancement need to be achieved?

(I) Reduction in the number of manpower involved in the operation

(II) Reduction in the number of man-hours

(III) Increase in efficiency by reducing human errors or reducing the time taken to complete tasks;

(IV) Reduction in accident/complaint rate

4. Other contributing factors for productivity enhancement?

(I) Possibility of upgrading in future

(II) Possibility of integrating into other processes

(III) Worker Safety & Environment Improvement

(IV) Energy Efficiency

Source:

SIRIM verification of machine/equipment for ACA

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Advance to Directors

Impact on Advance to Directors

🚩Issue

ABC Sdn Bhd is a dormant company (not yet commence since incorporation) with a share capital of RM100,000. There is a balance of advance to directors at the financial year ended 31.10.2022 where:

(i) Mr A holds 60% - RM60,000.

(ii) Mr B holds 10% - RM10,000.

What is the audit and tax impact on advance to directors?

🚩Opinion

Audit Impact

ABC company shall not make a loan to directors unless the loan or advances is made in the ordinary course of the company’s business according to section 224 of CA 2016.

Tax impact

Only the advances with internal funds made to Mr A whose shareholding > 20% is subjected to deemed interest which by referring to Paragraph 5.3 of Public Ruling No.8/2015 & Subsection 75A(2) of ITA 1967. Thus, Mr A’s outstanding balance will subject to deemed interest but Mr B will not.

Refer to Paragraph 6 of Public Ruling No. 8/2015, with the advances made to Director Mr A & B, the company is deemed to have commenced operation in accordance with subsection 21A (8) of the ITA 1967.

🚩Reasoning

Audit Impact

Section 224 of the Companies Act 2016 – Loan to director

• A company shall not enter any guarantee or provide any security in connection with a loan made to such a director by any other person, unless the loan is made:

(i) To meet the expenditure incurred or to be incurred by the director for the purpose of the company;

(ii) To a full-time director in purchasing or acquiring a home; or

(iii) Where the company has passed a resolution to approve a scheme for the making of loans to employees of the company and the loan is in accordance with that scheme.

• Penalty:

(i) An imprisonment of not > 5 years; or

(ii) A fine of not > RM3 million; or

(iii) Both.

Tax Impact

Subsection 75A(2) of the Income Tax Act 1967 – Meaning of a director

• A person who involved in the management of the company’s business; and

• Holds at least 20% of company’s ordinary share; or

• Directly or indirectly through other companies holds at least 20% of company’s ordinary share.

Public Ruling No. 8/2015

(a) Paragraph 5.3 – Determination and the amount of interest income deemed to be received by the company

• Internal funds: The amount of interest will be computed or determined based on the prescribed formula with ALR published by BNM in the basis year in which the loans or advances are given.

(b) Paragraph 6 - Loan or Advances by a dormant company to directors of the company

• A dormant company is deemed to have commenced operation if a loans or advances made to the directors in accordance with subsection 21A (😎 of the ITA 1967.

🚩Example/Sources

(i) Section 224 – Loans to director (Act 777, Companies Act 2016)

https://www.ssm.com.my/.../aktabi_20160915...

(ii) Definition of director

- Section 75A – Director’s Liability (Act 53, Income Tax Act 1967)

https://phl.hasil.gov.my/pdf/pdfam/Act_53_01032021_2.pdf

- Public Ruling No. 2/2019 – Director’s Liability

http://lampiran1.hasil.gov.my/pdf/pdfam/PR_02_2019.pdf

(iii) Public Ruling No. 8/2015 – Loan or advances to director by a company

https://phl.hasil.gov.my/.../LOAN_OR_ADVANCES_TO_DIRECTOR...

🚩Authored by Ong Xin Ying (Christine), Audit/Tax Junior of the Firm in her personal LinkedIn.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

MPERS Section 7 Statement of Cash Flows

MPERS Section 7 Statement of Cash Flows

What is the Statement of Cash Flows?

This is the statement showing the inflows and outflows of cash for the reporting period and showing separate changes from operating activities, investing activities and financing activities.

Information to be presented in the Statement of Cash Flows

1) Operating activities

The main activities that generate revenue for the company.

Example:

o Cash receipts from sales and other revenue

o Payments to suppliers and employees

o Payments or refunds of income tax

2) Investing activities

The acquisition and disposal of long-term assets and other investments not included in cash equivalents.

Example:

o Purchase and proceeds from the sale of Property, plant and equipment

o Purchase and proceeds from the sale of marketable securities

o Advance or repayment of advances and loans made to other parties

3) Financing activities

It results in an entity's equity and borrowings changing in size and composition.

Example:

o Proceeds from issuing shares or other equity instruments

o Proceeds from issuing short-term or long-term borrowings and repayment of debts

Method to present the cash flow statement

2 types of methods to represent:

A) Indirect method

Determined by adjusting net Profit or loss for the effects of: -

-

Changes in inventories, receivables, and payables;

-

Non-cash items, such as depreciation, unrealised foreign currency gains and losses and etc; and

-

All other items that relate to investing or financing.

B) Direct method

Major classes of gross cash receipts and payments are disclosed.

Information may be obtained such as:

-

From the accounting records; or

-

By adjusting sales, cost of sales and other items in the income statement for:

-

Changes in inventories, receivables, and payables;

-

Other non-cash items; and

-

Other items that are investing or financing.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

What are the criteria for an individual to become a tax resident in Malaysia?

What are the criteria for an individual to become a tax resident in Malaysia?

There are 4 criteria for the basis year of assessment to determine an individual’s residency status in Malaysia.

If he falls into any of these criteria, he will be a resident, if not, he will be a non-resident.

Let's start to understand the following 4 criteria:

In Malaysia for ≥ 182 days in a basis year

The number of days does not have to be consecutive.

In Malaysia for ≤ 182 days in basis year

A period of less than 182 days can be linked to another period of 182 consecutive days or more during which he was in Malaysia before or after the current basic year.

In calculating the period, temporary absence is allowed as following: -

1. Attending conference or seminar abroad

2. Ill-heath involving the individual or immediate family member

3. Social visit not more than 14 days

In Malaysia for ≥ 90 days

The number of days does not have to be consecutive. 3 out of 4 years of assessment before/after the current year assessment

-

He is a resident; OR

-

He is in Malaysia for 90 days or more

Not in Malaysia or in Malaysia for ≤ 90 days

-

The individual is resident for 3 consecutive year assessment prior to the current basic year assessment; AND

-

The individual is a resident for the next year of assessment.

Source:

Public Ruling No 11/2017 - Residence Status of Individuals

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Avoiding Pitfalls When Claiming Tax Incentives

Avoiding Pitfalls When Claiming Tax Incentives

How one seminar amazed me!

On 30 November 2022, I attend Ms Yong Mei Sim webinar ''Avoiding Pitfalls When Claiming Tax Incentives'' conducted by the Chartered Tax Institute of Malaysia.

When it comes to tax incentives, I thought to myself ''What else can tax incentives changes since I have been doing for more than 20 years? Now what?''

Nevertheless, I am truly surprised to realise there are some insights or changes from MIDA or IRBM relating to tax incentives policy.

The key takeaways from the webinar can be summarised as follow :

1. Intellectual property (IP) income is excluded from tax incentives due to ''compliance'' with the OEDC ruling on preferential tax treatment!

2. The use of tax incentives to attract foreign investment is considered ''harmful tax competition'' under the current global tax environment-BEPS (not K-Pop boy band).

3. Taxpayers are to comply MIDA annual declaration as duly certified by the external auditor on pre-determined operating/capital expenditure and employment, local value add %, preparation of transfer pricing documentation & etc.

4. IRBM shall ''tarik balik''/revoke tax incentive shall those conditions from MIDA are not met.

5. Discuss with MIDA the relaxation of terms and conditions with relevant facts and documentary justification ASAP.

6. With effect from 7 July 2019, a Malaysian company with corporate shareholders is no longer eligible for the Allowance of Increased Export.

7. Trading of agriculture products is not eligible for the Allowance of Increased Export.

8. ''Contract R&D company'' and ''R&D company'' must be approved by MITI under the new Section 4H of the Promotion of Investment Act 1986.

9. Full documentation from the project paper, feasibility study, board resolution, and other documents (engineering report, cost-saving report, financing report & etc) to support the Reinvestment Allowance claim.

Maybe it is a good time to conduct a risk assessment review before IRBM knock on your door for a tax audit.

In short, don't play play with tax incentives.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Tax Incentive for Employers Who Provide Child Care Centre

Tax Incentive for Employers Who Provide Child Care Centre

Definition of childcare centre

A centre to take care of:

• At least 4 or more children;

• Aged below 4 years old;

• From more than one household

Qualifying childcare centre

• Registered with the Department of Social Welfare (DSW);

• Subjected to Child Care Centre Act 1984 (Act 308);

• Governed by the Ministry of Women, Family and Community Development

Existing Tax Treatment

(i) Provision and maintenance of childcare centre

Expenses incurred for the provision and maintenance of a child care centre are allowed for tax deduction. [Paragraph 34(6)(i) of the ITA 1967]

Examples:

-

Rental

• Salaries

• Food and beverage

• Cleaning fee

(ii) Child care allowances

Employer – Provider

• The child care allowance paid to employees who have children is allowable for tax deduction under Section 33(1) of the ITA 1967.

Employee – Receiver

• Employee has to declare the allowances received as part of gross income, which subjects to tax. [Paragraph 13(1)(a) of the ITA 1967]

• Enjoy tax exemption up to RM2,400.

Additional Tax Incentives

A 100% further deduction will be given in respect of:

• The provision and maintenance of child care centre; and

• Child care allowances paid to employees

Industrial Building Allowance (IBA)

An employer is entitled to claim a 10% IBA of the capital expenditure of the building, where it is:

• Built or purchased by the employer;

• Served as a child care centre for his employees' children; and

• In operation

Qualifying Capital Expenditure (QCE)

Only cost attributable to the building is entitled, which include:

• Purchase price

• Legal fee

• Stamp duty

• Other incidental expenditure

Sources:

Public Ruling No. 5/2016: Tax Incentives For Employers Who Provide Child Care Centres

https://phl.hasil.gov.my/pdf/pdfam/PR_5_2016.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Month End Closing

Month End Closing

The month-end close is the collection of financial accounting information, review, and reconciliation of records each month. This is a financial reporting requirement for some companies and helps businesses keep accurate records throughout the year.

Appended below is the checklist for month end closing :

-

Record incoming cash

-

Update account payable

-

Reconcile bank accounts

-

Review petty cash

-

Review fixed assets

-

Count stocks

-

Check revenue and expense account

-

Adjust journal entry

-

Final review

-

Plan for next month

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Minimum Transfer Pricing Documentation LHDN

Minimum Transfer Pricing Documentation LHDN

On 11.11.2022 LHDN has published a new document for transfer pricing which is Minimum Transfer Pricing Documentation.

The Minimum Transfer Pricing Documentation is to replace the Limited Transfer Pricing Documentation.

Key takeaways:

You will understand the:

1. Requirement to use this documentation.

2. Differences between Minimum Transfer Pricing Documentation and Limited Transfer Pricing Documentation.

Requirement to use the documentation

According to Section 3.1 of Transfer Pricing Guidelines 2012, there are two criteria to be determined:

i. gross income and total related party transactions must be greater than RM25 million and RM15 million respectively; or

ii. financial assistance must be greater than RM50 million.

If tax payer fulfils one of the criteria as above, Full Transfer Pricing Documentation should require to be prepared.

On the other hand, Minimum Transfer Pricing Documentation is required for those falls outside the transfer pricing guidelines 2012 section 3.1.

Differences between Minimum Transfer Pricing Documentation and Limited Transfer Pricing Documentation.

The major difference between these two documentations is comparability study. In previous Limited Transfer Pricing Documentation, we do not perform any comparable working and causing there is a limitation to justify the reasonableness of pricing policy.

Minimum Transfer Pricing Documentation has implemented a new section to resolve this limitation.

New Requirements

Under section D of Minimum Transfer Pricing Documentation, there are 6 columns need to fill in to justify the transfer price is reasonable, which are:

• What is the element of costs

• What is the anticipated profit mark-up

• Who determine the pricing policy

• How often is the policy being revised

• Sample of documents to support the pricing policy

• Comparability study Source Minimum Transfer Pricing Documentation

Source:

https://www.hasil.gov.my/media/gesbb4yx/template-minimum-tp-doc-1_2022.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Service Tax on Customs Agent Services

Service Tax on Customs Agent Services

On 09 August 2022, RMCD issued a Guide on Customs Agent Services. Generally, this guide is to let us know about the service tax treatment on customs agent services.

Key takeaways:

You will understand 5W:

1. Who is Customs Agent?

2. What is the threshold for registration under Service Tax?

3. What types of services are subject to service tax?

4. What types of services are not subject to service tax?

5. What are the responsibilities of the registrant?

Who is “Customs Agent”?

Who acts on behalf of importers and exporters to carry out the business to relieve goods from customs control.

What is the threshold for registration under Service Tax?

-

·There is no threshold for Customs Agent.

-

All customs agent must apply for service tax registration within 14 days from the date of approval as a customs agent.

What types of services are subject to service tax?

1. Preparing or amending customs declaration

2. Presenting goods for customs declaration

3. Documentation

4. Handling / forwarding

5. Examination / attendance to examination

6. Sealing

7. Electronic Data Interchange (EDI)

8. Overtime (relating to clearance of goods only)

What types of services are not subject to service tax?

1. Haulage services

2. Services provided by shipping agents and freight forwarders

What are the responsibilities of the registrant?

1. Charge service tax on taxable services

2. Issue an invoice and receipt to customers

3. Submit SST-02 Form and pay service tax before the deadline

4. Keep proper record

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

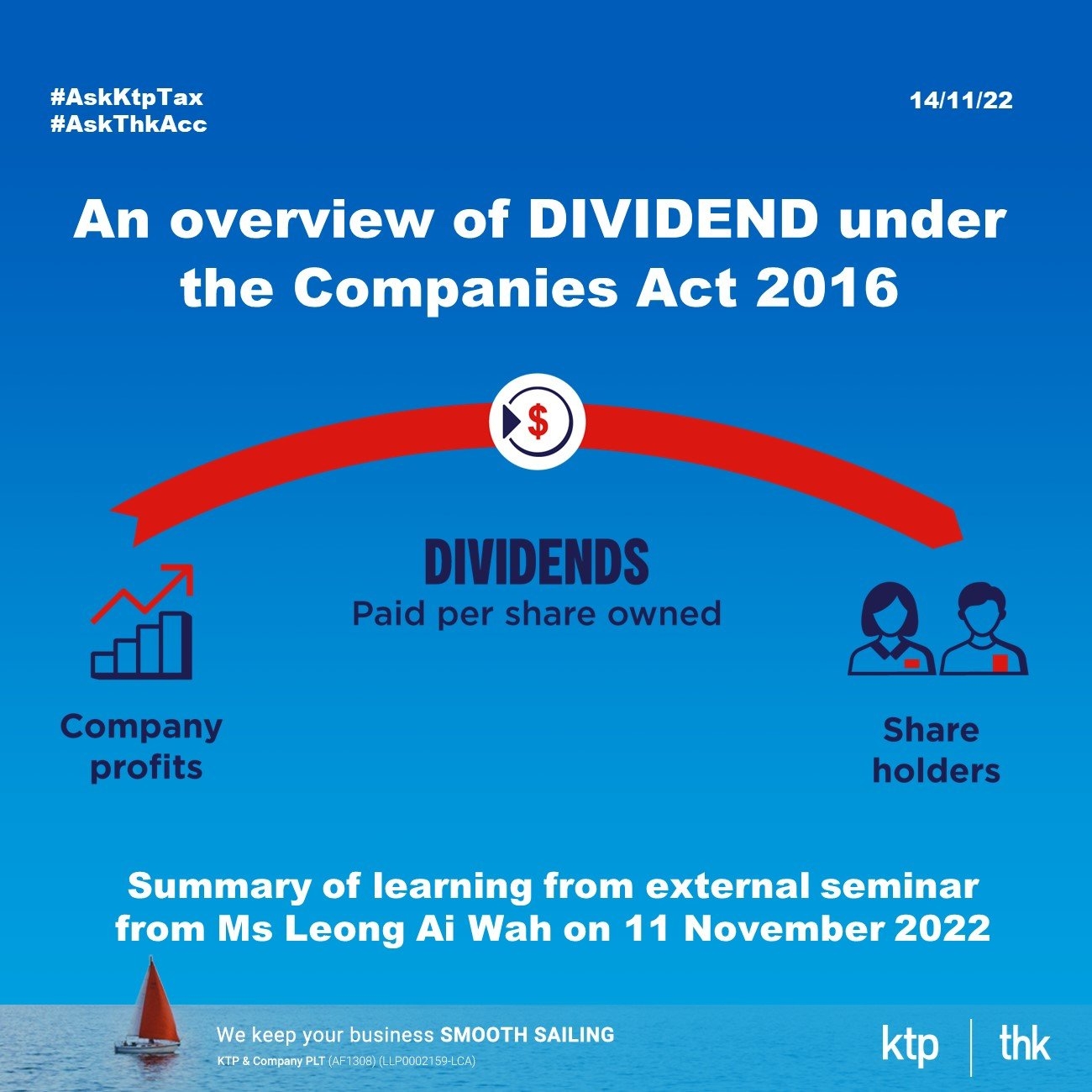

Dividends the Companies Act 2016

Dividends the Companies Act 2016

Continuous learning is part of our company culture…

We attended an external webinar on “Everything About Dividends” from Ms Leong Ai Wah on 11 November 2022.

The key takeaway from the webinar:

a) Dividend distribution requirements.

b) How is available profit determined?

c) Powers to declare dividends.

d) Dividend policy

e) Solvency test can be cashflow or ratio

f) Dividend distribution method

Summary of learning

Here is the summary reflected in the webinar is dividends can only be distributed to shareholders if the company has available profit and solvency.

Most of the time we focus on retained earnings, but in fact, the profits for the year can also be used to determine dividend distribution.

The power to declare dividends differs between companies with constitution and those company without constitution. The companies with constitution will be determined by the board of directors and followed by members at the annual general meeting. For companies without constitution, the decision is made only by the board of directors.

Dividend Policies

Dividend policies are divided into 3 categories namely Residual, Stable and Hybrid. The Residual policy is that dividends are paid only when all capital requirements are met, but with the Stable policy, dividends are paid annually regardless of earning fluctuations. However, the Hybrid policy is a combination of Residual and Stable.

Solvency Test

Typically, most of us assess a company's solvency by preparing a cash flow statement for the next 12 months from the payment date. In fact, in addition to the cash flow statement, we can also use the 3 ratios to do the solvency test. There are quick ratio, current ratio and solvency ratio.

Payment Mode

As we know, cash dividends are the most common payment method. In fact, there are any other payment methods, such as share dividends, also known as bonus issue. It will be paid up in full or in part non-cash using shares allocated or deemed allocated.

The third is set-off again amount owing, for example a company can declare a dividend to offset what is owed by shareholders.

Fourth, dividend in specie, also called the transfer of assets is also one of the mode of payment for distribute dividend. For example, land. The land is allocated according to the shareholders' shares.

Lastly, there are dividend reinvestment plans, which are plans that allow shareholders to reinvest cash dividends in additional company shares.

Thanks to the speaker – Ms Leong Oi Wah for hosting this webinar and giving us a clear picture of the dividend.

Authored by Caroline Teo, our assistant manager of the firm in our Group in her personal LinkedIn. http://bit.ly/3UQh5fE

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Key Amendments to the Employment Act 1955 (wef 1/1/2023)

Key Amendments to the Employment Act 1955 (wef 1/1/2023)

Definition of employment

1. Employee earning RM4000 and below *

2. Employee in manual labour

3. Supervisor of employee in manual labour

4. Employee in mechanically propelled vehicle

5. Domestic employee

*Provision of the Act not applicable include overtime, payment for work done on off/rest day and public holidays, shift allowance and termination benefits for employee’s wages exceeds RM4000.

Presumption of employment

The Bill provides that in the absence of a written contract and unless proven otherwise, there will be presumption of an employment relationship if the following factors are given:

-

his/her work or hours of work are subject to control by another person;

-

he/she is equipped with tools, material or equipment by another person to execute his work;

-

his/her work constitutes an integral part of another person's business;

-

his/her work is performed solely for the benefit of another person; or

-

payment is made to him/her for work done at regular intervals and it constitutes the majority of his/her income.

Apprenticeship Contract

Shall be for a minimum period of six months and a maximum period of twenty four months.

Calculation of wages for an incomplete month

The Bill provides a new section in the Act that introduces the below formula for calculating wages where an employee has not worked a full month:

(Monthly wages/number of days of the particular wage period ) X Number of days eligible in the wages period

For OT (or encashment of annual leave) : ordinary rate of pay (ie 26 days) remain unchanged under the current law.

Extension of maternity leave

Previously, the Act provided a 60 days maternity leave for all female employees, subject to the conditions of the Act. Now, when the Bill comes into force, eligible female employees will be entitled to 98 days of maternity leave.

Restriction on termination of pregnant employees

The Bill introduces a new section in the EA which prohibits an employer from terminating an employee who is pregnant or is suffering from an illness arising out of her pregnancy, except under specific circumstances such as willful breach of contract, misconduct or closure of the employer’s business. It is vital on employers to prove that the termination was not due to pregnancy.

Paternity Leave

Married male employees will now be entitled to 7 consecutive days of paternity leave up to 5 confinements.

Sexual harassment

The Bill introduces a new section which requires employers to conspicuously exhibit a notice to raise awareness of sexual harassment in the workplace. The sexual harassment provisions are still viewed as weak and limited. The Anti Sexual Harassment Bill 2021 would provide more guidelines upon being passed. It is currently in its first reading in Parliament.

Employment of foreign employees

Approval must be obtained from the Director-General of Labor to employ a foreign employee. Upon the employer satisfying the conditions listed in the Act, approvals are granted. Failure to obtain an approval is an offense, and on conviction, the employer shall be liable to a fine not exceeding RM 100,000 and/or to imprisonment for a term not exceeding five years.

Reduction on working hours

Previously, the Act provided 48 hours as regular working hours. With the Bill coming into force, the regular working hours will be reduced to 45 hours a week.

Flexible working arrangements

Employees can apply for flexible working arrangement, depending on the suitability of the working hours or work place. However, there is no legal obligation on the employer to grant this request. If the employer is to reject the request, they are required to provide grounds of refusal within 60 days of the application.

Discrimination

The Director General has the authority to investigate and decide disputes on discrimination in employment between employer and employee. Furthermore, the Director General has the power to make an order where necessary. However, this provision is vague and it does not define discrimination. Job seekers will not be able to rely on this provision as there is no employment relationship between an employer and job seekers, and as such this provision will not apply to protect job seekers from discrimination.

This message was brought to you by KTP