Blog

(Tax Update) Capital Gain Tax Malaysia

(Tax Update) Capital Gain Tax Malaysia

Effective 1 January 2024, Malaysia introduced a capital gains tax (CGT) through the Finance (No. 2) Act 2023 under which gains or profits from the disposal of capital assets are treated as income chargeable to income tax under the Income Tax Act 1967 (ITA).

Welcome to our guide on Capital Gains Tax (CGT)! If you're new to taxes or finding CGT confusing, don't worry. We, #ktp, here to help you understand everything easily.

In this video, we'll explain CGT basics in simple terms. We'll cover when CGT starts, who has to pay it, what it applies to, and more.

Let's get started on CGT

1. What is Capital Gain Tax (CGT)?

2. What is the effective date of CGT?

3. Who is liable/ chargeable to CGT?

4. What is the scope of CGT imposition?

5. How are the disposal and acquisition dates be determined?

6. How is the disposal price determined?

7. What constitutes a gain arise from disposal of CG?

8. How are losses treated under CGT?

9. What is the rate of tax?

10. When are returns required to be filed and taxes paid?

Video

Watch 15 minutes CGT video on our Youtube https://youtu.be/GNtW58J0Bio

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

(Sec Update) The Amended Occupational Safety and Health Act

(Sec Update) The Amended Occupational Safety and Health Act

The Minister of Human Resources in exercise of the powers conferred by subsection 1(2) of the Occupational Safety and Health (Amendment) Act 2022 – Act A1648 and subsection 1(2) of the Factories and Machinery (Repeal) Act 2022 – Act 835, appoints 1st June 2024 as the date on which the Act A1648 and Act 835 comes into operation.

The Act A1648 and Act 835 will affect all organizations (exemption is given to domestic workers, the Malaysian army, and workers on board ships) regardless of risk level and nature of business. With effect from 1st June 2024, some provisions under the Factories and Machinery Act 1967 (FMA 1967) [Act 139] will be migrated as new regulations under the Occupational Safety and Health (OSHA 1994) [Act 514].

We set out below the key changes under the Amended OSHA as below

Implementation and Scope:

Effective Date

The new amendments, Acts A1648 and Act 835, will be enforced starting 1st June 2024.

Affected Legislation

Provisions from the Factories and Machinery Act 1967 are integrated into the Occupational Safety and Health Act 1994.

Coverage

The updated legislation applies to all workplaces across Malaysia, including public services and statutory authorities, but excludes domestic workers, the Malaysian army, and maritime workers.

New Regulations and Provisions

Risk Assessments and Emergency Procedures

Employers are required to conduct thorough risk assessments and develop procedures to handle emergencies at the workplace.

Principal's Responsibilities

A new duty for principals to ensure the safety of contractors and subcontractors, emphasizing the safety of workers under their directive control.

Workers' Safety Rights

Workers now have the right to remove themselves from situations of imminent danger without repercussions.

Occupational Health Services

Mandatory health services and the designation of an OSH Coordinator in organizations with five or more employees.

Training and Licensing

Specific training is mandated for certain classes of persons, along with integrity and licensing requirements for machinery.

Penalties

The penalty structure is revised with significant increases, including fines up to RM500,000 and/or imprisonment for severe violations.

Appointment of occupational safety and health coordinator

The new provision mandates that employers who operate workplaces not specifically classified under existing regulations, and who have five or more employees, must appoint an Occupational Safety and Health Coordinator (OSH Coordinator).

The primary responsibility of the OSH Coordinator is to manage and coordinate safety and health issues at the workplace. This role is distinct from that of a Safety and Health Officer (SHO), who is tasked with ensuring compliance with the Occupational Safety and Health Act (OSHA) and its regulations across different workplaces.

Specific Regulatory Updates

Plant Certification and Licensing

New regulations under the Occupational Safety and Health (Plant Requiring Certificate of Fitness) Regulations 2024 and the Occupational Safety and Health (Licensed Person) Order 2024 detail requirements for plant operations and certifications.

Director and Officer Liability

Directors and specified office bearers are made jointly and severally liable for safety breaches, with provisions for defense in cases of unknowing violations.

Enhanced Notification and Inspection

Notification Requirements

Expanded obligations for reporting the usage of workplace premises and activities, focusing on proactive enforcement.

Certification of Fitness

Stringent standards for the certification and inspection of plants, ensuring their operational safety and compliance.

Overall Impact

These amendments aim to enhance workplace safety across all sectors in Malaysia, increasing accountability, broadening the scope of coverage, and reinforcing the regulatory framework for occupational safety and health. The increased penalties and comprehensive coverage intend to foster a safer working environment nationwide.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

(Tax Update) IRBM e-invoice Guideline Version 2.30 (published on 6/4/24)

(Tax Update) IRBM e-invoice Guideline Version 2.30 (published on 6/4/24)

The Inland Revenue Board of Malaysia (IRBM) recently updated its Software Development Kit (SDK) and guidelines for e-invoice on 6 April 2024. With important deadlines approaching for businesses of different sizes, it's crucial for taxpayers to understand these changes and how they affect their operations.

Here's a simpler breakdown of the updates:

Self-Billed e-Invoice for Importation

Malaysian businesses involved in importing goods and services must now issue a self-billed e-Invoice within a specific timeframe after receiving their Customs import declaration. This requirement aims to streamline tax documentation and compliance for imports, with deadlines tailored to the date of receiving the Customs declaration.

To be more specific, for importation of goods, the self-billed e-Invoice is required to be raised by the end of the month following the month in which Customs declaration (K1) is obtained. As an example, if K1 is obtained anytime during the month of August, the self-billed e-Invoice is required to be raised by 30th September.

As for importation of services, self-billed e-Invoice is required to be issued latest by the end of the month following the month in which the rule for timing of imported service tax is satisfied, i.e. earlier of payment and receipt of invoice. For avoidance of doubt, the requirement for self-billed e-Invoice applies regardless of whether imported service tax is required to be accounted on the invoice.

FOREX Clarification

The recent updates provide clarity on handling foreign exchange (FOREX) rates in transactions involving foreign currencies. Businesses have the flexibility to choose the FOREX rate based on their internal policy unless specific regulatory requirements dictate otherwise.

This clarification helps businesses in accurately reporting their financial transactions involving foreign currencies.

Non-Monetary Transactions

The IRBM has clarified that e-Invoicing requirements extend to non-monetary transactions, such as incentive trips and gift vouchers given to dealers. This update ensures that all forms of transactions, whether monetary or non-monetary, are appropriately documented and compliant with e-Invoicing regulations.

Credit Notes for Multiple e-Invoices

It's now confirmed that businesses can issue a single credit note that adjusts the transaction values of multiple e-Invoices. This flexibility is particularly useful for businesses dealing with returns or adjustments across several invoices, simplifying the process without being constrained by character limits.

Consolidated e-Invoices for Individuals

Businesses can issue consolidated e-Invoices for payments made to individuals, simplifying documentation and reporting.

However, payments to individuals acting as agents, dealers, or distributors require individual transactional self-billed e-Invoices, addressing tax compliance more rigorously.

Interest Payments

The updates outline specific requirements for issuing e-Invoices or self-billed e-Invoices for interest payments. The responsibility for issuing these documents depends on the nature of the transaction and the parties involved, aiming to close tax compliance gaps effectively.

Flexibility for Statements as e-Invoices

There's now greater flexibility in using statements as e-Invoices. Businesses can include adjustments and rebates within these documents, facilitating a more streamlined approach to e-Invoicing and compliance.

Size Limitation

New size limitations for e-Invoice submissions to the IRBM have been introduced, including a maximum submission size of 5MB, a cap of 100 e-Invoices per submission, and a maximum size of 300KB per e-Invoice. These limits are crucial for managing the data flow to the IRBM efficiently.

Digital Signature

Businesses can utilize the digital signature of their service provider for e-Invoice submission to the IRBM. This provision allows for a seamless integration and submission process, ensuring the authenticity and integrity of the e-Invoices submitted.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

How to Pay Withholding Tax Online

(Tax Update) How to Pay Withholding Tax Online

Paying and submitting withholding tax in Malaysia under the Electronic Transmission of Tax (eTT) system involves several steps, generally centered around using the Malaysian Inland Revenue Board's (LHDN) online platforms.

The eTT system is designed to streamline the process of declaring and paying taxes, including withholding tax, which is a tax deducted at source on certain types of payments made to non-residents in Malaysia.

Here’s a step-by-step guides :

Start at the MyTax Website

-

Access the MyTax website and head over to ''ezHasil Services.''

-

Select the ''e-TT'' option, followed by ''Electronic Telegraphic Transfer.''

Proceed Through the Steps

-

Click ''Next'' to move forward.

-

Enter your identification details and click ''Next'' again.

-

Provide your email address and proceed to the next step.

-

Input the One-Time Password (OTP) code you receive for verification.

Enter Payment Details

-

Navigate to the ''Payment Details'' section.

-

Choose ''Withholding Tax (WHT)'' as the payment type.

-

Fill in your tax number, address, and select the applicable tax section.

Submission and Virtual Account Number

-

Review all the information you've entered to ensure accuracy.

-

Submit your information.

-

Upon submission, you'll receive a Virtual Account (VA) Number. Print this out for your records.

Complete the Payment

-

Use the provided VA number to make your payment. This can be done via online banking, at a bank counter, or through an ATM.

Email Supporting Documents

-

After payment, email the necessary supporting documents. This includes the Withholding Tax form, a copy of the invoice, proof of payment, the VA number, and the bank transfer slip.

This guide provides a general overview. The specific steps, forms, and procedures may vary slightly depending on various factors, including changes in the e-Filing system or updates in tax laws.

For the most current and detailed instructions, it’s best to consult the LHDN’s official website or contact your trusted tax agent directly.

Past Blog on Withholding Tax

-

Tax Update on Withholding Tax on Royalties dated on 06.12.2023

https://www.ktp.com.my/blog/tax-treatment-on-copyright-and-software-payments-by-distributor-reseller-to-non-resident/06dec23

-

Tax Update: Use Of e-WHT For WHT Payment dated on 08.09.2023

https://www.ktp.com.my/blog/use-of-e-wht-for-wht-payment/08sept23

-

Tax Update - Form E-107D : 2% Tax Deduction For Commission to Agents, Dealers or Distributors dated on 29.06.2023

https://www.ktp.com.my/blog/2percent-tax-deduction-for-commission-/29june23

-

Tax Update on Withholding Tax dated 07.11.2022

https://www.ktp.com.my/blog/tax-update-on-withholding-tax/07nov22

-

Small Value Withholding Tax Payment (update) dated 07.10.2022

https://www.ktp.com.my/blog/small-value-withholding-tax-payment-update/07oct22

-

Small Value Withholding Tax Payment dated 19.08.2022

https://www.ktp.com.my/blog/small-value-withholding-tax-payment/19aug22

-

(Update) 2% Withholding Tax on Commission to Agents dated on 12.07.2022

https://www.ktp.com.my/blog/2percent-withholding-tax-on-payments-to-agents/12july22

-

(Latest update) Withholding Tax on Payments to Agents dated 21.04.2022

https://www.ktp.com.my/blog/2percent-withholding-tax-on-payments-to-agents/21apr22

-

Withholding Tax on Payments to Agents dated 17.03.2022

https://www.ktp.com.my/blog/2percent-withholding-tax-on-payments-to-agents/17mar22

-

Top 5 Withholding Tax Questions dated 28.01.2022

https://www.ktp.com.my/blog/top-5-withholding-tax-questions/28jan22

-

2% withholding tax on commission dated 30.12.2021

https://www.ktp.com.my/blog/2-withholding-tax-on-commission/30dec21

-

(English Version) Do you know how to reduce withholding tax with the certificate of residence (COR)? Dated 23.11.2021

https://www.ktp.com.my/blog/certificate-of-residence-lhdn/22nov21

-

(Chinese Version) 您知道如何使用居住证 (COR) 减少预扣税吗?dated 23.11.2021

https://www.ktp.com.my/blog/certificate-of-residence-lhdn-chinese/22nov21

-

(English Version) Budget 2022 – SME edition dated 18.11.2021

https://www.ktp.com.my/blog/tax-budget-2022-sme-edition/18nov21

-

(Chinese Version) 2022 年预算摘要 - 中小企业版dated 19.11.2021

https://www.ktp.com.my/blog/tax-budget-2022-sme-edition-chinese/19nov21

-

两个重要改变 - 预扣税(withholding tax)dated 11.11.2021

https://www.ktp.com.my/blog/withholding-tax-malaysia/11nov21

-

Purpose and usage of certificate of residence under withholding tax in Malaysia dated 23.04.2021

https://www.ktp.com.my/blog/certificate-of-residence/23april2021

-

马来西亚预扣税 (𝐖𝐢𝐭𝐡𝐡𝐨𝐥𝐝𝐢𝐧𝐠 𝐭𝐚𝐱)的规则概述(第3篇) dated 21.09.2020

https://www.ktp.com.my/blog/fwwses3ezyrg9gf-7r8xl-aaa5d-739bg-8lcep-c266s-s32bd-wf736-e4xsk-x3fp4-gj5z8-mwgzk-m3696-gw4b5-mmmbe

-

马来西亚预扣税 (𝐖𝐢𝐭𝐡𝐡𝐨𝐥𝐝𝐢𝐧𝐠 𝐭𝐚𝐱)的规则概述(第2️⃣篇) dated 21.09.2020

https://www.ktp.com.my/blog/fwwses3ezyrg9gf-7r8xl-aaa5d-739bg-8lcep-c266s-s32bd-wf736-e4xsk-x3fp4-gj5z8-mwgzk-m3696-gw4b5

-

马来西亚预扣税(withholding tax)的规则概述 (第1️⃣篇) dated 15.09.2020

https://www.ktp.com.my/blog/fwwses3ezyrg9gf-7r8xl-aaa5d-739bg-8lcep-c266s-s32bd-wf736-e4xsk-x3fp4-gj5z8-mwgzk-m3696

-

Withholding Tax In Malaysia Part 2 of 2 dated 28.06.2019 (eKTP 114)

https://www.ktp.com.my/blog/withholding-tax-in-malaysia-part-2-of-2

-

Withholding Tax In Malaysia Part 1 of 2 dated 28.06.2019 (eKTP 113)

https://www.ktp.com.my/blog/withholding-tax-in-malaysia-part-1-of-2

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

The Role of Company Secretaries on Money Laundering

The Role of Company Secretaries on Money Laundering

Company Secretaries stand at the forefront of efforts to combat money laundering and terrorism financing. As key figures within organizations, their responsibilities extend to implementing preventive measures outlined in regulatory frameworks like the Anti-Money Laundering Act. In this article, we'll explore the pivotal role company secretaries play in safeguarding financial systems against illicit activities and the essential steps they must take to mitigate risks effectively.

Understanding Money Laundering:

Money laundering is a complex process where cash obtained from illegal activities is integrated into the financial system to make it appear legitimate. This process involves three key stages:

Placement

This is the initial stage where cash proceeds from illegal activities are physically placed into the financial system. This could involve depositing cash into bank accounts or using it to purchase assets.

Layering

The illegally obtained funds are moved through a series of transactions to obscure their origin. This could involve transferring funds between accounts, converting them into different currencies, or making complex financial transactions to create layers of complexity. Until the funds look clean and from legal sources.

Integration

The final stage involves integrating the laundered funds back into the economy in such a way that they appear to be from a legitimate source. This could involve investing in businesses, purchasing real estate, or making other high-value transactions.

Company Secretaries as Reporting Institutions:

Company Secretaries play a crucial role in preventing money laundering activities. Under Part IV of the Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of Unlawful Activities Act (AMLA), Company Secretaries are considered Reporting Institutions (RIs) and have obligations both as individuals and at the firm level to combat or prevent money laundering activities.

Preventive Measures Taken by RIs:

To prevent their institutions from being used for money laundering or terrorism financing, RIs must undertake various preventive measures, including:

Risk Assessments

Conduct thorough assessments of the risks associated with their clients, products/services, geographical locations, and delivery channels.

Customer Due Diligence (CDD)

Verifying the identity of clients using reliable and independent sources and conducting enhanced due diligence for higher-risk clients.

Screening Against Sanctions Lists

Checking client names against relevant sanctions lists to prevent dealings with individuals or entities involved in terrorism or proliferation activities.

Submitting Suspicious Transaction Reports (STRs)

Reporting any suspicious activities to the appropriate authorities, such as Bank Negara Malaysia (BNM).

Record Keeping

Maintaining records of transactions, KYC information, and analysis of STRs for at least seven years.

Keeping Information Updated: Regularly updating client information and conducting ongoing monitoring for any suspicious activities.

Furthermore, company secretaries must adopt a Risk-Based Approach (RBA) to identify, assess, and mitigate money laundering and terrorism financing risks. This involves documenting risk assessments, considering relevant risk factors, and keeping assessments up-to-date through periodic reviews.

In conclusion, Company Secretaries play a crucial role in combating money laundering and terrorism financing by implementing robust preventive measures, conducting thorough due diligence, and adhering to regulatory requirements outlined in the AMLA. By taking a proactive approach to risk management, they contribute to maintaining the integrity of the financial system and preventing illicit activities.

PS : Authored by Mr Syazwan, our THK secretary associate, in his personal LinkedIn.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

(Tax Update) Foreign Capital Assets CGT Guidelines

(Tax Update) Foreign Capital Assets CGT Guidelines

The Inland Revenue Board of Malaysia (“IRB”) has issued the Guidelines on Tax Treatment on Disposal of Foreign Capital Assets Received From Outside Malaysia (“Foreign Capital Assets CGT Guidelines”) dated 27 March 2024 on its website.

The Foreign Capital Assets CGT Guidelines explain the CGT treatment on the gains or profits from the disposal of foreign capital assets situated outside Malaysia that occur on or after 1 January 2024 that are received in Malaysia by a resident that is a company, limited liability partnership, trust body or co-operative society.

Key Summary of the Guideline

Here's a summary of the guidelines for the tax treatment on gains from the disposal of foreign capital assets received in Malaysia, as outlined by the IRB:

Introduction

Capital Gains Tax (CGT) applies to gains from the disposal of capital assets in Malaysia, including foreign capital assets received in Malaysia, effective from 1 January 2024.

Objective

To explain the tax treatment on gains from the disposal of foreign capital assets received by a resident in Malaysia.

Provisions of The Law

Includes specific sections of the Income Tax Act 1967 and the Income Tax (Exemption) Order (No. 3) 2024 [P.U.(A) 75/2024].

Chargeable Person

From 1 January 2024, companies, LLPs, Trust Bodies, and Co-operative Societies receiving gains from the disposal of foreign capital assets in Malaysia are subject to tax.

Chargeable Gains from the Disposal

Definition and Scope

Gains from the disposal of foreign capital assets situated outside Malaysia are considered taxable income under paragraph 4(aa) of the Income Tax Act 1967 (ITA), subject to the prevailing tax rate.

This includes assets such as immovable property (e.g., buildings, land), movable property (e.g., machinery, vehicles), intellectual property rights, and shares issued by companies incorporated outside Malaysia.

Taxability Timing

Only gains from the disposal of foreign capital assets that occur on or after 1 January 2024 are subject to tax. This includes gains received in Malaysia from such disposals, emphasizing the importance of the date of disposal and receipt of gains.

Deductible Expenses

In determining taxable gains, expenses wholly and exclusively incurred for the acquisition and disposal of the capital assets can be deducted. This includes legal fees, appraisal fees, advertising costs, and expenses to increase or maintain the capital value of the asset.

Foreign Tax Credit

Purpose

To avoid double taxation of gains from the disposal of foreign capital assets that are also taxed outside Malaysia. Taxpayers can claim a tax credit for foreign taxes paid, which is either bilateral (if the country has a Double Taxation Avoidance Agreement with Malaysia) or unilateral (if there's no such agreement).

Conditions for Claiming

Taxpayers must keep records proving that foreign tax has been imposed on the income. The claim for tax credit must be supported by adequate documentation.

Limitations

If the foreign tax credit claimed for a year of assessment exceeds the Malaysian tax payable on the same gains, the excess amount cannot be carried forward or refunded; it is simply disregarded.

Tax Exemption

Eligibility Period: Gains from the disposal of foreign capital assets received in Malaysia are exempt from tax from 1 January 2024 until 31 December 2026, provided they meet specific economic substance requirements.

Economic Substance Requirements

To qualify for the exemption, entities must employ an adequate number of qualified employees and incur a sufficient amount of operating expenditures in Malaysia for carrying out specified economic activities.

The determination of adequacy is based on the facts of each case, considering factors like the industry type, whether the business is capital or labor-intensive, and the nature of the employment (full-time or part-time).

Specified Economic Activities

For investment holding entities, this involves holding/managing equity participation in other entities and making strategic decisions regarding assets. For other entities, it refers to the operations of the business carried out in Malaysia.

Outsourcing of Activities

Entities can outsource specified economic activities if these are carried out in Malaysia, there's sufficient monitoring and control, and the outsourcing does not result in double counting of employees or expenditures.

Tax Reporting

Requirements for reporting gains from the disposal of foreign capital assets in the Income Tax Return Form (ITRF).

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

(Tax Update) Tax Incentives on Child Care and Kindergartens

(Tax Update) Investing in Kids' Future: Tax Incentives on Child Care and Kindergartens

Investing in child care and kindergartens isn't just good for kids; it's a smart choice for investors too. With more parents working, there's a growing need for quality places where children can learn and grow.

The government is stepping up, offering tax breaks to encourage investment in this important area. This means investing in child care and kindergartens can be financially rewarding and help shape the future of our children.

Let's dive into why putting your money into early education is a win-win for everyone involved.

Public Ruling 4/2016 Tax Incentive for Child Care Centre and Kindergarten Operators

Public Ruling No. 4/2016 by the Inland Revenue Board of Malaysia, we draft out a compelling case study highlighting the significant tax incentives and their impact on the financial performance and sustainability of child care centres and kindergartens.

This case study aims to provide potential investors with a comprehensive understanding of the financial benefits of investing in these operations, underscored by real-world examples and legislative support.

Tax Incentives Overview:

Registration Requirement

Must be registered with the relevant authority: Department of Social Welfare for child care centres or the State Education Department under the Ministry of Education for kindergartens.

Exemption of Statutory Income

The tax exemption applies to business statutory income for a period of five consecutive years.

For existing operators, the exemption commences from the Year of Assessment (YA) 2013.

For new operators, the exemption starts from the YA during which the first invoice is issued.

Industrial Building Allowance

Operators who incur qualifying building expenditure on construction or purchase of a building used in their operations can claim a 10% industrial building allowance annually for ten years.

This incentive is aimed at reducing operating costs and enhancing service quality.

Non-Applicability

The tax incentives do not apply to operators of private pre-schools whose activities are integrated with private primary schools.

Separate Business Sources

If an operator of a child care centre or kindergarten carries on another business, the income from that other business must be treated as a separate source of income, and separate accounts must be maintained.

Adjusted Losses

Adjusted losses incurred from the start of the business until the year before the exemption period, and during the exemption period, can be carried forward and deducted from the statutory income of the business in the post-exempt YAs until fully utilized.

Discontinuation

If the business ceases operation, any unutilized brought forward adjusted loss will be disregarded.

Real-Case Examples:

Situation

ABC is an established child care centre that has been operating since 2020.

For the year of assessment 2020, ABC reported an adjusted income of RM80,000.

Impact of Tax Incentives

Under the tax exemption incentive, ABCs' statutory income of RM80,000 is exempt from tax for five consecutive years, starting from the year of assessment 2020.

This exemption translates into direct tax savings, enhancing the centre's cash flow and providing additional funds that could be redirected towards improving facilities, staff training, or further expansion.

Benefit Analysis

The immediate financial benefit is the preservation of cash that would otherwise be paid as tax. Assuming a corporate tax rate of 15% (concessionary SME rate), the savings amount to approximately RM12,000 for that year alone.

Over the five-year exemption period, assuming steady income, the total tax savings could be significant, providing a substantial financial cushion that can be reinvested into the business.

Conclusion

The government's tax incentives for child care centre and kindergarten operators present a lucrative opportunity for potential investors. By reducing tax liabilities and aiding in the recovery of capital expenditures, these incentives enhance the financial attractiveness and sustainability of investments in the early childhood education sector.

Investors are encouraged to leverage these benefits to contribute to the development of quality child care and education facilities, supporting societal needs and generating substantial returns on investment.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

(Tax Update) Buy Property Under Company or Individual

(Tax Update) Buy Property Under Company or Individual

Buying property under your personal name or through a Sdn Bhd (Sendirian Berhad, which is similar to a Private Limited Company) in Malaysia involves several considerations, including tax implications, liability, financing, and estate planning.

As an approved tax agent, we would guide you through the pros and cons of each approach, tailored to your specific circumstances. It's important to remember that the right choice depends on your financial situation, investment goals, and personal preferences.

Personal Name Purchase

Pros:

-

Simpler process: Generally more straightforward than company purchase.

-

Tax Benefits: Eligible for RPGT exemptions and potentially lower stamp duties, especially for first-time buyers.

-

Better Financing Rates: Often lower mortgage interest rates than those available to companies.

-

Stamp duty : Residential properties purchased worth between RM500,001 to RM1 million will get a 75% stamp duty exemption only up until 31st December 2023.

Cons:

-

Personal Liability: You're personally liable for debts and legal issues.

-

Limited Tax Deductions: Fewer opportunities for deductions on rental income-related expenses.

Sdn Bhd Purchase

Pros:

-

Limited Liability: Shareholders' liability is capped, protecting personal assets.

-

Tax Advantages: Can benefit from tax deductions on property expenses and potentially favorable corporate tax rates. Eligible for Investment Building Allowance (IBA) when leasing as industrial buildings. Watch out S60F Income Tax Act 1967 tax restriction on expenses.

-

Estate Planning: Easier transfer of ownership through shares.

-

Asset Management: Suited for managing multiple properties.

Cons:

-

Higher Costs: Involves setup, annual compliance, and accounting fees.

-

Complex Tax Filings: Must file audited accounts and annual returns.

-

Less Favorable Financing: Lower loan margins compared to individual purchases.

Tax Considerations

-

Rental Income: Non-SME Investment Holding Companies face a 24% tax on rental income.

-

RPGT: Individuals benefit from no RPGT from the sixth year, whereas companies face up to 30% depending on the sale timing.

-

Tax Audit Risks: High-risk profiles may trigger LHDN audits.

-

Industry Building Allowance: Potential tax reduction for property used as industrial buildings.

-

Capital Gain Tax : Be cautious of the new tax implications associated with the transfer of shares.

Loan Considerations

-

Financing: Individuals can secure up to 90% financing for residential properties, while Sdn Bhds may only get up to 60%.

Administrative Expenses

-

Setup and Maintenance: Sdn Bhd entails initial and ongoing costs, whereas personal purchases incur no extra administrative expenses.

Conclusion

Your decision should be informed by a comprehensive analysis considering your financial situation, investment strategy, and goals.

While personal purchases offer simplicity and certain tax benefits, Sdn Bhds provide liability protection and estate planning advantages but come with higher costs and stricter tax treatment on rental income.

Consulting a tax professional or financial advisor is crucial for personalized advice, ensuring your choice aligns with financial goals and legal requirements.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

(Tax Update) Is bad debt tax deductible?

(Tax Update) Is bad debt tax deductible?

Non-trade debts that are written off as bad, or provisions made in respect of non-trade debts that are doubtful, either specific or general, are not deductible in the computation of adjusted income. Similarly, recoveries relating to non- trade debts written off earlier are not taxable.

This tax question has become increasingly common “Should taxpayers use legal action to recover any debts for tax purposes?”.

Let’s talk about the bad debts written off in a tax perspective :

What Is Bad Debts

Debts that are allowed as a deduction in ascertaining the adjusted income of a business is a trade debt that is irrecoverable either wholly or partly. Such debt is written off as bad. Trade debt is a debt that arises from the sales of goods or services and has been included in the gross income of the business.

1. Issue

What is the tax treatment for bad debts?

2. Conclusion

If reasonable steps have been taken to recover the irrecoverable debts but showing there is no

way to recover the debt, the amount of irrecoverable debts is tax deductible.

However, if there are still any other reasonable steps for recovery, such debt cannot be written off

as irrecoverable. Thus, it is not tax deductible.

3. Reasons

For a trade debt to be written off as bad and allowed as a deduction, generally two conditions

are to be fulfilled.

1. The debt shall be an amount that has been included in the gross income of a person for the

basis period for a YA before the relevant YA.

2. The debt is irrecoverable.

To support a claim for deduction of a bad debt written off for tax purposes, there should be

sufficient evidence of such steps taken, including one or more of the following:

a) issuing reminder notices;

b) debt restructuring scheme;

c) rescheduling of debt settlement;

d) negotiation or arbitration of a disputed debt; or

e) legal action (filing of a civil suit, obtaining judgement from the court, and execution of the judgement).

After reasonable steps for recovery have been taken, debt can be considered wholly irrecoverable on the occurrence of any one of the following :

a) the debtor has died without leaving any assets from which the debt can be recovered;

b) the debtor is bankrupt or under liquidation and there are no assets from which the debt can be recovered;

c) the debt is statute-barred;

d) the debtor cannot be traced despite various attempts and there are no known assets from which the debt can be recovered;

e) attempts at negotiation or arbitration of a disputed debt have failed and the anticipated cost of litigation is prohibitive; or

f) any other circumstances where there is no likelihood of cost-effective recovery.

4. Sources

Public ruling no. 4/2019 Tax treatment of wholly & partly irrecoverable debts and bad debts

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Form E 2024 Guidelines

(Tax Update) Form E 2024 Guidelines

What is CP8D?

Form E (also known as Borang E or CP8D ) is a form that allows the employer to all staff particulars to LHDN, this form will have to be submitted to LHDN via the e-Filing method on a yearly basis.

Appointment as Director or Employer or Representative

Effective from Year 2023, Form E and Statement e-C.P.8D are mandatory to submit through e-Filing.

To submit Form E, statement e-C.P.8D and e-CP22 through e-filing is only allowed for the individual who is Employer or Employer Representative only.

The role of Employer or Employer Representative can be added in MyTax for individuals who have a digital certificate.

1. Director (Private Sector , Private Sector other than Company)

This role needs to submit through MyTax include a supporting document

2. Deputy director (Private Sector, Private Sector other than Company)

• Individuals who have role as Director can appoint any individual under the same organization to be appointed as Director representative.

• No need any supporting document

• Approvals are automatic

• Director can terminate the director representative at any time

3. Employer (Private Sector + Private Sector other than Company)

• This role will be given automatically if the application of Director have been approved

4. Employer (Sole Proprietorship , Government Sector, Statutory Body, Local authority)

• This role application can submit through MyTax include a supporting document

5. Employer Representative (All category of employer)

• Individuals who have role as employer can appoint any individual under the same organization to be appointed as employer representative.

• No need any supporting document

• Approvals are automatic

• Employer can terminate the employer representative at any time

Retirement Ages in CP8D

Retirement date shall be determined by retirement age in Malaysia which is 60 years old. For example, date of birth of an employee is 1st January 1990. The retirement date of the employee is 1st January 2050.

For those employees which already reached retirement age, then a contract date shall be determined and declared in CP8D.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Logistics Sector Business-to-Business Service Tax Exemption.

(Tax Update) Logistics Sector Business-to-Business Service Tax Exemption.

Key Summary

The Finance Minister announced that taxes for logistics services won’t apply to certain areas to avoid extra taxing at different levels. From March 1, 2024, a 6% tax was planned for these services, but now the government says the following won’t be taxed:

-

Services for goods sent abroad.

-

Services for moving goods from one ship to another at a port.

-

Services for moving goods through a place without staying there.

-

Door-to-door delivery services.

-

Online delivery of food and drinks.

Businesses in logistics won’t have to pay this tax when they buy the same services from each other.

The government made this change after listening to people’s concerns, including lawmakers, to make sure businesses aren’t paying too much tax when they use different logistics services.

Ministry of Finance Announcement

The expanded scope of exemption was announced by Minister of Finance II Datuk Seri Amir Hamzah Azizan in the Parliament on Monday.

The 6% service tax on the logistics sector was introduced on March 1. Other exemptions on the newly imposed tax include logistics services for transhipment, goods in transit, door-to-door, e-commerce food deliveries, and direct export products.

For newly registered logistics service providers, they will only be imposed the 6% service tax from April onwards, the ministry added.

Source :

Ministry of Finance announcement on SST certain exemption for logistic company

https://www.mof.gov.my/portal/ms/berita/siaran-media/skop-pengecualian-cukai-perkhidmatan-sektor-logistik-diperluas-bagi-mengurangkan-kesan-cukai-berganda

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Understanding MFRS 116 : Accounting on Property, Plant, and Equipment

(Acc Update) Understanding MFRS 116 : Accounting on Property, Plant, and Equipment

Let’s learn MFRS 116, a key accounting standard for buildings, machinery, and equipment. Uncover the crucial guidelines it establishes and understand their impact on businesses globally.

What is MFRS 116?

MFRS 116 is a rule from Malaysia on how to account for property, plants, and equipment (PPE), updating the old rule, MFRS 117.

It tells companies how to recognize PPE as assets if they think these assets will bring future benefits and if they can accurately figure out the costs. This includes adding up all costs needed to get the asset ready for use.

Main Points Explained

Recognizing Assets

MFRS 116 focuses on correctly identifying PPE assets, making sure they will likely bring future benefits and that their costs can be accurately measured. This helps keep financial reports trustworthy, letting others understand a company's assets clearly.

Measuring Costs

After an asset is recognized, its cost is calculated by taking the original cost and subtracting any depreciation (value loss over time) and losses in value. All costs directly related to getting or building the asset are included. This careful calculation helps in making smart decisions and keeps financial reports clear.

Depreciation

Depreciation spreads out the cost of an asset over its useful life. Companies must choose a depreciation method that matches how the asset's benefits are used up over time. This makes sure the asset's value in the books matches its real contribution to the business.

Revaluation

MFRS 116 lets companies adjust the book value of an asset to its current market value, but it's not required. If companies choose to do this, they need to update the values regularly. This option lets companies show the true value of their assets.

Telling Others

Companies must share detailed information about their PPE, including values, depreciation methods, and life spans. This openness helps investors and others understand the company's financial health better.

Example: Updating Equipment Value

Imagine a company with a factory that suddenly becomes more valuable because of new technology. MFRS 116 says the company should update the factory's value in their books to show its true current worth. This shows the rule's focus on keeping financial information up-to-date and reliable.

Why It Matters for Businesses

Following MFRS 116 is important for companies because it affects their financial reports, taxes, and decisions. By sticking to these rules, companies make their financial statements more believable, clear, and trustworthy. This also helps compare different companies more easily, improving analysis within and across industries.

To sum up, MFRS 116 guides businesses in accurately and transparently accounting for their buildings, machines, and equipment. Understanding and applying these rules helps businesses deal with accounting challenges confidently, earning trust from those involved.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Guidelines on Capital Gains Tax for Unlisted Shares

(Tax Update) Capital Gain Tax: Guidelines on Capital Gains Tax for Unlisted Shares

The Inland Revenue Board of Malaysia has issued the Guidelines on Capital Gains Tax for Unlisted Shares dated 1 March 2024 on its website.

The CGT Guidelines explain the CGT treatment on the gains or profits from the disposal of:

a. Shares of a company incorporated in Malaysia not listed on the stock exchange; and

b. Shares of a controlled company incorporated outside Malaysia that owns real property situated

in Malaysia or shares of another controlled company or both.

Key Summaries of the Exemption Order

-

Introduction of CGT under the Income Tax Act 1967 (ITA) effective from January 1, 2024, with implementation starting March 1, 2024.

-

CGT applies to profits from the disposal of capital assets, including unlisted shares of companies incorporated in Malaysia and foreign-controlled companies owning property in Malaysia or shares in other controlled companies.

-

The guideline provides explanations for terms such as ''capital asset,'' ''consideration,'' ''disposal,'' ''stock exchange,'' and ''shares.''

-

Entities liable for CGT include limited liability partnerships, trusts, cooperatives, including Labuan entities subject to tax under ITA.

-

CGT imposition based on the year of assessment in which the disposal transaction occurs.

-

Methodology for determining the disposal and acquisition dates and values of capital assets.

-

Calculation of profits or gains from the disposal of capital assets and the handling of unabsorbed losses.

-

Transfer of capital assets to stock in trade and disposal of shares in relevant companies as per Section 15C of the ITA.

-

Claiming foreign tax credits, the CGT rate, and reporting requirements.

-

Exemptions and conditions under which CGT may not apply or be calculated differently.

Past Blog on CGT

Read our past blog on CGT

-

Capital gain tax https://www.ktp.com.my/blog/malaysias-budget-2024-capital-gain-tax-part1/23nov23

-

Exemption Period on CGT https://www.ktp.com.my/blog/capital-gain-tax-malaysia-2024/04jan24

-

Real property company under CGT https://www.ktp.com.my/blog/real-property-company-under-capital-gain-tax/10jan24

-

Capital Gain Tax: Filing Deadline https://www.ktp.com.my/blog/capital-gain-tax-filing-deadline/30jan24

-

Capital Gain Tax: Unresolved Questions https://www.ktp.com.my/blog/capital-gain-tax-unresolved-questions/23feb24

-

Capital Gain Tax : Gains From Disposal Of Capital Asset Arising From Outside Malaysia Received in Malaysia https://www.ktp.com.my/blog/capital-gain-tax-exemption-foreign-source-income/05march24

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

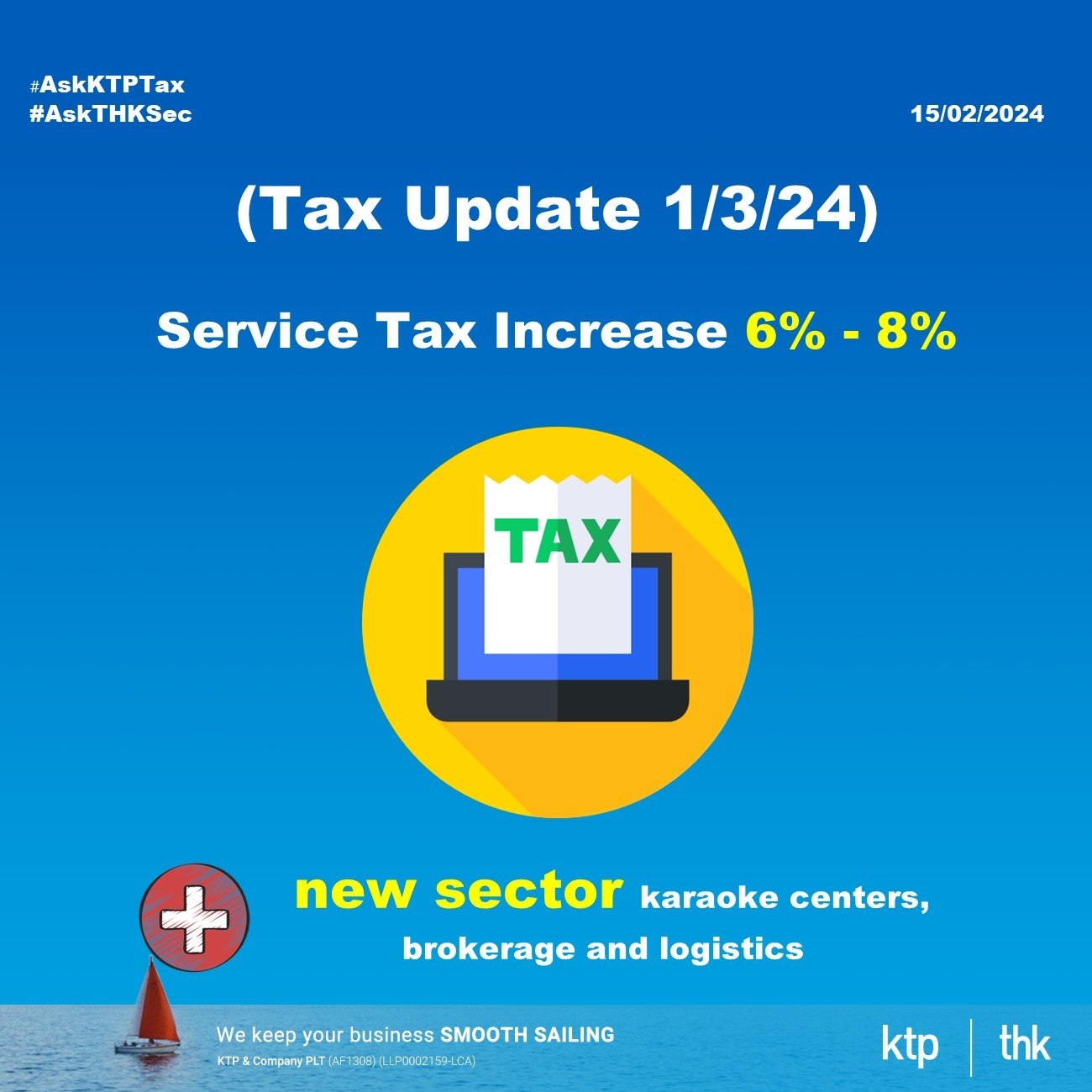

Service Tax Increase To 8%

(Tax Update) Service Tax Increase To 8%

We discuss the service tax rate will increase from 6% to 8% on all taxable services with effect from 1 March 2024, except for F&B, telecommunication services, vehicle parking space services and logistic services.

The scope of service tax will also be widened to include karaoke centre services, delivery services, brokerage and underwriting services, logistics services as well as repair and maintanence, effective 1 March 2024.

Key Summary

Service Tax Rate Increase

-

Starting from 1 March 2024, the service tax rate will go up to 8%.

-

Some services like food, beverages, telecom, parking, and logistics will still be taxed at 6%.

-

Credit card fees will stay at RM25 per card per year.

-

Other services like accommodation, clubs, and professional services will be taxed at 8%.

Transition Rules for the Tax Increase

-

Services provided before 1 March 2024, will be taxed at 6%, but services after that date will be taxed at 8%.

-

If a service spans 1 March 2024, part of it will be taxed at 6% and the rest at 8%.

-

Payments made before 1 March 2024, for services after that date will be taxed at 6% if provided within six months, and 8% if provided after six months.

-

Special rules will apply to businesses offering services taxed at different rates.

Expansion of Taxable Services

-

New services like karaoke centers, brokerage, and logistics will be taxed.

-

Logistics services involve managing the movement and storage of goods and information efficiently.

-

Some services like food delivery and transshipment won't be taxed.

-

Businesses providing logistics services to other businesses will be exempt from tax.

Expansion of Taxable Services - Repair & Maintenance

Royal Malaysian Custom Departments released the Service Tax guidance for maintenance or repair services in Malaysia, as of February 26, 2024. Key points include:

-

Introduction of service tax on maintenance or repair services under the Service Tax Act 2018 from September 1, 2018.

-

Mandatory registration for providers exceeding a threshold, with a focus on maintenance or repair services.

-

Details on taxable and exempt services, including specific examples.

-

Clarification on the tax treatment of various maintenance and repair activities.

-

Guidelines for service providers on registration, tax imposition, and compliance requirements.The government has unexpectedly decided to expand the scope of the sales and service tax (SST) to include almost all types of repair and maintenance jobs.

-

Maintenance management services related to residential land or buildings provided by developers, joint management bodies, management corporations, or residential associations are not subject to service tax.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Form E FAQ

(Tax Update) Form E FAQ

Form E 常见问题呢

阅读我们过去在 Facebook 上的 E/EA 表格上的分享 :

1) Tax Filing Deadline 2022 Malaysia dated on 10/01/2022

2) E呈报(E Filing)Form E 终极秘籍 dated on 15/03/2021

3) 温馨提示 - Form E 截至日期为31/03/2021 dated on 12/03/2021

4) Form EA 有什么? Dated on 22/02/2021

5) 花红几时需要报进Form EA? Dated on 16/02/2021

6) 公司给员工红包可不可以扣税? Dated on 10/02/2021

7) Deadline for Form E submission is approaching! dated on 09/02/2021

是时候呈报𝐅𝐨𝐫𝐦 𝐄了,让我们为您复习一遍!dated on 28/01/2021 各位雇主与员工请注意!!!

9) 你知不知道 ... IRB不再打印+发E表格(Form E) 给雇主! Dated on 25/01/2021

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Capital Gain Tax: Unresolved Questions

(Tax Update) Capital Gain Tax: Unresolved Questions

Introduction

Effective from 1st January 2024, company, limited liability partnership, trust body, and co-operative society which receives gains or profits from the disposal of capital assets consisting of:

-

share of a company incorporated in Malaysia not listed on the stock exchange; or

-

share of a controlled company incorporated outside Malaysia that owns real property situated in Malaysia or shares of another controlled company or both,

are subject to Capital Gains Tax (CGT) under the Income Tax Act 1967.

Exemption Period

Any disposal for the period of 1st January 2024 to 29th February 2024 is exempted from Capital Gains Tax under The Income Tax (Exemption) (No. 7) Order 2023.

The taxpayer is not required to submit a tax return for the disposal of that capital asset within the above period.

CGT Filing and Tax Payment Deadline

IRBM has published Capital Gains Tax Return Form (CGTRF) Filing Programme on 15 January 2024 with key takeaways is summarised as below :

Taxpayers are to submit CGT tax returns and make tax payments within sixty (60) days of the date of disposal.

For assessments raised under sections 91, 96A, and subsections 90(3), 101(2) of ITA 1967, the tax / balance of tax shall be paid within 30 days from the date of assessment. Nevertheless, a grace period of 7 days is given.

Taxpayers are required to submit tax returns through e-Filing (e-CKM Form). Kindly visit MyTax portal at https://mytax.hasil.gov.my to access e-CKM Form from 1st March 2024.

Taxpayers shall have a Tax Identification Number (TIN) and Digital Certificate to access e-CKM.

Unresolved Questions

On January 15, 2024, the Inland Revenue Board of Malaysia (IRBM) shared the filing process for the Capital Gains Tax Return Form (CGTRF) but didn't provide further guidance.

With the new Capital Gains Tax (CGT) beginning on March 1, 2024, the lack of clear instructions has left taxpayers and businesses unsure about how to proceed.

-

The Exemption Order does not change the start date for a lower 2% tax option on unlisted shares bought before 2024. If bought between January and February 2024, future sales are taxed at 10%, not 2%. There might be a ''tax-free'' period due to a technicality, but this wasn't officially announced.

-

Redeemable preference shares' redemption isn't clearly defined as a ''disposal'' for CGT, suggesting future clarification.

-

The term ''real property'' lacks a clear definition for CGT purposes, and it's unclear how the 75% test for foreign company disposals applies over time.

-

Exemptions mentioned previously might be added later. For foreign-sourced gains to be tax-exempt, companies must meet certain economic substance requirements in Malaysia.

-

It's uncertain how losses from domestic and foreign asset disposals are treated for tax purposes, indicating a need for further guidance.

Past Blog on CGT

Read our past blog on CGT

-

Capital gain tax https://www.ktp.com.my/blog/malaysias-budget-2024-capital-gain-tax-part1/23nov23

-

Exemption Period on CGT https://www.ktp.com.my/blog/capital-gain-tax-malaysia-2024/04jan24

-

Real property company under CGT https://www.ktp.com.my/blog/real-property-company-under-capital-gain-tax/10jan24

-

Capital Gain Tax: Filing Deadline https://www.ktp.com.my/blog/capital-gain-tax-filing-deadline/30jan24

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Role of Company Secretary Under The AMLD Malaysia

(Sec update) Role of Company Secretary Under the AMLD Malaysia

What is the Role of the Company Secretary’s play as a reporting institution under the Anti-money Laundering, Anti-terrorism Financing and proceeds of Unlawful Activities Act 2001 (AMLA)?

What is Malaysian AMLA regime?

Before we determine our role, we should understand the meaning of money laundering. Money laundering is a process of converting cash, funds or property derived from criminal activities to give it a legitimate appearance. It is a process to clean ‘dirty’ money to disguise its criminal origin.

How about terrorism financing? It is an act of providing financial support to terrorists or terrorist organisations to enable them to carry out terrorist acts or to benefit any terrorist or terrorist organisation.

Like many other countries, Malaysia government is highly concerned about this area, where money laundering, terrorism financing and proliferation financing pose a significant challenge to the financial system and the overall business sector.

What is The Role of Company Secretary Under AML

Company secretaries are required to comply with Bank Negara Malaysia’s (BNM) Anti-Money Laundering, Countering Financing of Terrorism and Targeted Financial Sanctions for Designated Non-Financial businesses and professions & non-Bank financial institutions policy documents (BNM Policy Document).

Company secretaries are appointed as one of the reporting institutions by Bank Negara Malaysia (BNM), they are playing an important role in this area.

They are required to take the necessary steps to prevent Money laundering / Terrorism Financing and have a system to report suspected transactions to the Financial Intelligence and Enforcement Department (FIED).

Company secretaries have to carry out the following measures to prevent Money Laundering / Terrorism Financing :

-

Compliance with laws

-

Cooperation with law enforcement agencies

-

Establishing internal Control

-

Risk-based approach

-

Customer Due Diligence

A Company Secretary is mandated to conduct CDD on customers when establishing business relations by overseeing transactions. To identify and verify the customer’s identity using reliable, independent source documents, data or information such as identification card.

Additionally, it is crucial to verify the authorization of any person acting on behalf of the customer and confirm their identity. The company secretary must ensure the beneficial ownership’s identity by using reliable information to ensure confidence in their identification.

AMLA Reporting Entity

There are many appointed Reporting Institutions, both in the financial and non-financial sectors.

For examples:

-

Financial Intermediaries,

-

Lawyers,

-

Accountants,

-

Registered Estate Agents, and etc.

All appointed reporting Institutions to work hand in hand with the Malaysian Government and Bank Negara Malaysia to prevent money laundering and terrorism financing, contributing to Malaysia’s brighter future.

PS : Authored by Hui Ting, our secretary associate in THK, in her personal LinkedIn post

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3Rko5kN

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career