Accounting

做账的痛苦

Provision of depreciation

Auditor! Can I don't charge depreciation in my account this year as my company makes loss due to Covid?

I need to borrow money from the bank?

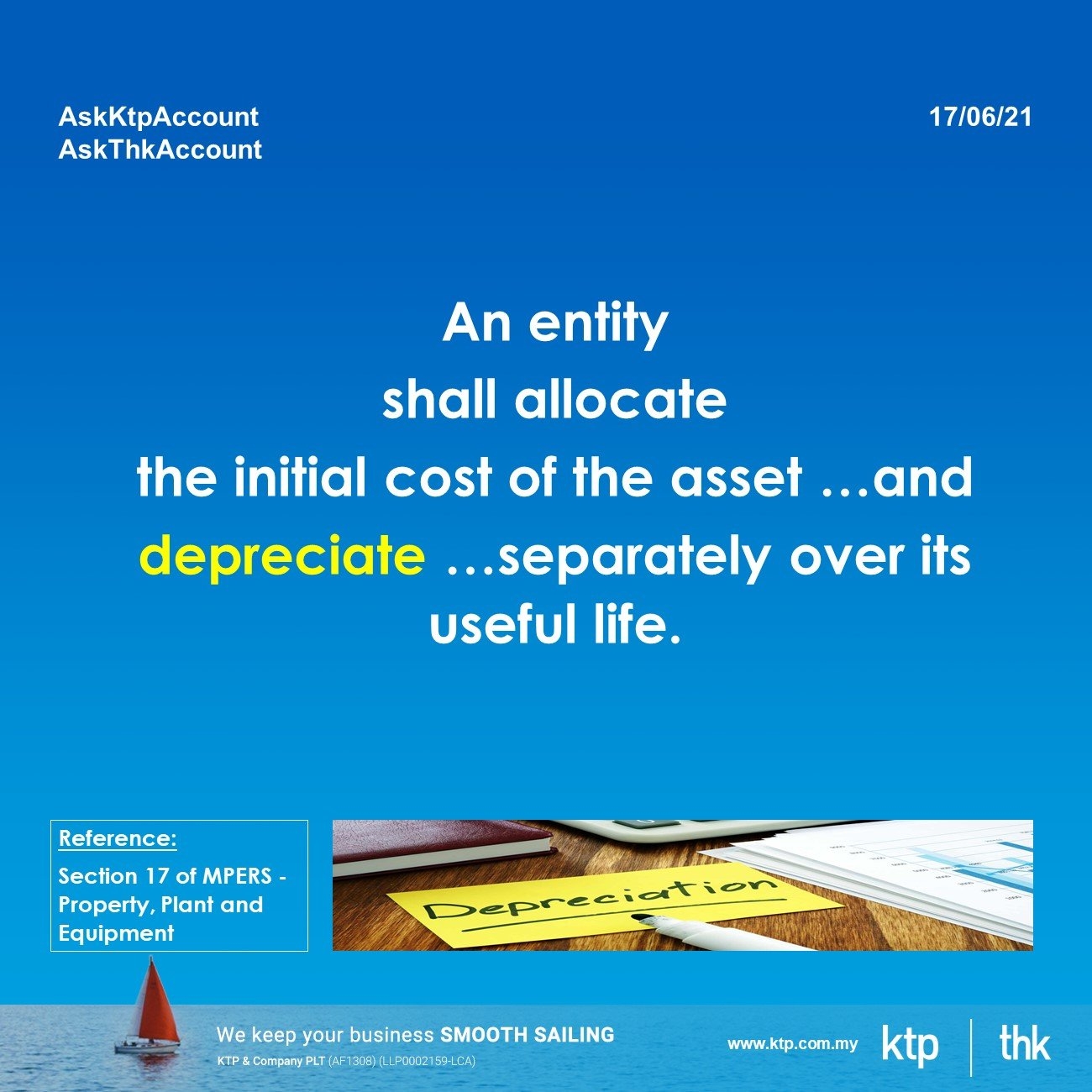

Key summary from the MPERS Section 17 of MPERS -Property, Plant and Equipment

An entity shall allocate the initial cost of the asset …and depreciate …separately over its useful life.

With some exceptions, such as quarries and sites used for landfills, land has an unlimited useful life and therefore is not depreciated.

The depreciation charge for each period shall be recognised in profit or loss…

Depreciation of an asset begins when it is available for use, ie when it is in the location and condition ….

Depreciation of an asset ceases when the asset is derecognized.

Depreciation does not cease when the asset becomes idle or is retired from active use unless the asset is fully depreciated

Auditor opinion :

You still have to charge depreciation in the account!

But …

You can try the following methods and change

* Useful life of assets

* Financial year-end

* Name of company

Visit Us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#irb

#lhdn

What is the difference between Provision and Liability in accounting

Why do auditors keep asking company’s lawsuit status? Why is it so important?

You know the lawsuit is a very slow and irritating one! How I know!

What is the difference between ‘Provision’ and ‘Liability’?

Provision: a liability of uncertain timing or amount.

Liability:

- present obligation as a result of past events

- settlement is expected to result in an outflow of resources (payment)

Provision :

3 criteria are required to be met before a provision can be recognised. These are:

- There needs to be a present obligation (legal/ contractual) from a past event

- There needs to be a reliable estimate (best estimate/ expected value)

- There needs to be a probable outflow (high chance)

What is the difference between ‘Contingent liability’ and ‘Contingent asset’?

These two categories should only be disclosed in financial statements but not recognised in accounts.

Contingent liability :

- a possible obligation depending on whether some uncertain future event occurs, or

- a present obligation but payment is not probable or the amount cannot be measured reliably

Contingent asset :

- a probable asset that arises from past events, and

- whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity.

Example

Contingent Liability:

- Pending lawsuit, product warranty or pending investigation

- The outcome is unknown

- If possible to lose, disclose a contingent liability

- If probable to lose, recognise the provision

Contingent Asset :

- Pending lawsuit, insurance claim

- The outcome is probable

- If probable to receive income (by lawyer or insurance company), disclose contingent asset

- If virtually certain to receive income (subsequently proof by supporting), recognise asset

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

您对公司营业前的费用知道多少呢?

您对公司营业前的费用知道多少呢?

相信很多老板们在营业之前都需要准备一笔筹备费用. 然而,您是否对这些费用在账上面处理的方式有所困惑?

别担心,就让我们给您一个概念吧!

1. 含义- 营业前的费用

营业前的费用 (Preliminary Expenses/Pre-Operating Expenses)

在公司开始运作之前有些费用是务必要花的,这些费用在会计的角度就是营业前的费用。

这些费用基本包括(并不是每个费用将获得扣税资格):

· 市场调查与研究费用

· 律师与秘书费用

· 公司成立的专业的咨询费用

· 招聘与培训员工的费用

· 行政费用等等

2. 复式进账法

Debit 营业前的费用 (Income Statement - Expenses)

Credit 现金 (Balance Sheet - Current Asset)

3. 费用扣税资格与条件

一般上,公司营业前所产生的费用都是无法扣税的。但是某些费用在一定的条件下是可以扣税的。条件如下:

- 该公司必须成立与坐落于马来西亚,商业活动也必须获得财政部长的批准。

例如:市场调查与研究费用,以市场调查为目标的国外交通费与每日不超过四百令吉的国外生活花费都能扣税。

- 该公司的注册法定资本不可超过2,500,000令吉。

例如:注册公司的相关手续费,准备与打印公司章程费,印花税与公司印章费都是可扣税的。

- 生产业公司培训员工的费用可享有双重扣税的福利,但必须达到以下条件:培训费须在营业前发生,培训内容须与产品未来的生产相关,培训计划的机构须获得马来西亚工业发展局(MIDA)与财政部长的批准,培训的员工必须是马来西亚公民。

4. 例子

陈先生于2020年2月15日在马来西亚注册成立,法定资本为500,000令吉。他于2020年4月1日开始从事汽车零件零售业务,并于每年的3月31日作为年度结账。截至2021年3月31日, 该公司的营业前费用有:申请生意上的准证,文书注册,公司章程备忘录及印花税。这些费用总共是4,500令吉。

复式进账法:

Debit 营业前的费用 - 4,500令吉

Credit 现金 - 4,500令吉

这些费用在税务上可进行扣税,原因是这些费用属于可扣税费用与法定资本少于2, 500,000令吉。

欲知更多可参考以下网址:

IRB Public Ruling - PRE-OPERATIONAL BUSINESS EXPENDITURE PUBLIC RULING NO.11/2013

http://phl.hasil.gov.my/pdf/pdfam/PR_11_2013.pdf

Visit Us

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#irb

#lhdn

Acounting standard on revenue

Read the full story in our blog

https://www.ktp.com.my/blog/accounting-for-revenue/11may2021

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏 (𝐀𝐮𝐝𝐢𝐭,𝐓𝐚𝐱, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫

We are one-stop (

What is the difference between director's fee (董事费) and director's remuneration (董事薪金)?

What is the difference between director's fee (董事费) and director's remuneration (董事薪金)?

DIRECTOR FEE

-

The annual fees paid by any employer including retainer fee and meeting fees as compensation for setting on the board of directors.

-

Pay once a year.

-

Require approval at board of director meeting and subsequently approval from the member of meeting.

-

Subject to PCB only.

-

Declare in personal tax.

DIRECTOR REMUNERATION

-

It is the salaries, allowance and bonuses which are paid to director on monthly basis.

-

Pay every month.

-

No need approval, it is base on employment contract.

-

Subject to EPF, SOCSO, EIS, PCB.

-

Require to declare in personal tax.

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

预付款和应计项目您掌握了多少呢? 相信大家在资产负债表里常看到预付款 (Prepayment) 和应计项目(Accrual), 但是您是否知道这两个账目的意义存在?该怎么在账目上呈现呢? 科普时间

预付款和应计项目您掌握了多少呢?

相信大家在资产负债表里常看到预付款 (Prepayment) 和应计项目(Accrual), 但是您是否知道这两个账目的意义存在?该怎么在账目上呈现呢?

科普时间到!让我们带大家一同了解这其中的迷思…

1. 顾名思义:

(a) 预付款

在当年度提前付款下一年的费用。

举个例子:一般上,公司的火险是以一年份的方式付费,公司所偿还的火险保障期已包括了下个年份的费用。

(b) 应计项目

每个月或每年公司应还的费用但是还未付款。

举个例子: 公司每个月都需要偿还电费,但是由于电单在下一个月才收到因此无法在当个月付款。此时我们就必须在当个月应记这笔开销。

2. 在年度报表有什么影响?

(a) 预付款

让公司的年度报表更准确,以便管理层能够做出理想的判断与决定。

这项账目是呈现在年度报表中的流动资产 (Current Assets)。

(b) 应计项目

让公司明确的了解每个月或每年开销的数额,以便预先储备足够的现金以及避免不必要花费。

这项账目是呈现在年度报表中的流动负债 (Current Liabilities)。

3. 何时要输入进或出账目?

(a) 预付款

输入账目:在当下付款时就必须把下个月份或年份的费用归类去预付款的账目。

输出账目:当预付款的日期已达到时就必须把此账目输出到费用的账目。

(b) 应计项目

输入账目:每个月尾或年末时必须把应还但未付款的费用输入到应计项目。

输出账目:在付款的那一天就必须把应计项目输出。

4. 复式记帐法

(a) 预付款

输入账目:

Debit 费用

Debit 预付款

Credit 现金

输出账目:

Debit 费用

Credit 预付款

(b) 应计项目

输入账目:

Debit 费用

Credit 应计项目

输出账目:

Debit 应计项目

Credit 现金

5. 例子

(a) 预付款

公司收到保安公司的账单并在1月时已付款。单据中保安费的日期是从01/01/2021 致 28/02/2021总计RM 120。此时公司必须把1月的费用RM 60输入到保安费(Expenses),2月的预付数额RM 60输入到预付款的账目。当2月时才把预付款中的数额输出到保安费。

(b) 应计项目

公司在每个月为都会在月尾之前计算薪水并支付,但由于这个月的现金流动不是很宽裕。因为此,公司想把这笔薪水RM 12,000 在下个月的5号之前才

公司在每个月都会计算薪水RM 12,000并在下一个月的5号之前才将薪水支付给员工。即使公司还未支付,公司还是必须将当个月的薪水RM 12,000输入到应计项目。直到公司将薪水支付给员工时我们才将这笔费用输出。

欲知更多可参考以下网址: IFRS - Conceptual Framework

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Accounting for bad debts

Do you know what is the difference in Bad Debts, Provision for Doubtful Debts and Bad Debts Recovery?

Due to the impact of Covid-19, the economy has become worse. There are many companies that will face a situation in which the debts cannot be collected.

However, if the companies are unable to collect the debts, what should we do on account?

Don’t worry, let us show you how to do it!

1. Definition:

(a) Bad Debts

- The uncollectible debts from customers.

(b) Provision for Doubtful Debts

- The estimation of future uncollectible debts from customers.

(c) Bad Debts Recovery

- The cash is recovered from bad debts written off previously.

2. What is the document needed to prepare?

(a) Bad Debts

- Issuing reminder notices.

- Legal action

(b) Provision for Doubtful Debts

- The aging report shows customers in slow payment and long outstanding.

(c) Bad Debts Recovery

- The payment slips form customer or Bank receipt.

3. When do we need to do the transaction in account?

(a) Bad Debts

- Once the debts are confirming uncollectible.

(b) Provision for Doubtful Debts

- The debts are overdue but still can be pursued for collection though difficult.

(c) Bad Debts Recovery

- The overdue is received from customers on the bad debts written off.

4. Double Entry:

(a) Bad Debts

Debit Bad Debts Written Off (Expenses)

Credit Account Receivable (Current Assets)

(b) Provision for Doubtful Debts

Debit Allowance for Doubtful Debts (Expenses)

Credit Provision for Doubtful Debts (Current Liabilities)

(c) Bad Debts Recovery

Debit Cash at Bank (Current Assets)

Credit Bad Debts Recovery (Income)

5. Example:

Example 1:

In year 2021, Company A’s account receivable is RM 100,000.00 and RM 10,000.00 is uncollectable due to the customer is bankrupt.

Answer:

The journal entry is debit Bad Debts RM 10,000.00 and credit Account Receivable RM 10,000.00.

Example 2:

In year 2020, Company A's account receivable amounted to RM 200,000.00. Company A decided to provide 5% for doubtful debts on the year.

Answer:

The journal entry is debit Allowance for Doubtful Debts RM 10,000.00 (RM 200,000.00 X 5%) and credit Provision for Doubtful Debts RM 10,000.00 in year 2020.

Example 3:

In year 2021, customer paid RM 1,000.00 to Company B for a debt which had already been written off as bad debts in year 2020.

Answer:

The journal entry is debit Cash RM 1,000.00 and credit Bad Debts Recovery RM 1,000.00 in year 2021.

You may refer to the link for more information of tax treatment on bad debts: Is Provision of Bad Debts eligible for tax deduction?! Is Provision of Bad Debts tax deductible?

Case Study on the Transition of MFRS 16 Leases

Case Study on the Transition of MFRS 16 Leases

Background

ABC Sdn Bhd's financial statement is in accordance of Malaysian Financial Reporting Standards (MFRS).

The Company has signed a 5 years tenancy agreement since Year 2018 for the warehouse used in its business.

Struggles

The accountant of the Company is wondering whether

Ø They should apply for MFRS 16 Leases to comply the Standards?

Ø What is the corrective action if they fail to comply in Year 2019?

Ø What is accounting entries to recognise the MFRS 16 Leases?

Q1: They should apply for MFRS 16 Leases to comply the Standards?

Solution Exemption requirement

The Company can elect not to apply only if the lease contract is:-

1. Short-term lease

- less than 12 months

2. For low value assets

- Not highly dependent on, or highly interrelated with other assets

- Benefit from use of assets on its own or together with other sources that are readily available to the lessee

If the Company is not exempted, it has to apply the Standard and determine the following items:-

1. Discount rate

- Implicit interest rate; or

- Incremental borrowing rate

2. Application method

- Retrospectively to each prior reporting period; or

- Retrospectively with the cumulative effect

Q2: What is the corrective action if they fail to comply in Year 2019?

Solution The Company has to do the restatement of its financial statement for the reporting period by applying MFRS 129 Financial Reporting in Hyperinflationary Economies.

Q3: What is the accounting entries to recognise the MFRS 16 Leases?

Solution The accounting entries for recognition of right-of-use assets and lease liability will be as follow:-

Dr. Right-of-use assets

Cr. Lease liability

Dr. Depreciation

Cr. Accumulated depreciation

Dr. Interest on lease liability

Cr. Lease liability

Dr. Lease liability

Cr. Bank/Cash

Source:

MFRS 16 Leases https://www.masb.org.my/pdf.php?pdf=BV2018_MFRS%2016.pdf&file_path=pdf_file

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Latest update on accounting for lease

The development on accounting for lease

Effective from 1 January 2019, IAS 17 Leases will be replaced by MFRS 16 with the following changes.

- The leases are no longer classified into operating leases or finance leases

- All leases are capitalised by recognising a lease liability and the right to use of assets on balance sheet.

This means that the Company which takes up leases that only allows the right of use of asset, and not the ownership of assets, will also need to recognise its right to use the assets (Asset) first, and later on expense off to the interest (Expenses) and depreciation of the assets (Expenses).

This affects the balance sheet of the company as the old accounting standards only requires Company to disclose these leases on the profit and loss.

The new standard on MFRS 16 and the effect on financial statements are as follows:-

- A ‘right-of-use’ model replaces the ‘risks and rewards’ model.

- Lessees should recognise an “right-of-use” asset and lease liability based on the payment under lease

- The lease liabilities must be measured to the lease term (optional lease period)

-

Lessees should reassess the lease term only upon the occurrence of a significant event or a significant change in circumstances that are within the control of the lessee

Double entry of accounting for leasing

For leases that allows right of use but the lessee does not have ownership at the end of the lease(i.e. renting an asset), the new accounting standard requires Company to recognise the lease on the assets and liability on balance sheet. So, at the commencement of lease, based on the contract of rental, the lessee will need to present the contracted rental payment as follows:

- Dr Right of use of asset

- Cr Lease liability

The asset and liability will be slowly reduced when the payment are made, as the company will expense off these expenses to profit and loss (i.e. interest paid, rental expenses/depreciation).

- Dr Lease liability

- Dr Interest paid

- Dr Rental expenses paid

- Cr Cash at bank paid

- Cr Right of use of assets

Recognition of lease

To recognize the right of use and lease liability by:

Right of use – measured by cost /fair value/ revaluation method

- obtain substantially all of the economic benefits from the use of the identified asset throughout the period of use

- direct the use of the identified asset throughout that period

Lease liability – Lessee needs to recognize on interest of lease liability

- there is an identified asset

- has the rights to all of the economic benefits from that asset

- directs the use of that asset, including how and for what purpose

Exemption

There has two specific exemptions where leases do not need to be reported on balance sheets:

- Leases with a term of 12 months or less with no purchase option

- A lease where the value of the item is low value.

Sources

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our job platform for interns, graduates & experienced candidates )

𝐓𝐇𝐊 (Our associate in secretarial & accounting services)

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#accountingstandards

#mfrs16

#masb

Construction Accounting Q&A Part 2 - Key Components

Confused over construction accounting. Q&A Part II - Key Components

Today we cover Q&A #2 on key component in the construction accounting following our first sharing on the business cycle in last week.

Next is the accounting standard on the construction account.

Key Components in Construction Accounting

1. What is progress bill?

2. How to calculate the % of Completion?

3. How to recognize revenue?

4. What kind of costs may incur for a construction?

5. How to recognize cost?

6. What is retention sum?

7. What is amount due from/to customer?

Visit us www.ktp.com.my

Visit us www.thks.com.my

Construction Accounting Q&A Part 1 - Business Cycle

Confused over contract accounting. Wait no more!

We will run a series of our training note to our clients and new colleagues on contract accounting.

Today we cover Q&A on business cycle in contract accounting.

In general these 11 steps are common in the construction accounting.

Step 1 : Tender a project

Step 2 : Negotiate with customer

Step 3 : Enter agreement (if applicable)

Step 4 : Engage with sub-contractor

Step 5 : Start construction

Step 6 : Receive progress claim from sub-contractor

Step 7 : Verify the work done completed by sub-contractor

Step 8 : Send progress claim to customer

Step 9 : Customer verify the work done

Step 10 : Obtain progress claim certificate from customer

Step 11 : Issue invoice to customer

Visit us www.ktp.com.my

Visit us www.thks.com.my