Blog

What is Company Secretary?

What is Company Secretary?

A Company Secretary is a senior position in a citizen sector establishment. Also known as Compliance Officers, it is one of the positions that is a part of the key managerial personnel (which usually includes the CEO & CFO) of any company.

In large American and Canadian publicly listed corporations, a Company Secretary is typically named a Corporate Secretary.

A Company Secretary is responsible for the efficient administration of a company, particularly with regard to ensuring compliance with statutory and regulatory requirements and for ensuring that decisions of the board of directors are implemented.

Roles of Company Secretary

A. Helps you with starting a Company (incorporation),

He/she provides you with advice in terms of corporate restructuring, mergers, acquisitions, complying with good corporate governance

B. Advise you on other laws and regulations compliances such as tax issues, business licenses, EPF, Socso, and EIS contributions.

C. Attend and arrange Board or Members Meetings.

He/she assists you in drafting the Agenda, and sending out the notice to ensure that the meeting is properly called, constituted, and carried out according to the laws.

D. Ensure the Company complies with the rules set out in the Companies Act, 2016.

E. Maintain Statutory Records for the Company.

He/she is to ensure that the Company register books are recorded up to date, as well as the records books are kept for a period according to the requirements of the laws.

F. Handle and arrange the Company’s Annual General Meeting.

He/She ensures that the meeting is carried out properly during the whole process of the meeting.

He/She prepares the minutes of the meeting once the meeting is adjourned.

G. Prepare and file the Company’s annual return and audited financial statements with the Directors’ reports.

He/she ensures that the Company is in compliance with these deadlines.

H. Update and maintain the Company’s Statutory Books and documents.

The Company details such as directors, shareholders, paid-up capital, shares and constitution will be changed from time to time.

He/she is responsible for notifying the registrar of the changes and updating all related records.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Audit Exemption Malaysia

Document Required for Audit Exemption

After our sharing on the qualifying criteria for audit exemption, let us further share more information on the documents required for submission of unaudited financial statements to Suruhanjaya Syarikat Malaysia (SSM)

Question :

Do the Company still require to submit a financial report to SSM even though the company is qualified for audit exemption?

Yes, the company is required to prepare the financial statement for submission to SSM.

What are the documents for the submission of the financial statement?

1. Audit Exemption Certificate

In compliance with Section 258 and Section 259 of the Companies Act 2016.

2. Unaudited Financial Statements

In compliance with applicable approved accounting standards.

3. Directors’ Report, Statement by Directors, and Statutory Declaration Under Section 251 and Section 252 of the Companies Act 2016.

Source

For more information on Practice Directive No. 3/2017

-

https://bit.ly/3Bgm0Pf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Double submission of statutory form to Suruhanjaya Syarikat Malaysia (SSM)?

Double submission of statutory form to Suruhanjaya Syarikat Malaysia (SSM)?

A situation that may encounter on double submission:

• The director of the company submitted the form to SSM (usually over the counter at SSM office) in his/ her capacity without informing the company secretary.

• Appointed Company Secretary submits the same form via SSM system.

The consequences of double submission?

• SSM issued a letter to query both persons (director and secretary) on the submission of the form.

Under some circumstances, the director of the company may not receive the queries from SSM.

Click on this link to retrieve the query:: Pages - e-query (ssm.com.my)

Who to solve the problem?

• Director; or

• Appointed Company Secretary.

How to solve the problem?

1) Cancellation

Cancel the previously submitted form by a notice of withdrawal to SSM with a payment of RM500.00 to SSM.

2) Re-submission after cancellation

Submit again the form by either one of the persons (director or secretary)

3) Follow up

To ensure the completion, need to follow up and check the status via mydata or e-info system to ensure that the form appears in the document listing.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

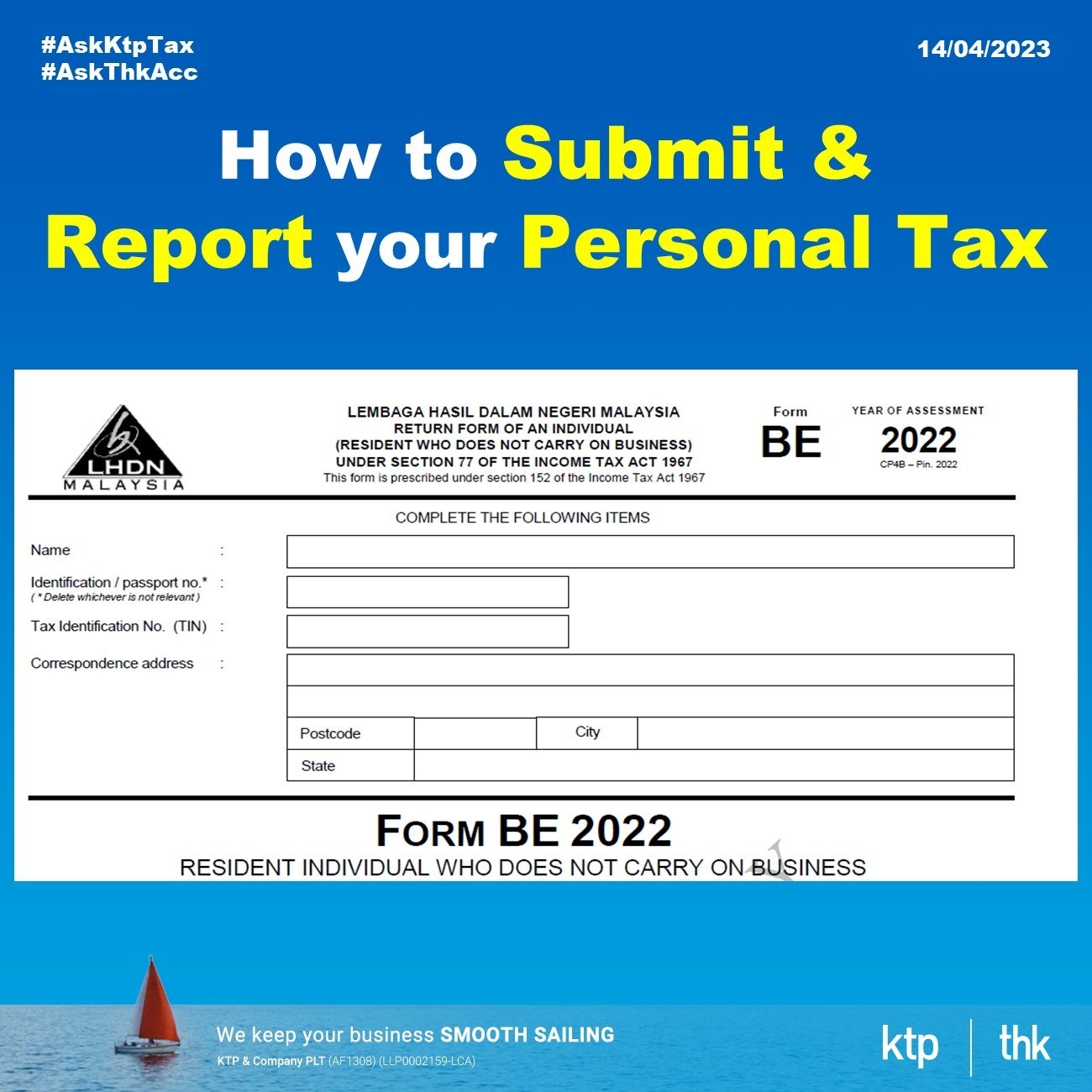

How to file personal income tax?

How to file persona income tax?

Taxpayers can start submitting their income tax return forms through the e-Filing system starting from March 1 of every year, unless otherwise announced by LHDN.

This method of e-filing is becoming popular among taxpayers for its simplicity and user-friendliness.

If this is your first time filing your tax through e-Filing, don’t worry, we’ve got your back with this handy guide on e-Filing.

Step by step

-

Log into mytax.hasil.org.my

-

Choose “Identification Card No”

-

Complete it and click submit

-

Choose e-CP55PD on the first timer if the digital certificate is not displayed.

-

Fill in your email address, upload IC, and click submit

-

You will receive IRB notification within five (5) working days.

-

Follow step 2 and 3

-

Mytax dashboard will be displayed

-

Click ezHasil service and select e-filing

-

Choose the Form

-

Select Tahau Taksiran

-

Complete Part 1, 2, 3, 4 and 5

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

How to check personal income tax numbers online?

How to check personal income tax numbers online?

Step 1 : Go to https://mytax.hasil.gov.my

Step 2 : Click “E-draft”

Step 3 : A new page will emerge.

Step 4 : Select “Individual”

Step 5 : Fill in email & phone number. Fill in security phase and click Search

Step 6 : Get your income tax number

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

RMDC Remission Program 2023

RMDC Remission of Penalty & Surcharge

The Royal Malaysian Customs Department (RMCD) has announced Remission Program 2023 on Penalty and Surcharge in their website banner.

Key Summaries of the Remission Program

-

Full payment must be made.

-

The Bill of Demand (BOD) is issued for taxable period on or before 31 December 2022.

-

For cases registered with court, company/ individual is required to inform Civil Officer handling the case by writing in order to participate in this program ( T&C apply).

-

This program is also offered to company/ individual who has received approval to pay outstanding taxes by instalment.

-

The amnesty program run from 1 February 2023 to 30 September 2023 (8 months)

Our Takeaways

Is this Special Voluntary Disclosure Program (SVDP) which is scheduled to start in June 2023?

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

How to submit personal income tax Malaysia?

How to submit personal income tax 2023

Audit Exemption - A higher threshold in qualifying criteria for exemption from audit

New Proposed Audit Exemption for Sdn Bhd Malaysia

Audit Exemption - A higher threshold in qualifying criteria for exemption from audit

Background

This article relates to the qualifying criteria for the Audit Exemption (AE) that we published on 8 February 2022.

Suruhanjaya Syarikat Malaysia (SSM) issued a Consultative Document on the Proposed Review of AE Criteria for Private Companies in Malaysia on 2 February 2023 with the purpose to seek public response and feedback upon the proposal of new thresholds for the following categories:

1. Zero-Revenue Companies

• Turnover: No changes as remain at RM0

• Total Assets: Increase from RM300,000 to RM500,000 for the current financial year and the immediate past 2 financial years.

2. Threshold-Qualified Companies

• Turnover: Increase annual revenue from RM100,000 to RM1,000,000 during the current financial year and the immediate past 2 financial years.

• Total Assets: Increase from RM300,000 to RM1,000,000 for the current financial year and the immediate past 2 financial years.

• Employees: Increase from not more than 5 to not more than 30 employees at the end of its current financial year and immediate past 2 financial years.

SSM remains the same threshold for Dormant Companies category.

SSM Findings

From the Consultative Document (CD), SSM considered the following in formulating the above proposal:

1. SSM analysis on data available as at 30 November 2022

From Table 2 and Table 3 of the CD, the statistics reflected the overall percentage of AE submissions at a very low rate since the introduction in the year 2017.

Financial Year Ended (Rate)

2020 6%

2019 7%

2018 4%

SSM Explanation

Tag along in the analysis rate, SSM also listed 4 possible reasons for the low rate summaries as below :

a. awareness on the eligibility for AE;

b. procedure imposed by related bodies (such as licensing and regulatory authorities, banks) which require audited Financial Statement;

c. Company Directors' option to submit the audited Financial Statement; and

d. Other factors - limitation of data on the number of employees cause the requirement to submit the audited Financial Statement.

2. Findings of a survey

The Malaysian Institute of Accountants (MIA) conducted a survey in the year 2021 on “The Impact of Audit Exemption on Small Companies and Audits Firms.

MIA reported their findings summaries as below:

a. reasons to option for AE or not; and

b. the majority of respondents agreed to increase the threshold.

3. SSM comparative study in other 3 jurisdictions (United Kingdom, Australia and Singapore) on the trend of AE.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

(update) Corporate Income Tax Rate for SME

Corporate Income Tax Rate for SME

Tax Rate - Companies

Resident companies are taxed at the rate of 24% while those with paid-up capital of RM2.5 million or less*, and gross business income of not more than RM50 million (strictly all business sources) are taxed at the following scale rates:

-

SMEs will have a reduced corporate income tax rate of 15% for the first RM150,000 ringgit chargeable income.

-

SMEs earning between RM150,00 to RM600,000 on the first chargeable income will be charged at 17%, and

-

Balance (those earning more than RM600,000) will be charged the 24% tax rate.

* none of its related companies within the group ( by way of shareholding of more than 50%) paid up share (ordinary) exceeding RM2.5 million.

Definition of SME for Tax Purpose

SME companies are defined

-

Paid-up share capital not exceeding RM2.5 million

-

Gross income (business source) not exceeding RM50 million

New Ruling on Foreign Shareholders (wef Year of Assessment 2024)

With effect from YA 2024, one more condition for SMEs to enjoy the preferential tax rate

If more than 20% of paid-up share capital is owned by a foreign company or non-Malaysia citizen, SME will not entitle to 15% and 17% preferential tax rate.

Tax Implication on Foreign Shareholding More Than 20%

Taxpayers will be subject to a 24% tax rate if the foreigner owns more than 20% shareholding.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

What is LLP in Malaysia?

What is LLP in Malaysia?

The Limited Liability Partnership (LLP) is an alternative business container regulated under the Limited Liability Partnership Act 2012 which incorporates the characteristics of a company and conventional partnership.

What is LLP (Limited Liability Partnership)?

1. Combination of a company and conventional partnership.

2. It’s governed under LLP Act 2012

Who does the registration of LLP?

Compliance officer - he/she may also be one of the partners of the LLP.

Where can register an LLP?

Registrar (SSM) - The compliance officer may log in to MyLLP portal to do registration

How to register an LLP?

Requirements

a) name of LLP

b) nature of business

c) registered office of LLP

d) partner’s details

e) compliance officer’s details

f) approval letter from the governed body (if any)

g) others relevant infomation

How to register an LLP?

Registration procedure

a) Either one of the partners will be appointed as a compliance officer.

b) he/she shall go to SSM office to do identity verification purposes to activate the portal account.

c) the registration of LLP will submit via MyLLP portal by the compliance officer.

d) reserve of LLP Name (SSM) must approve your name before you can register it).

e) you need to register the LLP within 30 days.

What documents do you get after registration?

- Company’s profile

- Certificate of registration

***the documents will be issued by SSM upon request together with the prescribed fee.

What are the registration fees for LLP?

There is a registration fee of RM500 to be charged by SSM

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Can I reuse a company name after strike off from SSM?

Can I reuse a company name after strike off from SSM?

On 30 January 2023, Suruhanjaya Syarikat Malaysia (SSM) issued a guideline related to the application to Court to reinstate the name of the company under Section 555(1) of Companies Act (CA), 2016.

This guideline is useful to the public (especially Company Directors) who felt upset by SSM's decision to strike off their company under Section 549.

SSM Power To Strike Off

This section gives SSM the legal power to strike a company off in the registrar where the company:

(a) is not carrying on business or operation;

(b) has contravened any of this act;

(c ) is being used for unlawful purposes; and

(d) is being wound up.

This reinstatement is applicable within 7 years after the name has been struck off by SSM.

How does it work?

Application process according to

1) Order 88 rule 2 of the Rules of Court 2012; and

2) Section 555 of CA, 2016.

The proceeding shall be commenced by the applicant (ie Plaintiff) to file in court an originating summons (“Originating Summons”).

The Originating Summons needs to be supported by an Affidavit in Support (“Affidavit”) setting out the grounds and evidence in support of the application.

General Guidelines

The Guidelines about the application for reinstatement under Section 555 of CA 2016 are summarised below: -

1. The Defendant: SSM is to be named as the defendant in the application;

2. Contents of the Affidavit:

The Affidavit must include the following: -

a) Info on the directors of the Company;

b) Info on the shareholders;

c) Consent letter from the other directors;

d) Address of the registered office;

e) Ground of the application; and

f) Other necessary and relevant facts (for example Annual Return and Financial Statement to prove that the company is in existence and operation or bank transaction reflected in the bank statement or there is the existence of ownership of assets).

The orders sought from the Court must include:

a) The Plaintiff lodges the overdue statutory documents not submitted previously such as Financial Statements, Annual Return and other related documents if any;

b) The cost of the proceedings of RM2,000 be paid by the plaintiff within 30 days of the order made;

c) An order that the cost of the application is borne by the plaintiff.

As the result, SSM may oppose an application that does not fulfill the requirements and the court ultimately has the discretion of whether or not to allow an application for reinstatement under Section 555 of CA 2016 to have proceeded.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

How to set up a company in Malaysia?

KTP Get-Connected Session @ 31/03/23

-

Topic : How to set up a company in Malaysia?

-

Date : 31/03/23

-

Time : 10:30am

-

Location : Live Interview

-

Speakers : Jasmine Ma

-

Moderator : Koh Teck Peng

Proposed Agenda :

1) What company name you want your company to be called?

2) What words/symbols are prohibited by SSM for you to use?

3) How many directors do you want your company to have?

4) How many shareholders will your company have?

5) Does a company need a secretary?

6) What is the nature of the business of your company?

7) What is your company's paid-up capital?

8) How long for the whole process of incorporation?

9) & more

Recorded Webinar on YouTube

Stay tuned for the recorded webinar on our YouTube in the coming days.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

How to close LLP in Malaysia ?

How to close LLP in Malaysia ?

Dissolution of Limited Liability Partnership

Section 50 of the Limited Liability Partnership (LLP) Act 2012 shall apply to a voluntary winding-up of a Limited Liability Partnership. S.51 of the LLP Act 2012 Power of Registrar to strike-off limited liability partnerships from the register is reserved for the Registrar.

3 options for closure:

1) Compulsory winding-up by Court

2) Voluntary winding up by partners (Preferable option)

3) Strike-off by SSM.

When partners of LLP do not wish to continue the business or have no successor to take over the entity, the partners may opt to close the entity by Voluntary Winding Up (VWU).

The basic requirement for Voluntary Winding Up (VWU)

Section 50(2) of LLP Act, 2012 required the LLP has:

1) ceased to operate and

2) discharged all its debts and liabilities

Who can apply?

1) Any one of the partner

2) Compliance Officer

with an authorised user to access MyLLP under SSM4U system

Application process with SSM to effect the VWU

-

Part A – Pre-application

-

Part B – Application

-

Part C – Post application

Part A - Pre-application process

As per Section 50(4) of LLP Act, 2012 and Item 4 in SSM Guideline

1) Send a notice to all partners by registered post;

2) Send and obtained a written notice of clearance and no objection from Inland Revenue Board (IRB) of Malaysia; and

3) Publish a notice in Malaysia newspaper as per Appendix A and B in

a. national language; and

b. English language

Part B - Application process

As per Section 50(3) of LLP Act, 2012 and Item 9 in SSM Guideline

1) Submit the application via MyLLP within 7 days upon compliance with Part A together with the following documents:

a. Statutory Declaration as per Appendix C;

b. copy of the notice sent to all partners;

c. written notice from IRB; and

d. copy of the notice published in the newspaper

Part C – Post application process

As per Section 50(7),(8) and (9) of LLP Act, 2012 and Item 14 to 16 in SSM Guideline

1) SSM will notify the applicant in writing on

a. declare that the LLP is dissolved if no further objection and withdrawal; and

b. entitlement to distribute its surplus assets (if any) among partners under the LLP agreement.

2) The applicant required to notify SSM of the completion of the distribution of surplus assets within 14 days to effective and complete the application process.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

延长国家教育储蓄计划 (SSPN) 的个人所得税减免

延长国家教育储蓄计划 (SSPN) 的个人所得税减免

这项延长措施将导致政府一年减少约 2亿5000万令吉的收入. 一个人在评估年度内为其孩子存入 SSPN 可获得最高 RM8,000 的所得税减免 (因当年的任何提款而减少).

原定于 2020 年到期 的减免已延长至 2022 年

什么是SSPN?

• 它是一个国名教育储蓄计划

• 为了鼓励父母们培养良好的储蓄习惯,提早为孩子准备教育基金

SSPN 是国家高等教育储蓄机构 (PTPTN) 推出的储蓄计划. PTPTN 是根据 1997 年国家高等教育管机构法 [第 566 号法案] 成立的.

SSPN 的推出是为了让父母能够储蓄并最终资助他们的孩子在高等教育机构的教育。 为了鼓励个人向 SSPN 账户存款,引入了 ITA 第 46(1)(k) 段,允许对向该计划存款的个人进行扣除.

从 2012 年至 2018 年课税年起,允许扣除的金额是相关年度的净捐款,上限为 6,000 令吉。从 2019 课税年起,净捐款的最高扣除额增加至 8,000 令吉.

净贡献是一年中的存款数额减去当年的任何提款数额。

SSPN 账户可以由父母为 18 岁及以下的孩子开立,并维持该账户直到孩子年满 29 岁.

父母在孩子年满 29 岁之前存入此账户的存款可作为扣除额。

对于 18 岁及以上的儿童,他们可以选择以自己的名义或以父母的名义开立账户。 如果账户是以孩子的名义开立的,则该孩子没有资格从账户中的存款中扣除,因为根据 ITA 第 46(1)(k) 段的扣除仅适用于作为父母的存款人或 监护人。 父母也没有资格扣除,因为他们不是以孩子的名义开设账户的存款人。

SSPN-I & SSPN-I Plus的分别

SSPN-I 就是现在所谓的SSPN Prime

• 纯储蓄的存款计划

• 存款者无需每个月固定存款

SSPN-I & SSPN-I Plus的分别

SSPN-I Plus就是现在所谓的SSPN Plus

• 它类似是储蓄保险配套, 可享有人寿保险,36种疾病医药保障,住院补贴等等。

SSPN可以扣税吗?

• SSPN-I 税务减免高达RM8,000

• SSPN-I PLUS 则分成两个部分

(i) 净存款 – 税务减免高达RM8,000

(ii) 人寿保险 – 税务减免高达RM3,000

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

(Special Update) Postponement of Sales Tax On Low Value Goods

Last Friday, the Royal Malaysian Customs Department announced that the implementation of sales tax on Low Value Goods (LVG) which was initially intended to be implemented with effect from 1.4.2023 has been postponed to a later date.

Kindly refer to RMCD announcement here: https://lnkd.in/efyFBzpm

Read our past KTP blog posting on LVG

https://lnkd.in/gai_vJRY

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏 (𝐀𝐮𝐝𝐢𝐭,𝐓𝐚𝐱, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

Website www.ktp.com.my

Instagram https://bit.ly/3jZuZuI

Linkedin https://bit.ly/3sapf4l

Telegram http://bit.ly/3ptmlpn

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

Website www.thks.com.my

Facebook https://bit.ly/3nQ98rs

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞

An internal community for our colleagues on work and leisure.

Tiktok http://bit.ly/3u9LR6Q

Youtube http://bit.ly/3ppmjyE

Facebook http://bit.ly/3ateoMz

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

Instagram https://bit.ly/3u2PxHg

Facebook http://bit.ly/3rPxz9o

#KTP

#thk

#ktplifestyle

#ktpcareer

#LVG #tax

Tax Budget 2023 - Webinar

Tax Budget 2023 - Webinar

-

Topic : Tax Budget 2023

-

Date : 10/03/23

-

Time : 2.00pm

-

Location : Live Interview

-

Language : Chinese

-

Speakers : Chong Yew Jia & Teo Mei Qi

-

Moderator : Koh Teck Peng

Proposed agenda :

Prime Minister and Finance Minister Datuk Seri Anwar Ibrahim have proposed some changes to the income tax rates under the new Budget 2023.

Key summary on tax budget 2023 for

-

Individual

-

Corporate

-

Indirect Tax

-

Others (Capital Gain Tax, Luxury Goods Tax, SVDP)

Webinar

Watch the full video (45 minutes) in the YouTube

https://youtu.be/k4XBq8rzZoE

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Tax Budget 2023 - Others

Tax Budget 2023 - Others

Prime Minister and Finance Minister Datuk Seri Anwar Ibrahim have proposed some changes to the income tax rates under the new Budget 2023.

Key summary on tax budget 2023 for Others

Capital Gain Tax

The proposal to introduce a capital gains tax (CGT) on the disposal of unlisted shares has been welcomed as a move in the right direction by economists but a tax expert has cautioned a more in-depth study is needed.

The proposal is a sign the government is kickstarting its move to impose taxes on more capital items in the future.

Tricor Malaysia chairman Veerinderjeet Singh opines the government would have in theory three mechanism options for CGT implementation.

“Either a new legislation on CGT will be introduced, or the existing legislation on real property gains tax (RPGT) will be amended to include the sale of shares of unlisted companies, or it will be added within the Income Tax Act by defining it to include certain capital gains, which can be reported annually.”

Luxury Goods Tax

A luxury tax is a tax imposed on goods that are considered expensive, unnecessary and unimportant. Such items include cars, private jets, yachts and jewellery.

Retabling the budget in the Dewan Rakyat last week, Anwar who also holds the finance portfolio said that the government had no plans to reintroduce the goods and services tax (GST).

In Norway, cars and chocolate alike are considered a luxury and subject to a luxury tax.

Let’s see how the government come out with detailed implementation in the coming months.

Special Voluntary Disclosure Program (SVDP)

The IRB and RMCD will implement the SVDP again. Under the SVDP, a 100% penalty remission will be granted with effect from 1 June 2023 to 31 May 2024.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Tax Budget 2023 - Indirect Tax

Tax Budget 2023 - Indirect Tax

Prime Minister and Finance Minister Datuk Seri Anwar Ibrahim have proposed some changes to the income tax rates under the new Budget 2023.

Key summary on tax budget 2023 for Indirect Tax

Extension of Exemptions on Purchase of EV

• Full import duty exemption on components for locally assembled EV

Until 31 December 2027

• Full excise duty and sales tax exemptions on locally assembled CKD EV

Until 31 December 2027

• Full import duty and excise duty exemptions on imported CBU EV Until 31 December 2025

Expansion of Excise Duty and Sales Tax Exemptions on Sale, Transfer, Private Use or Disposal of Individually Owned Taxis and Hired Cars

• Excise duty and sales tax exemptions on the sale, transfer, private use or disposal of individually owned taxis and hired cars are expanded to include taxis (budget taxis, executive taxis and TEKS1M), airport taxis (budget and family) and hired cars.

• The vehicle age condition is relaxed to at least 5 years from the date of registration.

• For applications received by the RMCD from 1 March 2023.

Imposition of Excise Duty on Gel or Liquid Products containing Nicotine

• Excise duty to be imposed on gel or liquid products containing nicotine used for electronic cigarettes and vaping.

• Effective date and applicable rate yet to be announced.

Import Duty and Sales Tax Exemptions on Nicotine Replacement Therapy

• Import duty and sales tax exemptions on nicotine gum and nicotine patch for a period of 3 years.

• For applications received by the MOF from 1 April 2023 to 31 March 2026.

Import Duty and Sales Tax Exemptions on Studio and Filming Production Equipment

• Import duty and sales tax exemptions on studio and filming production equipment to providers of studio equipment, production and post- production services for a period of 3 years.

• For applications received by the MOF from 1 April 2023 to 31 March 2026.

Extension of Import Duty Exemption for BioNexus Status Company

• Import duty exemption on raw materials/ components and machinery/equipment for BioNexus Status Company to be extended for 2 years.

• For applications received by Malaysian Bioeconomy Development Corporation from 1 January 2023 until 31 December 2024.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

Tax Budget 2023 - Corporate

Tax Budget 2023 - Corporate

Prime Minister and Finance Minister Datuk Seri Anwar Ibrahim have proposed some changes to the income tax rates under the new Budget 2023.

Key summary on tax budget 2023 for Corporate

Reduction of SME tax rates for first RM150,000 from 17% to 15%

Income tax rate to be reduced from 17% to 15% for the first RM150,000 of chargeable income from YA 2023 for resident companies with paid- up capital of RM2.5 million and below and annual sales turnover not exceeding RM50 million.

Chargeable income of RM150,001 to RM600,000 remains to be taxed at 17%; excess shall be taxed at the prevailing rate of 24%.

Tax deduction for non-commercial Electric Vehicles (EV)

Tax deduction for company that rents non- commercial EV increase to RM300,000 for YA 2023 to YA 2025.

Tax deduction on smart artificial intelligence (AI) driven reverse vending machine

Special tax deduction for donations or sponsorships of Smart AI-Driven Reverse Vending Machine.

For contribution/sponsorship and applications received by Ministry of Finance (MOF) from 1 April 2023 until 31 December 2024.

Extension of full stamp duty exemption on the restructuring of loan/finance agreement executed from 1/1/23-31/12/24

Tax incentive for chicken rearing in closed house system

100% Accelerated capital allowance & Income Tax Exemption on qualifying capital expenditure incurred from YA 2023 until YA 2025.

Tax incentive for automation in manufacturing, service and agriculture sector

100% Accelerated capital allowance

• Scope of automation to include the adaptation of Industry 4.0 elements.

• Scope of tax incentive is expanded to include agriculture sector.

• Capital expenditure threshold to be increased up to RM10 million.

• Application extended to 31 December 2027

Extension of tax incentive on electrical and electronic

Extension of existing relocation incentives for the manufacturing sector.

Extension of tax incentive on biotechnology and food production

Existing tax exemption for BioNexus status companies is increased from 70% to 100% of statutory income and is extended to 31 December 2024.

Existing tax incentive for food production projects is extended to 31 December 2025 and expanded to include agricultural projects based on Controlled Environment Agriculture.

Extension of tax incentive on aerospace and shipbuilding

Existing income tax exemption and investment tax allowance for the aerospace industry is extended to 31 December 2025.

Existing tax incentives for the shipbuilding and ship repairing industry are extended to 31 December 2027.

Tax incentive for manufacturing of electric vehicle (EV) charging equipment

100% Income tax exemption on statutory income commencing YA 2023 to YA 2032 or 100% Investment tax allowance for a period of 5 years to set off against 100% of statutory income.

For applications received by Malaysian Investment Development Authority (MIDA) from 25 February 2023 until 31 December 2025.

Tax incentive for Carbon Capture and Storage (CCS)

Companies undertaking CCS in-house activity

• Investment tax allowance of 100% for 10 years to set-off against 100% of statutory income.

• Full import duty and sales tax exemption on equipment for CCS technology from 1 January 2023 until 31 December 2027.

• Tax deduction for allowable pre-commencement expenses within 5 years prior to the date of commencement of operation.

Companies undertaking CCS services

100% Investment tax allowance for 10 years to set-off against 100% statutory income or 70% Income tax exemption on statutory income for 10 years

• Full import duty and sales tax exemption on equipment used for CCS technology from 1 January 2023 until 31 December 2027.

• Tax deduction on fees incurred for use of CCS services for YA 2023 to YA 2027.

For applications received by MOF from 25 February 2023 until 31 December 2027.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o