Blog

Sales Tax (Exemption from Registration) (Amendment) Order 2022

Sales Tax (Exemption from Registration) (Amendment) Order 2022

The Royal Malaysian Customs Department has issued the Sales Tax (Exemption From Registration) (Amendment) Order 2022 on 1st September 2022 to replace the 2018 Order.

Don’t worry, let us summarize it for you.

Amendment # 1: Definition on Paragraph 2

2018 Order

-

Whose only have one of the manufacturing operations listed in Schedule A are exempted from registration.

2022 Order

-

Whose only have one of the manufacturing operations out of several operations in a manufacturing chain to produce a good and that operation is specified in Schedule A is exempt from registration.; and

-

The person who operates more than one manufacturing operation in Schedule A and manufacturing operations that do not relate in producing a goods is exempt from registration.

Amendment # 2: Schedule A

Removed Order

-

The incorporation of goods into buildings.

-

The installation of air conditioners in motor vehicles.

-

The manufacture of jewellery and goldsmiths wares.

-

The extraction of gold from mineral ores.

-

The recovery of gold from jewellery and / or the refining of gold.

New Order

-

A cleaning operation by removing dirt or dust without any further operation.

Amendment Order

-

The developing, printing of photograph, production of film slides or any forms or combination of any of those activities.

-

Engraving, printing, drawing, writing, embossing or any other similar activities on taxable goods with a description relating to the sports record or other circumstances under which the taxable goods was donated or awarded.

-

The preparation of foods or drinks by —

(i) any person who provide services under Group B, First Schedule, Service Tax Regulations 2018 or

(ii) central kitchen for distribution to its premises which provide services under Group B, First Schedule, Service Tax Regulations 2018

-

Printing, sewing or pasting of logo, knitting, crocheting or embroidering on ready made garments.

Sources:

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Cases on promoters under the Company Act

Cases on promoters under the Company Act

Who is a promoter?

“Someone who undertakes all necessary steps to form a company” - Twycross v Grant

What are Promoter duties?

-

Make an adequate disclosure

-

Does not exercise undue influence

-

Cannot make a secret

How to make an adequate disclosure?

Full disclosure of any transactions he had entered into on behalf of the company by way of

-

General meeting (Public Limited “Bhd”)

-

Board meeting (Private limited “Sdn Bhd”)

What does it mean by undue influence?

Where the “consent” is obtained by some pressure whereby the other party was in a disadvantaged position

Am I ever making a secret profit?

Profit in terms of rebates, discounts or incentives received without the company’s consent either by way of in the connection of the company or via its nominee (family related).

What if I breach my duties as a promoter?

Company may:

-

Rescind the contract

Case law : Erlanger v Sombrero Phosphate Co

-

Recovery of secret profit

Case law : Gluckstein v Barnes

-

Claim damages for breach of fiduciary duties

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

RMCD Special Voluntary Disclosure & Amnesty Program (VA) - Update

RMCD Special Voluntary Disclosure & Amnesty Program (VA) - Update

Background of VA

Under the proposed indirect tax amnesty program, taxpayers will be encouraged to voluntarily disclose underpaid or unpaid indirect taxes arising from errors or mistakes made in indirect tax filings or submissions, in exchange for reduced penalties.

Taxpayers who have failed to register and comply with indirect tax filing requirements are also expected to be eligible for the VA.

Key summary of VA

Special Voluntary Disclosure and Amnesty Program (VA) will be implemented with effect from 1 January 2022.

The VA program will be introduced in two (2) phases with penalty remission (with full payment during the said period) :

-

1 January 2022 to 30 June 2022 : 100% penalty remission

-

1 July 2022 to 31 December 2022 : 50% penalty remission

What is VA?

The VA program will involve two (2) distinct programs :

1. Voluntary disclosure program : Taxpayers can voluntarily disclose any unpaid or under-reported indirect tax/duty not known or discovered by RMCD under this program.

2. Amnesty program – Taxpayers with any outstanding Bill of Demand (“BOD”) or who have been audited by the RMCD Compliance Division and received audit findings on non-compliance areas can enjoy penalty and tax/duty remissions under this program.

The VA program will cover all indirect taxes administered by RMCD, including Sales Tax, Service Tax, GST, Tourism Tax, Departure Levy, Import Duty, Export Duty and Excise Duty.

Good faith

Voluntary disclosure submitted in good faith will be accepted. No audit will be conducted on the activities and periods involved.

Once the VA period is over, RMDC will enhance enforcement with hefty penalties.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Corporate and Business Information Data (CBID)

Corporate and Business Information Data (CBID)

Corporate and Business Information Data (CBID) is a business information tool available in SSM to customise data for both companies and businesses at a reasonable price.

The specific sets of data are divided into 3 segments as follows:

1. Demographic:- ie. gender, age, race, etc.;

2. Geographic:- ie. State, town, etc.; and

3. Financial:- ie. profit and loss, balance sheet, etc.

CBID become one of the important resources where users can obtain the information as research material to advantageously make a business decision in starting, operating, or even expanding the business.

The importance of CBID:

- business growth information in a particular location.

- marketing purpose and networking collaboration.

- specialised research and analysis.

- business or company expansion analysis either through joint ventures or alliances.

This product is accessible at e-CBID and the cost is listed below:

a) Companies

i) Processing Data / Statistics Fee - RM20/Application

ii) Companies Data Fee by Package - RM3/package per company

iii) List of Company – RM10/Company

iv) Companies Statistics Fee - RM100/statistic

b) Business

i) Processing Data / Statistics – RM10/Application

ii) Businesses Data Fee - RM10/Business

iii) Businesses Statistics Fee – RM20/Statistic

In conclusion, SSM encourages entrepreneurs to utilise the CBID platform for more accurate and reliable information to ease decision-making in business operations at an affordable price.

For more information, click here :

https://bit.ly/3AQ5QeO

https://bit.ly/3KVOdi8

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Exposure Draft on Section 23 Revenue of the IFRS for SMEs

Exposure Draft on Section 23 Revenue of the IFRS for SMEs

Section 23 of the IFRS for SMEs Accounting Standard set out requirement for SMEs to recognise revenue. It is based on IAS11 Construction Contracts and IAS 18 Revenue.

The IASB has applied the alignment approach to IFRS 15 Revenue from Contracts with Customers and is proposing to revise Section 23 by introducing a single framework for recognising revenue for goods and services.

The IASB is proposing to

-

introduce a framework for recognizing revenue which require revenue to be recognized when the customer obtains control of the goods/service, based on the 5 step model in IFRS 15.

-

simplify requirements of IFRS 15 to make the five-step model easier for SME

-

provide transition relief to allow SME to apply their current revenue recognition policy to contracts already in progress.

Framework for recognizing revenue

1. Identify the contract with a customer

2. Identify the promises in the contract

3. Determine the transaction price

4. Allocate the transaction price to the promises in the contract

5. Recognise revenue when (or as) the entity satisfy a promise

What would this proposal mean for SME?

A comprehensive framework for determining when and how much revenue to recognise for goods and services.

For many contracts, the revised Section23 is expected to have little, if any, effect on the amount and timing of revenue recognition.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Covid test tax deduction (update)

Covid test tax deduction (update)

Current requirements (remained)

An employer who claims the deduction of the Cost of Detection Test of COVID-19 shall produce: -

A receipt and certification of its employees issued by: -

-

a registered medical practitioner; or

-

a medical practitioner registered outside Malaysia; or

Addition requirements (updated)

A receipt and result of the detection test of Covid-19 of its employees issued by a health facility listed by the Ministry of Health Malaysia for the costs of the RT-PCR detection test incurred by its employee.

Where to check the registered medical practitioner?

Visit the official website of Malaysian Medical Council https://meritsmmc.moh.gov.my/search

What can I claim on tax 2023 Malaysia?

What can I claim on tax 2023 Malaysia?

Overview

Year 2022 is approaching to its end and now is the time for you to keep and plan on your personal tax.

Do you know what personal deduction can be claimed for year 2022?

With that, here’s the full list of tax reliefs for YA 2022.

Key takeaways:

You will know the Tax Relief and consequences for non-compliance as follows:

1. What types of Personal Tax Relief for YA 2022?

2. What types of donation allowed for deduction?

3. What types of documents are required to be kept?

4. How many years to keep the documents?

5. What are the consequences of non-keeping proper records?

Summary of learning

1. What types of Personal Tax Relief for YA 2022?

- Please refer to the link https://bit.ly/3R1Y6fU to get the full listing.

2. What types of donation allowed for deduction?

-

Gift of money to the Government/ approved institutions;

-

Contribution in fighting against the COVID-19 pandemic; or

-

Gift of money / cost / value of gift of medical equipment to any healthcare facility approved by the Ministry of Health or etc

-

For full information on tax allowable donation for deduction, please refer to the link https://bit.ly/3R1Y6fU.

3. What types of documents are required to be kept?

Receipts and supporting documents for the tax deduction claimed must be kept for future reference and inspection if required from LHDNM.

4. How many years to keep documents?

Must be kept for a period of seven (7) years after the end of the year in which the return form is furnished to LHDNM.

5. What are the consequences of non-keeping proper records?

A RM300.00 – RM10,000.00 fine or imprisonment for a term not exceeding twelve months of both.

Source

a) Public Ruling No. 5/2021 – Taxation of A Resident Individual Part I - Gifts Or Contributions And Allowable Deductions

https://phl.hasil.gov.my/pdf/pdfam/PR_05_2021.pdf

b) Public Ruling No. 5/2000 – Keeping Sufficient Records for Individuals & Partnerships

https://phl.hasil.gov.my/pdf/pdfam/PR5_2000_Rev.pdf

c) Public Ruling No. 6/2000 – Keeping Sufficient Records for Persons Other Than Companies Or Individuals

https://phl.hasil.gov.my/pdf/pdfam/PR6_2000_Rev.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

RiSE4WRD FOR INDUSTRY4WRD

RiSE4WRD FOR INDUSTRY4WRD

RiSE4WRD for Industry4WRD is HRD Corp's initiative to support the national agenda of embracing the Fourth Industrial Revolution (IR 4.0).

HRD Corp through RiSE4WRD aimed to support Industry4WRD policy by providing a platform for SMEs (Small & Medium Enterprises) in manufacturing sector which have undertaken the Readiness Assessment (RA).

HRDF Funding

Every SME is fully funded for the skills or training identified and recommended in the RA report.

The maximum funding is up to RM25,000 per SME.

Objectives of RiSEWRD

1. To create a platform for SMEs which participated in RA and identify suitable skillset/training programs.

2. To help the SMEs in funding the identified skills/training programs.

3. To ensure people readiness of the SMEs prior to high technology adoption or transformation.

Funding for training courses in the following areas:

Connectivity, automation, cyber security, Internet of Things (IoT), cloud computing, big data, advanced simulation, autonomous systems, universal integration, augmented reality and additive manufacturing or any relevant technology

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

SOCSO Enforce New Salary Ceiling Limit for Contributions

SOCSO Enforce New Salary Ceiling Limit for Contributions

Are you Aware of the Latest Announcement by SOCSO on New Salary Ceiling Limit?

Effective from 1st September 2022, SOCSO will increase the monthly salary ceiling limit from RM4,000 to RM5,000 for contributions.

i. How would this affect the SOCSO and EIS contributions?

• Additional SOCSO and EIS contributions for employees who earn monthly salaries between RM4,000 and RM5,000.

• Flat contribution rates for both SOCSO and EIS for employees who earn RM5,000 or more per month.

For the latest contribution rate, please refer to the link below

https://www.perkeso.gov.my/en/rate-of-contribution.html

ii. What Should the Employers Do?

• Employers must make contribution payments in accordance with the new wage ceiling limit adjustment.

• Employers are requested to record the contribution deductions in the pay slip or statements of their respective employees.

iii. Transition Period for Employers

The transition period for employers to comply with the new contribution rate is six (6) months, starting from 1st September 2022 to 28th February 2023.

Source:

Employment Insurance System (Amendment) Act 2022:

- https://lom.agc.gov.my/act-detail.php?type=amendment&act=A1657&lang=BI

- Employees’ Social Security (Amendment) Act 2022:

- https://lom.agc.gov.my/act-detail.php?type=amendment&act=A1658&lang=BI

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Tax Incentive for Organising Conferences in Malaysia

Tax Incentive for Organising Conferences in Malaysia

Overview

On 29 July 2022, IRB issued Public Ruling (PR) No.2/2022 - Tax incentive for organising conferences in Malaysia. Generally, this PR has explained the tax incentive are available to:

1. Conference promoter promoting and organising conferences in Malaysia as its main activity; and

2. Qualifying person whose main activities are other than promoting and organising conferences in Malaysia. In simple words, the nature of business is not related to promoting and organising conferences. For instance, a manufacturing company.

Key takeaways:

You will understand: -

1. What is the tax incentive?

2. How to become an eligible conference promoter and qualifying person?

3. Differences between conference promoter and qualifying person?

4. Requirement of separate account?

Summary of learnings:

1. What is the tax incentive?

The tax incentive is given to eligible conference promoter and qualifying person.

The exemption is on 100% of the statutory income derived from organising conferences held in Malaysia in the relevant year of assessment.

2. How to become an eligible conferences promoter and qualifying person?

Brought in at least 500 foreign participants to attend conferences held in Malaysia in the year assessment.

3. Differences between conferences promoter and qualifying person

i) Under Income Tax (Exemption) (No.53) Order 2000 [P.U. (A) 500/2000], an eligible conference promoter must be a resident company, an association, or an organisation whose main activities are promoting and organizing conferences in Malaysia.

The period of exemption is effective from the year of assessment 1997 onwards.

ii) Whereas under Income Tax (Exemption) (No.4) Order 2021 [P.U. (A) 195/2021], a qualifying person which is a resident company, an association, or an organisation that carries on business not related to the activity of promoting and organizing conference is also eligible to enjoy the tax incentive.

The period of exemption is effective from the year of assessment 2020 until 2025.

4. Separate accounts

A separate account is required to be maintained for the income exempt under both P.U.(A) 500/2000 or P.U.(A) 195/2021.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Tax on digital currency Malaysia

Tax on cryptocurrency Malaysia Part 2

IRB has issued the Guideline on Tax Treatment of Digital Currency Transactions dated 26 August 2022.

Key issues in the guideline include :

Taxability

Crypto transactions fall under the scope of Malaysia income tax if

-

the key activities and operation business operations are performed in Malaysia or

-

where there is a business presence in Malaysia

Summary of Tax on Digital Currency

-

Trading of digital currencies - Profit from the business of trading is taxable .

-

Mining of digital currencies- Profits from the mining of digital currencies are subject to income tax if the mining activity is carried out with a profit-seeking motive.

-

Business transactions carried out using digital currency- Record based on the open market value of the underlying goods or services in RM.

-

Realisation of digital currencies from business transaction- The tax treatment of the subsequent disposal of the digital currency received will depend on the analysis of the capital and revenue (ie badge of trade)

-

Realisation of digital currencies investment-The tax treatment will depend on the analysis of the capital and revenue (ie badge of trade).

-

Free distribution - The mere purchase of digital currencies as a result of free distribution/spitting is not taxable.

-

Exchange of digital currencies -The tax treatment will depend on the analysis of the capital and revenue (ie badge of trade)

Past Blog on tax on cryptocurrency Malaysia

https://www.ktp.com.my/blog/tax-on-cryptocurrency-malaysia/05sept2022

This message was brought to you by KTP

What is Automation Capital Allowance (ACA) ?

What is Automation Capital Allowance (ACA) ?

Overview of ACA :

After the opening of international borders, Malaysia is facing a serious manpower situation, thus, Automation machines may become one of the solutions for manufacturing companies to overcome the workforce issue.

The Automation Capital Allowance (Automation CA) was introduced to encourage the adoption of automation among manufacturing companies. In budget 2020, the Government extended the period for the incentive in both categories. The effective date of application is from 1 Jan 2015 until 31 Dec 2023.

Key takeaways:

1. How does the incentive work?

2. Who is eligible to claim?

3. Application procedures

4. Thing to take note

Summary of learnings:

1. What type of incentive?

A. Labour-intensive industries (rubber products, plastics, wood, furniture, and textiles)

- Automation Capital Allowance of 200% on the first RM4 million expenditure incurred within assessment from 2015 to 2023

B. Other Industries

- Automation Capital Allowance of 200% on the first RM2 million expenditure incurred within assessment from 2015 to 2023

2. Who is eligible to claim?

I. Manufacturing companies incorporated under the Companies Act, 1965 / 2016

II. Resident in Malaysia

III. Valid Business License and Manufacturing License

IV. The Company has been in operation as manufacturing activities for 36 months

V. Automation machine/equipment is used directly in the manufacturing activities

3. Application process:

I. Submit the ‘Automation CA Form’ to MIDA

II. MIDA evaluation and SIRIM site visits regarding technical verifications

III. MIDA issues a ‘Consideration Letter’ as approval

4. Things to take note:

A. The incentive is mutually exclusive to other incentives; thus, Company can only enjoy one of the incentives including Automation CA, Reinvestment Allowance (RA), Pioneer Status (PS), Investment Tax Allowance (ITA), or Allowance for Increased Exports (AIE)

B. If Company is claiming RA, it also can opt to claim Automation CA. However, the company must utilize the full amount of Automation CA before it continues to claim RA and the period of RA will continue even if the Company has opted for Automation CA.

Sources:

- Guidelines and Procedures for the application of Automation Capital Allowance

https://www.mida.gov.my/wp-content/uploads/2021/01/GD_ACA_14012021.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

MPERS Section 33 Related party disclosures

MPERS Section 33 Related party disclosures

My auditor is so annoying! Every time audit needs to ask me to confirm related party balances and transactions and force me to disclose them in my financial report.

Why?

Malaysian Private Entity Reporting Standard (MPERS) Section 33 has clearly stated that the Company should disclose anything that involves related parties which have affected the Company’s financial position and its profit and loss in its financial statement.

Who are the Related Party?

1. Parent and subsidiary relationship

2. Subsidiaries of Common parent company

3. Associates

4. Joint ventures Entities

5. Key management personnel with significant influence

6. A close family to the key management personnel

100% related party if two entities have a common director?

1. Assessment of the extent of the relationships is required (MEPRS 33.3) to determine whether the director has significant influence in both entities (MPERS 33.2) instead of judging on its legal title.

2. Hence, the two companies are not necessarily related parties even though they have common directors.

What disclosures are required for related parties at the reporting entity’s year ended?

1. Nature of related party relationship

2. Type of transactions

3. Value of transactions

4. Outstanding balance between related parties and its terms and conditions

What are the examples of the transactions?

1. Sales and purchase of goods

2. Rendering or receiving any form of services

3. Acquisition and disposal of assets

4. Use of assets by way of lease arrangement

5. Borrowings, lending, and guarantees provided for/to

6. Others

Source:

MPERS Section 33 Related party disclosures:

- https://c0aa0d68-de31-44c8-bb40 ac5f2e0a9fe4.filesusr.com/ugd/a87018_5b13be37ec354e388901ef7342d8f641.pdf?index=true

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Tax Incentives in Agriculture Industry

Tax Incentives in Agriculture Industry

Under the Promotion of Investments Act 1986, the term ''company” in relation to agriculture includes:

-

agro-based cooperative societies and associations

-

sole proprietorships and partnerships engaged in agriculture.

Companies producing promoted products or engaged in promoted activities are eligible to apply for the following incentives:

Pioneer Status

As in the manufacturing sector, companies producing promoted products or engaged in promoted activities are eligible for Pioneer Status.

Investment Tax Allowance (ITA)

Companies producing promoted products or engaged in promoted activities can apply for Investment Tax Allowance (ITA). To enable agricultural projects to enjoy greater benefits, the Government has broadened the definition of qualifying capital expenditure to include the following:

-

the clearing and preparation of land;

-

the planting of crops;

-

the provision of plant and machinery used in Malaysia for the purposes of crop cultivation, animal farming, aquaculture, inland or deep-sea fishing and other agricultural or pastoral pursuits;

-

the construction of access roads including bridges, the construction or purchase of buildings (including those provided for the welfare of persons or as living accommodation for persons) and structural improvements on land or other structures which are used for the purposes of crop cultivation, animal farming, aquaculture, inland fishing and other agricultural or pastoral pursuits. Such roads, bridges, buildings, structural improvements on land and other structures should be on land forming part of the land used for the purpose of such crop cultivation, animal farming, aquaculture, inland fishing and other agricultural or pastoral pursuits.

In view of the time lag between start-up of the agricultural project and processing of the produce, integrated agricultural projects are eligible for ITA for an additional five years for expenditure incurred for processing or manufacturing operations.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

This message was brought to you by KTP

Tax on cryptocurrency Malaysia

Tax on cryptocurrency Malaysia

Badge of trade

Determining the existence of trade The general tax treatment for transaction gain / loss from the disposal of digital currencies is based on whether it is capital or revenue in nature.

The badges of trade such as profit seeking motive, nature of asset and changes to the asset are considered when determining if such gains are taxable. The followings are considerations in deciding whether elements of trade exist for transactions involving digital currencies:

1. Nature of subject matter

This refers to the nature of the digital currencies that is being bought and sold. The digital currencies could be regarded as the subject of trading when they are bought in large quantities.

2. Length of ownership

This refers to the holding period of the digital currencies. The shorter the holding period, the more likely it would be regarded as held for trading.

3. Frequency of transactions

High frequency of similar transactions of digital currencies is more indicative of trading than an isolated transaction.

4. Supplementary work

This refers to additional work done on digital currencies to make it more marketable or extra effort made to find or attract purchasers. If this is done, it is more likely that the subsequent disposal would be regarded as trading.

5. Circumstances of the realization

Some circumstances are less likely to indicate trading (e.g. company is forced to sell the digital currencies due to compulsory acquisition, sudden urgent need of cash or threat of foreclosure by creditors).

6. Motive

This refers to whether there was an intention to trade at the time of the acquisition of the digital currencies. If a person undertake the activities in a business-lime manners such as developing a business plan, preparing accounting records and advertising the digital currencies business, the intention is definitely to do a business of digital currencies.

7. Mode of financing

This refers to how the purchase of the digital currencies is being financed. Short term financing is more indicative of trading than long term financing. The company’s financial position and ability to hold on to the digital currencies will also be taken into consideration.

Source

IRB Guideline on tax treatment on digital currency transactions @ 26/8/2022

This message was brought to you by KTP

Agriculture Allowance

Agriculture Allowance

Are agriculture companies entitled to any tax incentives?

Agriculture allowance

A taxpayer who incurred Qualifying Agriculture Expenditure is entitled to claim Agriculture Allowance.

Qualifying Agriculture Expenditure

1. Clearing and preparation of land

2. New planting (exclude replanting) either:

a) new crop of any product

b) replace old crops with a crop of a different type

3. Construction on a farm of a road or bridge

4. Construction on a farm of a building either:

a) used in working of farm

b) welfare of persons

c) living accommodation

5. Schedule of Agriculture Allowance

Non-Qualifying Agriculture Expenditure

1. Cost of land

2. Cost of plant and machinery used in the farm

Agriculture Charges (Disposal)

1. If disposal within 5 years: agriculture charge equal = allowances claimed in prior years

2. If disposal made after 5 years: no agriculture charge will be made

Source

Reference: Public Ruling No. 1/2016 Agriculture Allowance

https://phl.hasil.gov.my/pdf/pdfam/PR_01_2016.pdf

This message was brought to you by KTP

Tax Deduction on Payment to Release Bumi Lot

Tax Deduction on Payment to Release Bumi Lot

Do you know there are 6 deciding case law in high court from 2020 to 2021 on the tax appeal regarding payment to release bumi lot.

Today we cover one recent Court of Appeal case namely DIRECTOR GENERAL OF INLAND REVENUE vs TAMAN EQUINE (M) SDN BHD which overturn High Court decision.

Lesson from Tax Case:

The tax treatment of application expenses incurred to release the Bumiputera quota units by a housing developer.

Background information

Taman Equine (M) Sdn Bhd (The Company) is a housing developer.

The Company has incurred expenses to apply to State Government to release the Bumiputera quota units.

Tax Issue:

Are expenses incurred for the release of the Bumiputera quote units allowable for tax deduction?

The Company’s opinion:

The application of the release the Bumiputera quota units is necessary else the Company would not be able to generate its income. Thus, the expenses incurred for the business expenses under section 33(1) ITA 1967.

IRB argument:

The expenditures in question were not eligible for deduction under Section 33(1) of the ITA for the following reasons:

a) the cost incurred is a penalty in nature and

b) not wholly and exclusively incurred for the purpose of producing the gross income.

The decision by The Court of Appeal

The Company expenses were not allowed for deduction due to the following reason:

a) the nature of the payment is a penalty for breach of a condition imposed by the State Government.

b) it does not form part of the taxpayer’s income-producing activity.

c) the expenses incurred are for the purpose of bringing into existence an advantage in terms of procuring permission/consent from the state authority for the permanent benefit of the business

d) it is capital in nature and prohibited under section 39(1) ITA 1967.

Source:

https://phl.hasil.gov.my/pdf/pdfam/KPHDN_v_TAMAN_EQUINE_17062022.pdf

This message was brought to you by KTP

Key Amendments to the Employment Act 1955 (Gazetted 2022)

Key Amendments to the Employment Act 1955

Definition of employment

1. Employee earning RM4000 and below *

2. Employee in manual labour

3. Supervisor of employee in manual labour

4. Employee in mechanically propelled vehicle

5. Domestic employee

*Provision of the Act not applicable include overtime, payment for work done on off/rest day and public holidays, shift allowance and termination benefits for employee’s wages exceeds RM4000.

Presumption of employment

The Bill provides that in the absence of a written contract and unless proven otherwise, there will be presumption of an employment relationship if the following factors are given:

-

his/her work or hours of work are subject to control by another person;

-

he/she is equipped with tools, material or equipment by another person to execute his work;

-

his/her work constitutes an integral part of another person's business;

-

his/her work is performed solely for the benefit of another person; or

-

payment is made to him/her for work done at regular intervals and it constitutes the majority of his/her income.

Apprenticeship Contract

Shall be for a minimum period of six months and a maximum period of twenty four months.

Calculation of wages for an incomplete month

The Bill provides a new section in the Act that introduces the below formula for calculating wages where an employee has not worked a full month:

(Monthly wages/number of days of the particular wage period ) X Number of days eligible in the wages period

For OT (or encashment of annual leave) : ordinary rate of pay (ie 26 days) remain unchanged under the current law.

Extension of maternity leave

Previously, the Act provided a 60 days maternity leave for all female employees, subject to the conditions of the Act. Now, when the Bill comes into force, eligible female employees will be entitled to 98 days of maternity leave.

Restriction on termination of pregnant employees

The Bill introduces a new section in the EA which prohibits an employer from terminating an employee who is pregnant or is suffering from an illness arising out of her pregnancy, except under specific circumstances such as willful breach of contract, misconduct or closure of the employer’s business. It is vital on employers to prove that the termination was not due to pregnancy.

Paternity Leave

Married male employees will now be entitled to 7 consecutive days of paternity leave up to 5 confinements.

Sexual harassment

The Bill introduces a new section which requires employers to conspicuously exhibit a notice to raise awareness of sexual harassment in the workplace. The sexual harassment provisions are still viewed as weak and limited. The Anti Sexual Harassment Bill 2021 would provide more guidelines upon being passed. It is currently in its first reading in Parliament.

Employment of foreign employees

Approval must be obtained from the Director-General of Labor to employ a foreign employee. Upon the employer satisfying the conditions listed in the Act, approvals are granted. Failure to obtain an approval is an offense, and on conviction, the employer shall be liable to a fine not exceeding RM 100,000 and/or to imprisonment for a term not exceeding five years.

Reduction on working hours

Previously, the Act provided 48 hours as regular working hours. With the Bill coming into force, the regular working hours will be reduced to 45 hours a week.

Flexible working arrangements

Employees can apply for flexible working arrangement, depending on the suitability of the working hours or work place. However, there is no legal obligation on the employer to grant this request. If the employer is to reject the request, they are required to provide grounds of refusal within 60 days of the application.

Discrimination

The Director General has the authority to investigate and decide disputes on discrimination in employment between employer and employee. Furthermore, the Director General has the power to make an order where necessary. However, this provision is vague and it does not define discrimination. Job seekers will not be able to rely on this provision as there is no employment relationship between an employer and job seekers, and as such this provision will not apply to protect job seekers from discrimination.

This message was brought to you by KTP

What is Attestation of Company Good Standing (ACGS)?

What is the meaning of good standing from SSM?

What is Attestation of Company Good Standing (ACGS)?

ACGS is a confirmation from SSM that a company has met the criteria that were set in the issuance of this ACGS.

The Content in ACGS

Ø Company Name

Ø Company Registration Number

Ø Incorporation Date

Ø Types of the Company (Public /Private)

Ø Registered Address

Criteria of ACGS Product for a Company

1. Incorporated for at least 18 months from the date of purchase ACFS;

2. Lodged its latest annual return and audited financial statements or certificate relating to an Exempt Private Company;

3. Existence and not in the process of being wound up or struck off or dissolved ;

4. Not dormant according to the nature of business;

5. Has a registered address;

6. The company or its directors do not consist of any outstanding compound; and

7. The company or its directors do not have any pending prosecution case.

Why is ACGS important?

a) Official

– Confirmation issued by SSM and able to verified by digital scan QR code

b) Compliance

– The company’s statutory form and return are filed, up to date and well maintain or organised

c) Trustworthy

– Meet the criteria set up by SSM with confirmation and certification

d) Reliable

– consistently good in quality or performance and able to be trusted

How to generate a company ACGS?

ACGS can be generated upon request by the user if it passes the set criteria.

Will be available in SSM e-info if the Company meets all the requirements.

Where to purchase and the cost?

The user can purchase ACGS from SSM e-Info website [https://www.ssm-einfo.my/]

RM105 for each purchase.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

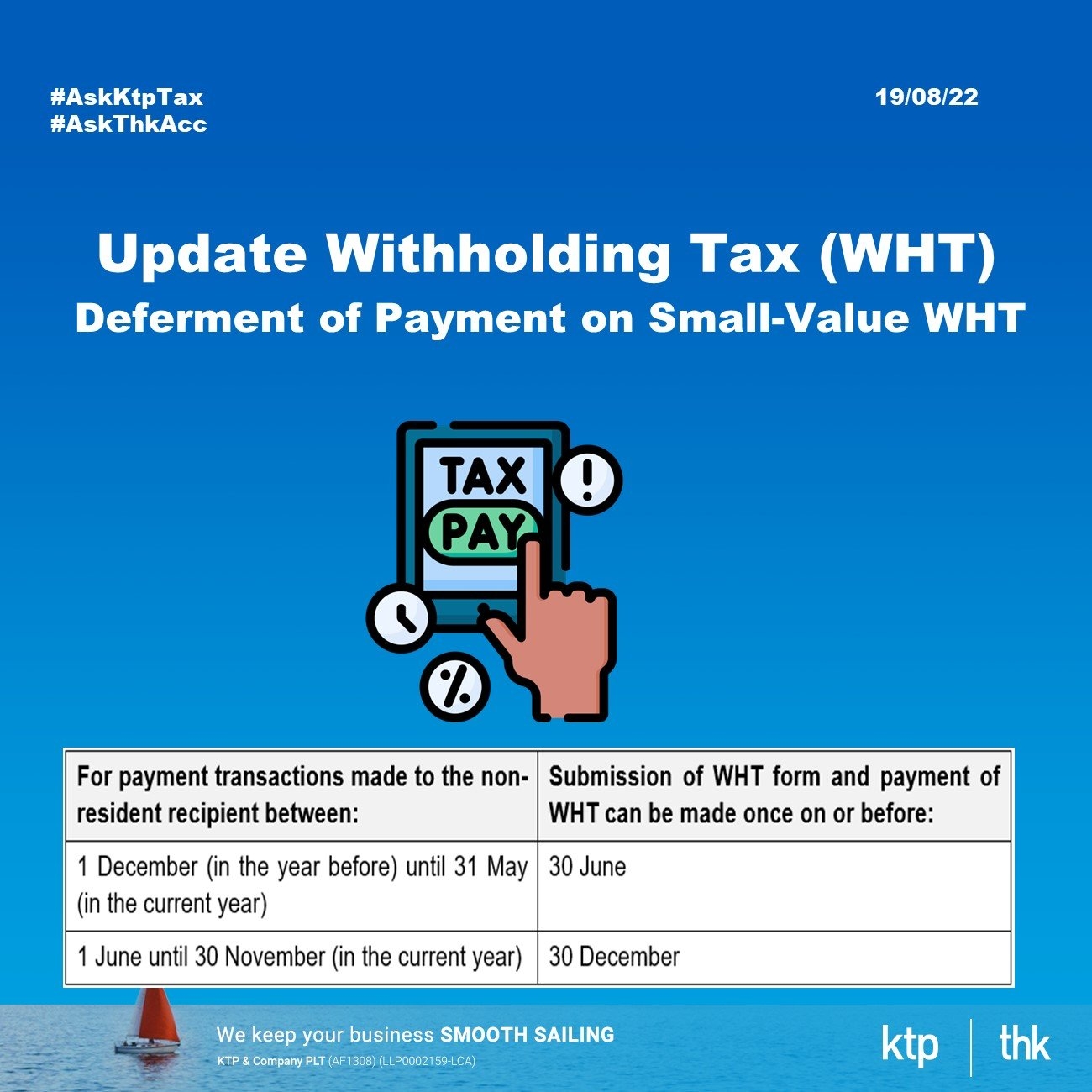

Small Value Withholding Tax Payment

Small Value Withholding Tax Payment

An individual/body resident in Malaysia or doing business in Malaysia that is required to pay WHT under S.109 or S.109B of the Income Tax Act 1967 that do not exceed RM500 per transaction for transactions that recur may submit the WHT form and pay the WHT as follows:

(See above)

-

S.109 = Royalty and Interest earned by non-resident

-

S.109B = Special class of income under Section 4A of the ITA including service and rental of moveable property

Others Operational Issue

The above will take effect from August 2022.

IRBM is in the process of preparing the special WHT forms for the purposes of the above.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o