Blog

director duties company law

Can a director be sued in Malaysia?

Corporate Veil

When a company is incorporated, it is deemed to be a separate legal entity that is distinct and separate from its members such that a 'corporate veil' is said to be drawn to separate the company and its members or directors.

In other words, the company’s rights and liabilities are their own and not that of the individual business owner. This principle has long been established in the English case of Salomon v Salomon & Co Ltd and has been adopted within the Malaysian jurisdiction as well.

Duties of Director under Common Law

The directors are effectively the agents of the company, appointed by the shareholders to manage its day-to-day affairs.

As a director of the company, you own

-

Duty to act bona fide in the interest of the company.

-

Duty to use power for a proper purpose.

-

Duty not to fetter discretions.

-

Duty to avoid actual and potential conflict of interest.

-

Duty to ensure the integrity of financial information.

Remedy Action under Company Act 2016

Section 346 of the Companies Act 2016 provides the courts with wide powers to grant remedies as they deem necessary to bring an end to the matters complained of in an oppression action.

Any member of a company may apply to the Court for an order :

(a) The affairs of the company are being conducted or the power of the director are being exercise in oppressive manner.

(b) Some act of the company has been passed which unfairly discriminate.

RDS Bina Sdn Bhd v Ong Chin Hoe & Anor

The Plaintiff filed a claim against the directors of a company in order to enforce payment due under a settlement agreement entered with the company that subsequently ceased operations and dissolved. The Plaintiff presented evidence of fraudulent acts by the directors to deregister their company to evade paying the monies owed to the Plaintiff. The Court allowed the Plaintiff to lift the corporate veil and found the directors to be personally liable for the debts owing to the Plaintiff.

Keller (M) Sdn Bhd v Ong Leong Chiou & Ors

The Plaintiff roped in several parties including a director of a company for the amount due to them as the appointed sub-contractor for work done in the construction of a shopping mall project. Upon close examination of the relationship between the parties, it was discovered that the 1st Defendant (Director) had orchestrated a complex plan to hide under the corporate veil in order to escape liability.

The 1st Defendant used a company (2nd Defendant) under his control and command to shield another company (3rd Defendant) from liability for fraud engineered by him.

Shortly after the project was completed, the 1st Defendant and other directors from the 2nd Defendant resigned and transferred their shares to other parties. In furtherance of the fraud, the 1st Defendant had also actively concealed vital information from the Plaintiff. These actions allowed the Court to pierce the corporate veil and have the Defendants jointly liable to pay the Plaintiff.

Final Word

In conclusion, the law generally provides a safe haven for directors through the separation of entity principle.

However, directors should not abuse their position by taking advantage of it as the new Company Act 2016 provide remedy actions for shareholders.

Source :

Ask Legal https://bit.ly/3OUzpBR

Donovan & Ho https://bit.ly/3nPSSHX

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

unabsorbed business loss carried forward 10 years

How many years can unabsorbed business losses can be carried forward?

Public Ruling 1/2022 - Time limit on unabsorbed adjusted business losses carry forward

IRB has produced the first public ruling of 2022 !

The objective of this Public Ruling (PR) is to provide an explanation on the time limit for unutilised or unabsorbed adjusted business losses arising from a business of a person to be carried forward.

Background

Effective year of assessment 2019, unabsorbed adjusted business losses carried forward for a period of 7 consecutive years of assessment.

But…subsequently.

The time limit for unabsorbed adjusted business losses carried forward arising from a relevant year of assessment change from a 7 consecutive years of assessment to 10 consecutive years of assessment through the Finance Act 2021 [Act 833] effective year of assessment 2019.

Tax Implication

Any balance of unabsorbed adjusted business losses after the

end of the period of 10 consecutive years of assessment is to be disregarded (ie lost).

T & C on Dormant Companies Solely

There has been no substantial change in the company’s shareholding.

By shareholding, Compare the last day of last YA and the first day of next YA on shareholding.

-

More than 50% of the paid-up capital.

-

More than 50% of the nominal value of the allotted shares.

Sections 44(5A) to (5D) – shareholder continuity rules

In a nutshell, where the shareholding of a company was changed substantially during a basis period, any unabsorbed loss and capital allowance brought forward were disregarded – ie were effectively lost forever.

These provisions have been somewhat suspended or deferred as it has been confirmed by the tax authorities that these rules are only applicable in the case of a substantial change of shareholding in dormant companies.

This is further validated via

-

Form C guidebook page 8

-

Post budget technical

-

LHDN dasar dan garis panduan untuk menbenarkan kerugian terkumpul dan elaun modal yang tidak diserap dibawa ke hadapan

https://phl.hasil.gov.my/pdf/pdfam/GP_Membenarkan_kerugianterkumpul.pdf

Source

Public Ruling 1/2022 Time limit on unabsorbed adjusted business losses carry forward

https://phl.hasil.gov.my/pdf/pdfam/PR_01_2022.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

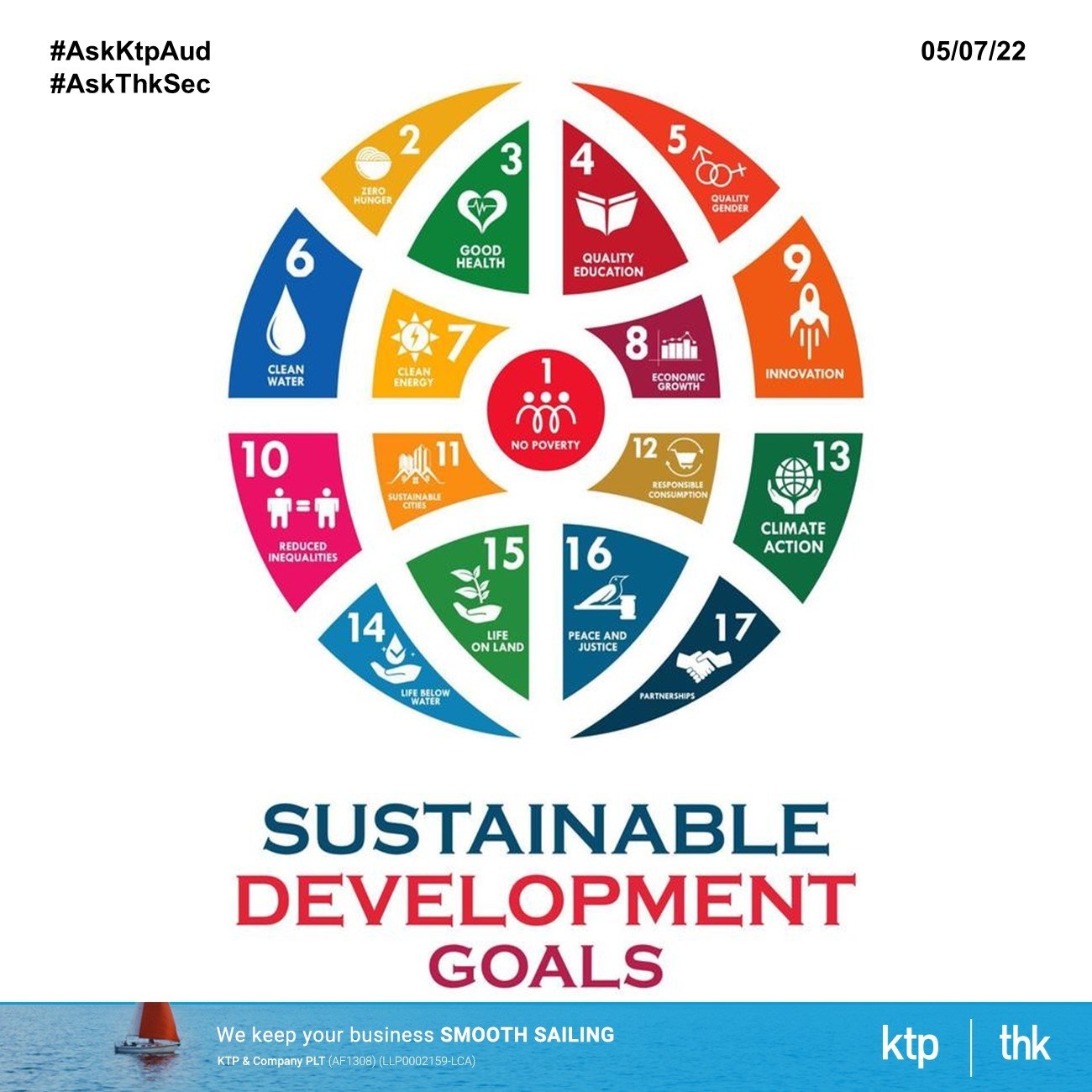

UN Sustainable Development Goals Part 2

UN SDG 17

The UN Sustainable Development Goals were launched in 2012 and finalised in 2015. They represent an international consensus on conditions under which humanity can thrive.

The UN SDGs set out a path to end extreme poverty, fight inequality and injustice, and protect the planet.

The United Nations 17 SDGs are a globally agreed framework for all countries to achieve by 2030 that sets out the building blocks of a new type of inclusive prosperity creation.

SDG 7 : Affordable and Clean Energy

Sustainable Development Goal 7 (SDG7) calls for “affordable, reliable, sustainable and modern energy for all” by 2030. It's three core targets are the foundation for our work: Ensure universal access to affordable, reliable and modern energy services.

SDG 8 : Decent Work and Economic Growth

SDG 8 recognises the importance of sustained economic growth and high levels of economic productivity for the creation of well-paid quality jobs, as well as resource efficiency in consumption and production.

SDG 9 : Industry Innovation and Infrastructure

Goal: Support domestic technology development, research and innovation in developing countries, including by ensuring a conducive policy environment for, inter alia, industrial diversification and value addition to commodities by 2030.

SDG 10 : Reduced Inequalities

Sustainable Development Goal 10 aims at reducing inequality within and among countries. This SDG calls for reducing inequalities in income as well as those based on age, sex, disability, race, ethnicity, origin, religion or economic or other status within a country.

SDG 11 : Sustain Cities and Communities

SDG 11 aims to renew and plan cities and other human settlements in a way that offers opportunities for all, with access to basic services, energy, housing, transportation and green public spaces, while reducing resource use and environmental impact.

SDG 12 : Responsible Consumption and Production

Sustainable Development Goal 12 encourages more sustainable consumption and production patterns through various measures, including specific policies and international agreements on the management of materials that are toxic to the environment.

SDG 13 : Climate Action

SDG 13 intends to take urgent action in order to combat climate change and its impacts. The contributing countries to this SDG are making plans to prioritize food security and production, terrestrial and wetland ecosystems, freshwater resources, human health, and key economic sectors and services.

SDG 14 : Life Below Water

SDG 14 targets seek to prevent and reduce marine pollution; further the sustainable management and protection of marine and coastal ecosystems; address the impacts of ocean acidification; regulate harvesting and end overfishing, illegal, unreported and unregulated fishing and destructive fishing practices.

SDG 15 : Life On Land

Goal 15 focuses specifically on managing forests sustainably, halting and reversing land and natural habitat degradation, successfully combating desertification and stopping biodiversity loss.

SDG 16 : Peace, Justice and Strong Institutions

Goal 16: Promote peaceful and inclusive societies for sustainable development, provide access to justice for all and build effective, accountable and inclusive institutions at all levels. Significantly reduce all forms of violence and related death rates everywhere.

SDG 17 : Partnership for the Goals

SDG 17 calls for a global partnership for sustainable development. The goal highlights the importance of global macroeconomic stability and the need to mobilise financial resources for developing countries from international sources, as well as through strengthened domestic capacities for revenue collection.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

UN Sustainable Development Goals Part 1

UN Sustainable Development Goals

Why is it important to talk about sustainability?

The fundamental fact underlying the whole topic is this: over the last century the population of the Earth increased from 1.5 to 7 billion people. Thus, building an inclusive, sustainable and resilient future for all people and our planet has become a big challenge for humanity.

What is sustainability?

It is defined as “Meeting the needs of the present without compromising the ability of future generations to meet their own needs.”

UN SDG 17

The UN SDGs set out a path to end extreme poverty, fight inequality and injustice, and protect the planet. Achieving the goals will require an unprecedented effort by all sectors in society, including businesses.

SDG 1 : No Poverty

SDG 1 is to: ''End poverty in all its forms everywhere''. Achieving SDG 1 would end extreme poverty globally by 2030. The goal has seven targets and 13 indicators to measure progress.

SDG 2 : Zero Hunger

Goal 2 seeks sustainable solutions to end hunger in all its forms by 2030 and to achieve food security. The aim is to ensure that everyone everywhere has enough good-quality food to lead a healthy life. Achieving this Goal will require better access to food and the widespread promotion of sustainable agriculture

SDG 3 : Good Health and Well Being

SDG 3 aims to prevent needless suffering from preventable diseases and premature death by focusing on key targets that boost the health of a country's overall population. Regions with the highest burden of disease and neglected population groups and regions are priority areas.

SDG 4 : Quality Education

Ensure inclusive and equitable quality education and promote lifelong learning opportunities for all.

SDG 5 : Gender Equation

Achieve gender equality and empower all women and girls. Gender equality is not only a fundamental human right, but a necessary foundation for a peaceful, prosperous and sustainable world.

SDG 6 : Clean Water & Sanitation

Ensure access to water and sanitation for all. While substantial progress has been made in increasing access to clean drinking water and sanitation, billions of people—mostly in rural areas—still lack these basic services.

To be continue

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

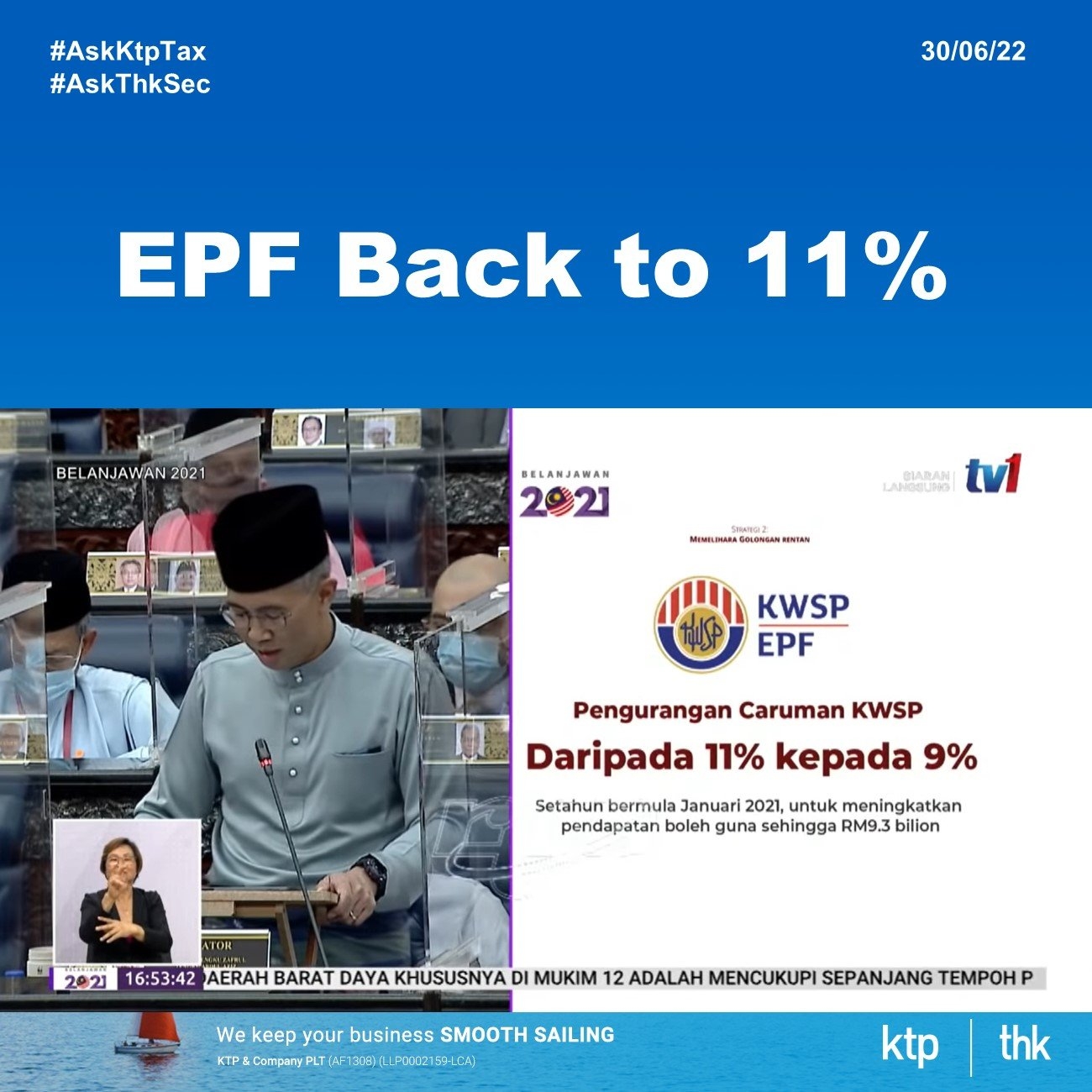

EPF return to 11%

EPF back to 11%

Background

With effective 1st January 2021 after the Budget 2021, employees have the option to reduce their EPF statutory contribution rate from 11% to 9%. This rate for employees will be in effect from January 2021 wages (February 2021 contribution) up to June 2022 (July 2022 Contribution) wages.

Why 9%

“The government understands the challenges faced by the people due to prolonged lockdowns and to increase cash in hand, EPF will extend the minimum contribution rate from 11% to 9% until June 2022.'' says Finance Minister Tengku Datuk Seri Zafrul Tengku Abdul Aziz.

Borang KWSP 17A for 11% contribution

The reduced rate is default for all employees under 60 years old.

Should an employee choose to remain at 11% contribution rate, they'll need to fill up Borang KWSP 17A (Khas 2022) which will then be submitted to EPF by their respective employer. For those aged 60 and above, the statutory contribution remains at the existing rate.

Upon receiving the completed Borang KWSP 17A (Khas 2022) form from the employees, employers will need to register the application via the i-Akaun (Employer) and keep the completed Borang KWSP 17A (Khas 2022) form as a record.

Back to EPF 11%

The minimum statutory EPF contribution rate for employees returns to 11% from July 2022 wages onwards (August 2022 contribution)

Source:

https://www.kwsp.gov.my/en/belanjawan-2021#Reduction-Statutory-Contribution-Rate

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Accounting for government grants

MPERS vs MFRS : Government Grants

In this article, we share the main differences in the accounting requirements for associates under MFRS 120 and Section 24 of MPERS.

Government Grants

Government grants are assistance by the government in the form of transfers of resources to an entity in return for past or future compliance with certain conditions relating to the operating activities of the entity.

They exclude those forms of government assistance which cannot reasonably have a value placed upon them and transactions with the government which cannot be distinguished from the normal trading transactions of the entity.

Section 24 of MPERS - Government Grants

Use income approach as all government grants are income transactions.

If there is no specified future performance condition imposed, the grant is recognized upon receivable.

If there is a specified future performance condition imposed, the grant is recognized when the condition is met.

Government grants are measured at the fair value of the assets received or receivable.

MFRS 120 Government Grants

Use income approach as all government grants.

Conditions :

1. The entity will comply with the conditions imposed.

2. The grants will be received.

Recognise grants in P/L on a systematic basis over periods in which the entity recognise the related costs.

Non-monetary grants is measured by

-

The fair value of assets received.

-

Nominal amount paid

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Accounting for intangible assets

MPERS vs MFRS : Intangible Assets

In this article, we share the main differences in the accounting requirements for associates under MFRS 138 and Section 18 of MPERS.

Intangible Assets

An item meets the definition of intangible asset if it poses the three criteria:

-

Identifiability.

-

Control over resources.

-

Existence of future economic benefits (or service potential).

An intangible asset is an identifiable non-monetary asset without physical substance. Such an asset is identifiable when it is separable, or when it arises from contractual or other legal rights. Separable assets can be sold, transferred, licensed, etc.

Examples of intangible assets include computer software, licences, trademarks, patents, films, copyrights and import quotas.

Section 18 of MPERS - Intangible Assets

Research and development expenditures should be recognized as expenses.

All internally generated intellectual property should be recognized as an expense.

MFRS 138 - Intangible Assets

Development expenditure of R&D activities that meet the recognition criteria must be capitalize.

All research and other development expenditure are recognized as an expense.

Internally generated intellectual property should not be recognized as an asset.

An entity is to recognise an intangible asset only if the two criteria are met:

1. It is probable that the expected future economic benefits (or service potential) will flow to the entity; and

2. It can measure the cost or fair value of the asset reliably.

MFRS 138 allow an entity to capitalise expenditure from the development phase if it can demonstrate all of the following conditions:

-

The technical feasibility of completing the intangible asset so that it will be available for use or sale.

-

Its intention to complete the asset and use or sell it.

-

Its ability to use or sell the intangible asset.

-

How the intangible asset will generate probable future economic benefits or service potential.

-

The availability of adequate technical, financial and other resources to complete the development and to use or sell the intangible asset.

-

Its ability to measure reliably the expenditure attributable to the intangible asset during its development.

MFRS 138 provide an accounting policy choice to subsequently measure an intangible asset either using the cost model or the revaluation model.

MFRS 138 states that intangible assets may have a finite or indefinite useful life. This requires an entity to assess and determine useful life. An intangible asset with indefinite useful life is not amortised but must be tested for impairment annually.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Accounting in Associates

MPERS vs MFRS : Associates

In this article, we share the main differences in the accounting requirements for associates under MFRS 128 and Section 14 of MPERS.

Associates

Investment in associate refers to the investment in an entity in which the investor has significant influence but does not have full control like a parent and a subsidiary relationship. Usually, the investor has a significant impact when it has 20% to 50% of shares of another entity.

Section 14 of MPERS - Associates

Measure investment in associates

-

The cost model

Investment is measured at cost less impairment. The quoted associate must be measured at fair value.

-

The equity method

No exception for temporary investment and for conditions of severe restriction.

-

The fair value model

Investment is measured at fair value through profit and loss. Any investment which is impracticable to measure fair value must be measured using the cost model.

When an associate becomes a subsidiary or joint venture, a remeasurement is required with gain or loss recognized in P/L account

MFRS 128 - Associates

Measure investment in associates under the equity method in the consolidated financial statements.

No exception for temporary investment and for conditions of severe restriction.

When an associate becomes a subsidiary (not joint venture), a remeasurement is required.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Accounting in Associates

MPERS vs MFRS : Associates

In this article, we share the main differences in the accounting requirements for associates under MFRS 128 and Section 14 of MPERS.

Associates

Investment in associate refers to the investment in an entity in which the investor has significant influence but does not have full control like a parent and a subsidiary relationship. Usually, the investor has a significant impact when it has 20% to 50% of shares of another entity.

Section 14 of MPERS - Associates

Measure investment in associates

-

The cost model

Investment is measured at cost less impairment. The quoted associate must be measured at fair value.

-

The equity method

No exception for temporary investment and for conditions of severe restriction.

-

The fair value model

Investment is measured at fair value through profit and loss. Any investment which is impracticable to measure fair value must be measured using the cost model.

When an associate becomes a subsidiary or joint venture, a remeasurement is required with gain or loss recognized in P/L account

MFRS 128 - Associates

Measure investment in associates under the equity method in the consolidated financial statements.

No exception for temporary investment and for conditions of severe restriction.

When an associate becomes a subsidiary (not joint venture), a remeasurement is required.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

How to apply EOT 2022 from SSM?

SSM Extension of Time 2022

You can apply for extension of time (EOT) with SSM if you cannot meet the SSM deadline.

Requirement of the Companies Act, 2016

Section 258(1)(a) and 259(1)(a) of CA 2016

A Private Company is required to circulate the audited financial statements within 6 months from the financial year end and submit to SSM within 30 days from the circulation date.

How to apply?

Submit the application form [Section 259(2)] to SSM by filling in the information required

When to submit?

The company is required to submit the EOT application at least 7 days before the last day of circulation period.

What is the information required?

a) Details of the Company

-

Company name

-

Registered office address

-

Company registration number

-

Telephone, fax number and email address

b) Details of the application

-

Financial year end

-

Last date of circulation date

-

Proposed period of extension

-

(Generally, maximum 90 days)

-

Reason for application

Application fee

-

RM100 for each segment of EOT application.

-

Payable to SSM

Result of application

-

The application of EOT is subject to SSM approval.

-

SSM will issue a letter informing the applicant of the result of the application.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Market Development Grant - Part 1

MATRADE - Market Development Grant (MDG) RM300,000

What is MDG?

The Market Development Grant (MDG) is a support initiative in the form of a reimbursable grant. MDG was introduced in 2002 with the objective of assisting exporters in their efforts to promote Malaysian made products or services globally.

The lifetime limit of MDG is RM300,000 and it is specifically formulated for Malaysian SME Companies, Professional Service Providers, Trade and Industry Associations, Chambers of Commerce, Professional Bodies and Co-operatives.

[Note: MDG reimbursements are subject to the availability of the government funds]

What Activities Are Eligible For Grant Funding?

Physical Events

-

Participation in International Trade Fairs or Exhibitions held in Malaysia/Overseas

-

Participation in Trade & Investment Missions (TIM) or Export Acceleration Missions (EAM)

-

Participation in International Conferences Held Overseas

-

Listing Fees for Made in Malaysia Products in Supermarkets or Hypermarkets or Retail Centres or Boutique Outlets Located Overseas

Virtual Events

-

Participation in Virtual International Trade Fairs In Malaysia Or Overseas

-

Participation In Business To Business (B2B) Meetings Related To Virtual Trade Investment Missions And Export Acceleration Missions

Who Is Eligible To Claim For MDG? (please refer to MDG Guidelines)

-

Small And Medium Enterprises (SMEs)

-

Professional Service Providers (Sole Proprietor Or Partnership)

-

Trade & Industry Associations, Chambers Of Commerce Or Professional Bodies

-

Co-operatives

Source

-

Market Development Grant (MDG) Physical Events

-

Market Development Grant (MDG) Virtual Events

This message was brought to you by KTP

Market Development Grant

Marketing Development Grant (MDG) is an export support initiative in the form of a reimbursable grant.

It is eligible for those attend international trade fairs and event to promote Malaysia products or services in current or virtual form.

🎯𝐇𝐨𝐰 𝐜𝐚𝐧 𝐌𝐃𝐆 𝐡𝐞𝐥𝐩?

The marketing team start to arrange for this event.

They book the flight tickets, accommodation, liaise with the organizer, looking for suitable spot and booth and others necessary.

With the assistance of MDG, these expenses are reimbursable!

🎯𝐇𝐨𝐰 𝐝𝐨 𝐀𝐀𝐀 𝐦𝐚𝐤𝐞 𝐭𝐡𝐞 𝐜𝐥𝐚𝐢𝐦?

1) Registered as MATRADE member

The registration is simple, just visit the MATRADE official website as link below:

http://www.matrade.gov.my/…/onli…/register-as-matrade-member

And fill up your company information as required. Registration is free.

2) Make the claim online

AAA can claim the MDG within 30 days from the last date of promotion activity.

The application can be made online: www.matrade.gov.my/mdg

The documentations required is to proof your presence in this events, such as payment trails, flight ticket, exhibitor pass and others.

Please make sure you keep all the documentations and fully utilise the grant!

The maximum claimable amount is depending on types of event you joined. As for AAA, they are eligible for maximum up to RM25k.

Let's hope AAA achieves success in this event and comes back with a big victory!

This message was brought to you by KTP

Accounting for Investment Properties in Malaysia

MPERS vs MFRS : Investment Properties

In this article, we share the main differences in the accounting requirements for investment properties under MFRS 140 and Section 16 of MPERS.

Investment Properties

Investment property is property (land or a building – or part of a building – or both) held by the owner or by the lessee under a finance lease to earn rentals or for capital appreciation, or both, rather than for:

-

Use in the production or supply of goods or services, or for administrative purposes; or

-

Sale in the ordinary course of operations.

What is the accounting treatment for investment properties?

Section 16 of MPERS - Investment Properties

If the fair value can be measured reliably without undue cost or effort on an ongoing basis, the IP must be measured at the fair value model.

All other IP must be accounted for as property, plant and equipment using the depreciated cost model in Section 17 Property, Plant and Equipment.

MFRS 140 - Investment Properties

Measured at fair value or depreciated cost model

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Accounting for borrowing cost Malaysia

MPERS vs MFRS : Borrowing Cost

In this article, we share the main differences in the accounting requirements for borrowing costs under MFRS 123 and Section 25 of MPERS.

Borrowing Cost :

Borrowing costs are interest and other expenses incurred by an entity concerning the funds borrowed. Borrowing cost includes the following type of costs:

-

Interest on bank borrowings (both short-term and long-term) as well as bank overdrafts.

-

Amortisation of discounts or premiums relating to borrowings.

-

Amortisation of ancillary costs incurred in connection with the arrangement of borrowings.

-

Finance charges in relation to finance leases and service concession arrangements.

-

Exchange differences from foreign currency borrowings, to the extent that they are regarded as an adjustment to interest costs.

-

What is the accounting treatment for borrowing costs?

Section 25 of MPERS - Borrowing Cost

Recognise all borrowing costs as an expense in profit or loss in the period they are incurred. The option of capitalising borrowing costs on qualifying

assets are not allowed.

MFRS 123 - Borrowing cost

Borrowing costs that are directly related to a qualifying asset shall be capitalised as part of the cost of that asset.

Borrowing costs directly attributable to the acquisition, construction or production of a 'qualifying asset' (one that necessarily takes a substantial period of time to get ready for its intended use or sale) are included in the cost of the asset.

An entity shall cease capitalising borrowing costs when substantially all the activities necessary to prepare the qualifying asset for its intended use or sale are complete

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

MPERS vs MFRS Malaysia

MPERS vs MFRS : An overview of Accounting Standards in Malaysia

There are 2 types of accounting standards in Malaysia

-

MPERS : Malaysian Private Entities Reporting Standard

-

MFRS : Malaysian Financial Reporting Standards

Private Entities

Private entities shall comply with either:

1. Malaysian Private Entities Reporting Standard (MPERS) in their entirety for financial statements. or

2. Malaysian Financial Reporting Standards (MFRS) in their entirety.

A private entity is a private company as defined in section 2 of the Companies Act 2016 that –

-

is not itself required to prepare or lodge any financial statements under any law administered by the Securities Commission Malaysia or Bank Negara Malaysia; and

-

is not a subsidiary or associate of, or jointly controlled by, an entity which is required to prepare or lodge any financial statements under any law administered by the Securities Commission Malaysia or Bank Negara Malaysia.

Notwithstanding the above, a private company that is itself, or is a subsidiary or associate of, or jointly controlled by, an entity that is a management company as defined in section 2 of the Interest Schemes Act 2016 is not a private entity.

MPERS vs MFRS

More to come in coming days the comparison MPERS and MFRS

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Investment Tax Allowance Incentive Malaysia

Tax Incentives For The Manufacturing Sector : Investment Tax Allowance

The major tax incentives for companies investing in the manufacturing sector are the Pioneer Status and the Investment Tax Allowance.

Qualifying Criteria

Eligibility for Pioneer Status and Investment Tax Allowance is based on certain priorities, including the level of value-added, technology used and industrial linkages.

Eligible activities and products are termed as “promoted activities” or “promoted products”. (See Appendix I: List of Promoted Activities and Products – General)

The company must submit its application to MIDA before commencing operation/production.

(i) Investment Tax Allowance

As an alternative to Pioneer Status, a company may apply for Investment Tax Allowance (ITA). A company granted ITA is entitled to an allowance of 60% on its qualifying capital expenditure (factory, plant, machinery or other equipment used for the approved project) incurred within five years from the date the first qualifying capital expenditure is incurred.

The company can offset this allowance against 70% of its statutory income for each year of assessment. The remaining 30% of its statutory income will be taxed at the prevailing company tax rate.

Any unutilised allowance can be carried forward to subsequent years until fully utilised.

Applications should be submitted to MIDA.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Pioneer Status Incentive

Tax Incentives For The Manufacturing Sector : Pioneer Status

The major tax incentives for companies investing in the manufacturing sector are the Pioneer Status and the Investment Tax Allowance.

Qualifying Criteria

Eligibility for Pioneer Status and Investment Tax Allowance is based on certain priorities, including the level of value-added, technology used and industrial linkages.

Eligible activities and products are termed as “promoted activities” or “promoted products”. (See Appendix I: List of Promoted Activities and Products – General)

The company must submit its application to MIDA before commencing operation/production.

(i) Pioneer Status

A company granted Pioneer Status (PS) enjoys a five year partial exemption from the payment of income tax. It pays tax on 30% of its statutory income*, with the exemption period commencing from its Production Day (defined as the day its production level reaches 30% of its capacity).

Unabsorbed capital allowances incurred during the pioneer period can be carried forward and deducted from the post pioneer income of the company. Accumulated losses incurred during the pioneer period can be carried forward and deducted from the post pioneer income of the company for a period of seven consecutive years.

Applications for Pioneer Status should be submitted to MIDA.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Overview of The Malaysian Financial Reporting Standards (MFRS)

The Malaysian Financial Reporting Standards (MFRS)

Accounting Standards Malaysia

There are three types of approved accounting standards here in Malaysia:

-

The Malaysian Financial Reporting Standards (MFRS) – This is the MASB approved accounting standards for entities, but this does not include private entities

-

Private Entity Reporting Standards (PERS) – This is the MASB approved accounting standards for all private entities. However, this has been withdrawn effective 1 January 2016.

-

Malaysian Private Entities Reporting Standards (MPERS) – This replaces the previous PERS and is in effect from 1 January 2016.

MFRS

Entities Other Than Private Entities shall apply the MFRS framework for annual periods beginning on or after 1 January 2012, with the exception of entities that are permitted in the alternative to apply the Financial Reporting Standards (FRS) framework.

The Malaysian Financial Reporting Standards (MFRS) framework was introduced by the Malaysian Accounting Standards Board (MASB) and came into effect on 1 January 2012.

It is fully compliant with the International Financial Reporting Standards (IFRS) framework, which enhances the credibility and transparency of financial reporting in Malaysia.

The numbering of the MFRS corresponds with the equivalent IFRS Standard issued by the IASB. MFRS prefix with “1xx” corresponds with the equivalent IAS.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Case Study : Tax incentives on the manufacturing of animal feeds from MIDA ?

How to apply tax incentives on the manufacturing of animal feeds from MIDA ?

Tax Incentive Application for Animal Feed Ingredients

Under the Promotion of Investments Act 1986, Small Scale Manufacturing Companies are eligible for the following tax incentives for manufacturing promoted products or activities:

a) Pioneer Status with a full tax exemption for 5 years, or

b) Investment Tax Allowance can be offset against 100% of statutory income for 5 years of assessments.

Besides, the Company needs to full fill the SME definition as follows to apply this tax incentive:

a) Companies with shareholders’ funds of up to RM500,000 with at least 60% Malaysian equity

b) Companies with shareholders’ funds of above RM500,000 and not exceeding RM2.5 million with 100% Malaysian equity.

Scenario

XYZ Sdn Bhd (Name changed to protect the privacy of the Company) is a new transfer client to the KTP Group of Companies. During the discussion with directors, we understand that the Company has the intention to manufacture animal feed supplements. The supplements will help the cows to produce more milk.

Thus, we have studied and identified the tax incentive for this business nature. Manufacturing animal feed is one of the promoted activities listed under Small Scale Manufacturing Companies (Appendix III).

Struggles

Firstly, we have contacted the MIDA officer to confirm manufacturing of animal supplements is fall under animal feed ingredients.

Following that we have arranged a virtual meeting with the MIDA officer and the Company directors. Prior to the meeting, the MIDA officer asks for some details as follows for an initial discussion with the client.

The information required such as:

a) shareholders fund and

b) employment,

c) project cost,

d) raw materials and

e) process flow chart.

Solution

After providing the details, the officer has further studied in detail and guided us on the application of the tax incentive to the next steps.

Source:

http://www.ctim.org.my/file/news/15/00141_Tax%20Incentive%20for%20Small%20Scale%20Manufacturing%20Companies.pdf

https://www.mida.gov.my/wp-content/uploads/2020/12/20200425151042_Appendix20III20Small20Company.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Should I declare rental income in Malaysia

What happen if you don’t declare rental income?

Omission of Rental Income

Any person who makes an incorrect return by omitting or understating any income.

Penalty

S113(1)(a) of the Income Tax Act

Make an incorrect return by omitting or understating any income

RM1,000 to RM10,000 and 200% of tax undercharged

S113(1)(b) of the Income Tax Act

Give any incorrect information affecting the tax liability

RM1,000 to RM10,000 and 200% of tax undercharged

S114 of the Income Tax Act

Wilfully and intent to evade or assist any other person to evade tax

RM1,000 to RM20,000 or imprisonment not exceeding 3 years and 200% of tax undercharged

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks