Blog

Tax case on bad debts write off

Frustrated when IRB adds back your bad debts in a tax audit.

Time is bad, pandemic cause bad debts to rise. Learn IRB official guidelines on bad debt tax treatment.

Why?

Bad debt is always our tax authority focus area. 100% guarantee !

Let’s learn this tax case on IRB fight on bad debts: Quality Concrete Holdings Berhad vs Ketua Pengarah Hasil Dalam Negeri.

In YA 2004, Quality Concrete Holdings Berhad (QCHB) claimed for tax deduction on bad debts of RM608,731.25 (balance of value work done: RM950,000.00). IRB disallowed the deduction on bad debts written off and imposed a penalty under Section 113(2) of the Income Tax Act 1967 (ITA 1967).

IRB argued that:

QCHB did not recognised the value of work done (i.e. RM950,000.00) as gross income for the year of assessment (YA) 1999 up to YA 2004.

Therefore, the deduction of bad debt should be disallowed according to Section 24 and 34 of ITA 1967:

“The amount of the debt shall be treated as gross income of the relevant person from the business

for the relevant period.”

QCHB argue …

The claim amount had been reported under the trade debtors account in the Balance Sheet as at 31.01.1998 for YA 1999.

The claim for the bad debt should be allowable according to Section 24(1)(b) of ITA 1967:

“any services rendered at any time in the course

of carrying on a business.”

QCHB argued it is a trade debt arising in respect of carrying on a business irrespective of where and how the sum of RM950,000.00 was entered and described in the account.

QCHB had acted in good faith and the impugned assessment involved technical interpretation. Thus, penalty should not be imposed.

The decision from the court :

Agreed with IRB tax treatment on deduction of bad debt is disallowed under Section 34(2) of the ITA 1967.

Technical interpretation and good faith are not valid defenses for penalty under Section 113(2) of ITA 1967.

Thus, the penalty imposed under Section 113(2) of ITA 1967 is correct because QHCB had filed an incorrect return and gave incorrect information.

Visit Us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#irb

#lhdn

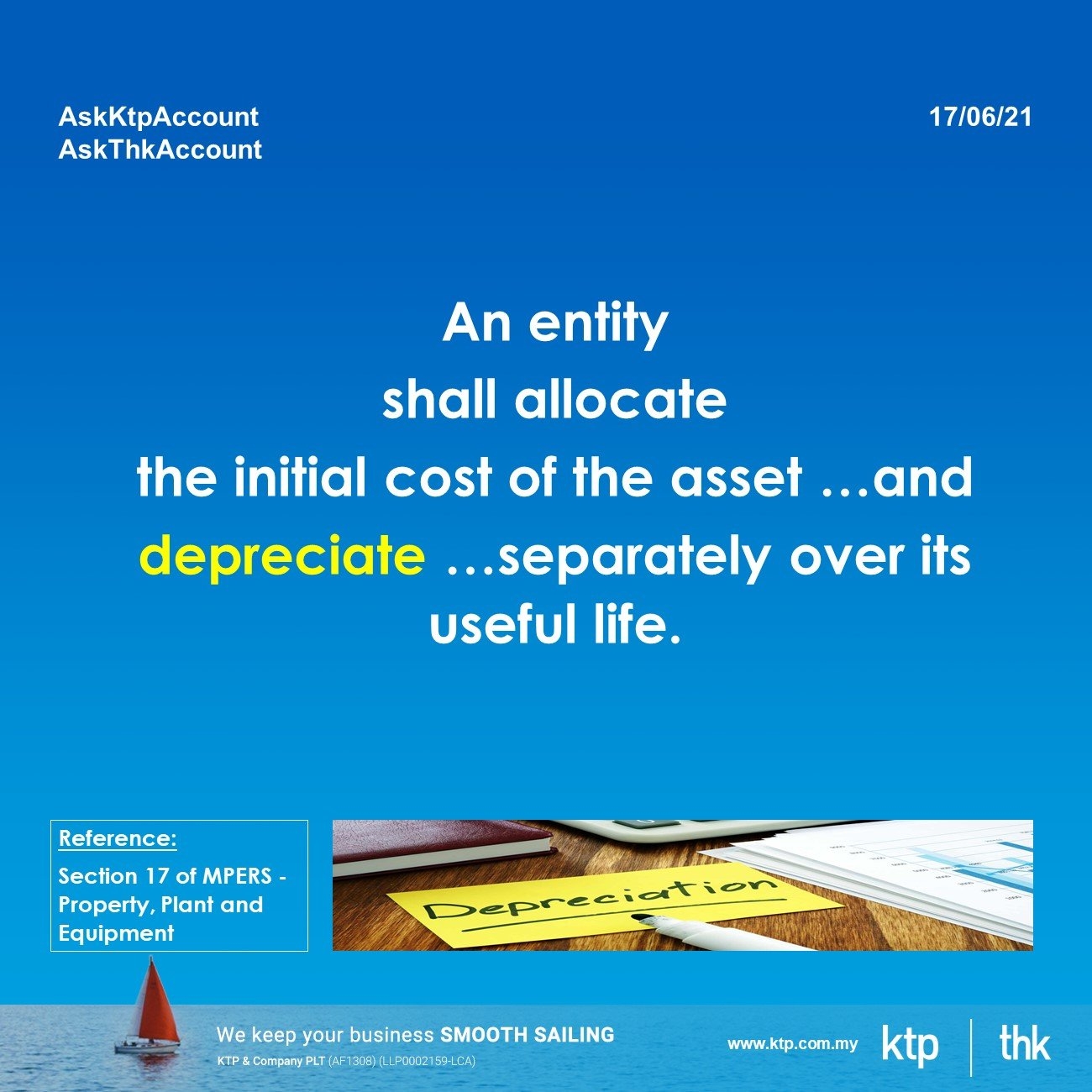

Provision of depreciation

Auditor! Can I don't charge depreciation in my account this year as my company makes loss due to Covid?

I need to borrow money from the bank?

Key summary from the MPERS Section 17 of MPERS -Property, Plant and Equipment

An entity shall allocate the initial cost of the asset …and depreciate …separately over its useful life.

With some exceptions, such as quarries and sites used for landfills, land has an unlimited useful life and therefore is not depreciated.

The depreciation charge for each period shall be recognised in profit or loss…

Depreciation of an asset begins when it is available for use, ie when it is in the location and condition ….

Depreciation of an asset ceases when the asset is derecognized.

Depreciation does not cease when the asset becomes idle or is retired from active use unless the asset is fully depreciated

Auditor opinion :

You still have to charge depreciation in the account!

But …

You can try the following methods and change

* Useful life of assets

* Financial year-end

* Name of company

Visit Us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#irb

#lhdn

Tax issue on 𝐂𝐨𝐦𝐩𝐞𝐧𝐬𝐚𝐭𝐢𝐨𝐧 𝐫𝐞𝐜𝐞𝐢𝐯𝐞𝐝 𝐨𝐧 𝐜𝐨𝐦𝐩w

𝐂𝐨𝐦𝐩𝐞𝐧𝐬𝐚𝐭𝐢𝐨𝐧 𝐫𝐞𝐜𝐞𝐢𝐯𝐞𝐝 𝐨𝐧 𝐜𝐨𝐦𝐩𝐮𝐥𝐬𝐨𝐫𝐲 𝐨𝐟 𝐥𝐚𝐧𝐝 𝐟𝐫𝐨𝐦 𝐠𝐨𝐯𝐞𝐫𝐧𝐦𝐞𝐧𝐭 𝐢𝐬 𝐭𝐚𝐱𝐚𝐛𝐥𝐞?

Overview of compulsory acquisition of land.

Compulsory acquisition is the power of the government to acquire private rights in a land without the willing consent of its owner or occupant in order to benefit society.

The compensation amount of acquisition is determined by the government.

𝗞𝗲𝘆 𝘁𝗮𝗸𝗲𝗮𝘄𝗮𝘆𝘀:

You will understand: -

1. Criteria to meet compulsory acquisition of land

2. Tax treatment on compulsory of acquisition of land-based on real tax case

𝐒𝐮𝐦𝐦𝐚𝐫𝐲 𝐨𝐟 𝐥𝐞𝐚𝐫𝐧𝐢𝐧𝐠𝐬:

Compulsory acquisition of land did not fall under the gross income unless the taxpayer when obtaining the said land had knowledge that it would be acquired by the government.

𝐖𝐡𝐚𝐭 𝐚𝐫𝐞 𝐭𝐡𝐞 𝐜𝐫𝐢𝐭𝐞𝐫𝐢𝐚 𝐭𝐨 𝐦𝐞𝐞𝐭 𝐜𝐨𝐦𝐩𝐮𝐥𝐬𝐨𝐫𝐲 𝐚𝐜𝐪𝐮𝐢𝐬𝐢𝐭𝐢𝐨𝐧 𝐨𝐟 𝐥𝐚𝐧𝐝?

1.There is no intention to sell the land.

2. During the purchase of the land, the owner should not aware of any government’s intention to acquire the land.

Tax treatment on compulsory acquisition of land-based on real tax case: Penang Realty Sdn. Bhd. v. Ketua Pengarah Hasil Dalam Negeri

A parcel of land was compulsorily acquired by the Government in August 1980 and was paid the sum of RM1,035,762.91 as compensation. IRB is claiming tax for the said compensation.

Penang Realty Sdn. Bhd. didn’t agree. The acquisition was compulsorily acquired and there is no intention to trade the land.

IRB argument - Gain on the disposal of land is taxable under section 4 of the Income Tax Act 1967 (ITA).

The decision by The Court

The proceeds received were not subject to income tax as the Company is no intention to trade the land and it was the compulsory acquisition of land.

𝐒𝐨𝐮𝐫𝐜𝐞𝐬:

http://lampiran2.hasil.gov.my/pdf/pdfam/PREALTYvsKPHDN.pdf

Visit Us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#irb

#lhdn

营业前的费用

1. 含义- 营业前的费用

营业前的费用 (Preliminary Expenses/Pre-Operating Expenses)

在公司开始运作之前有些费用是务必要花的,这些费用在会计的角度就是营业前的费用。

这些费用基本包括(并不是每个费用将获得扣税资格):

· 市场调查与研究费用

· 律师与秘书费用

· 公司成立的专业的咨询费用

· 招聘与培训员工的费用

· 行政费用等等

2. 复式进账法

Debit 营业前的费用 (Income Statement - Expenses)

Credit 现金 (Balance Sheet - Current Asset)

3. 费用扣税资格与条件

一般上,公司营业前所产生的费用都是无法扣税的。但是某些费用在一定的条件下是可以扣税的。条件如下:

- 该公司必须成立与坐落于马来西亚,商业活动也必须获得财政部长的批准。

例如:市场调查与研究费用,以市场调查为目标的国外交通费与每日不超过四百令吉的国外生活花费都能扣税。

- 该公司的注册法定资本不可超过2,500,000令吉。

例如:注册公司的相关手续费,准备与打印公司章程费,印花税与公司印章费都是可扣税的。

- 生产业公司培训员工的费用可享有双重扣税的福利,但必须达到以下条件:培训费须在营业前发生,培训内容须与产品未来的生产相关,培训计划的机构须获得马来西亚工业发展局(MIDA)与财政部长的批准,培训的员工必须是马来西亚公民。

4. 例子

陈先生于2020年2月15日在马来西亚注册成立,法定资本为500,000令吉。他于2020年4月1日开始从事汽车零件零售业务,并于每年的3月31日作为年度结账。截至2021年3月31日, 该公司的营业前费用有:申请生意上的准证,文书注册,公司章程备忘录及印花税。这些费用总共是4,500令吉。

复式进账法:

Debit 营业前的费用 - 4,500令吉

Credit 现金 - 4,500令吉

这些费用在税务上可进行扣税,原因是这些费用属于可扣税费用与法定资本少于2, 500,000令吉。

欲知更多可参考以下网址:

IRB Public Ruling - PRE-OPERATIONAL BUSINESS EXPENDITURE PUBLIC RULING NO.11/2013

http://phl.hasil.gov.my/pdf/pdfam/PR_11_2013.pdf

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

What is the difference between Provision and Liability in accounting

Why do auditors keep asking company’s lawsuit status? Why is it so important?

You know the lawsuit is a very slow and irritating one! How I know!

What is the difference between ‘Provision’ and ‘Liability’?

Provision: a liability of uncertain timing or amount.

Liability:

- present obligation as a result of past events

- settlement is expected to result in an outflow of resources (payment)

Provision :

3 criteria are required to be met before a provision can be recognised. These are:

- There needs to be a present obligation (legal/ contractual) from a past event

- There needs to be a reliable estimate (best estimate/ expected value)

- There needs to be a probable outflow (high chance)

What is the difference between ‘Contingent liability’ and ‘Contingent asset’?

These two categories should only be disclosed in financial statements but not recognised in accounts.

Contingent liability :

- a possible obligation depending on whether some uncertain future event occurs, or

- a present obligation but payment is not probable or the amount cannot be measured reliably

Contingent asset :

- a probable asset that arises from past events, and

- whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity.

Example

Contingent Liability:

- Pending lawsuit, product warranty or pending investigation

- The outcome is unknown

- If possible to lose, disclose a contingent liability

- If probable to lose, recognise the provision

Contingent Asset :

- Pending lawsuit, insurance claim

- The outcome is probable

- If probable to receive income (by lawyer or insurance company), disclose contingent asset

- If virtually certain to receive income (subsequently proof by supporting), recognise asset

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

When can a company be voluntarily wind up?

- Duration under company constitution expires

- A resolution (majority of shareholders) is passed in general meeting

- Triggering event stated in the company constitution & resolution pass in general meeting

- Special Resolution (3/4 majority of shareholders)

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

IRB FAQ (updated) 3 June 2021

Our Inland Revenue Board (IRB) has issued an updated version of the FAQ dated 3 June 2021 (after the original FAQ dated 2 June 2021).

Take note of the key updates before the FAQ changes again in view of the anticipated extension of lockdown.

Notification of new employee (Form CP22)

Submission of the Form CP22 can be made through the Customer Feedback Form

on the IRB’s Official Portal.

Tax clearance letter

Tax clearance letter will be processed after all documents and information are furnished completely.

The application for the tax clearance letter can be submitted through:

1. e-SPC

2. the Customer Feedback Form on the IRB’s Official Portal.

Tax estimates (Form CP204) & Notification of change in an accounting period (Form CP204B)

Application for extension of time (EOT) for the above forms is no longer required as EOT is now given until 31 July 2021 for submission of the above forms.

Revised tax estimates (Form CP204A & Form CP502)

Application for EOT for the above forms is no longer required with EOT already given until 31 July 2021 for submission of the above forms.

Deferment of tax payment (Form CP204 & Form CP500)

Tourism, Cinema and Spa industries

The deferment of payment of CP204 (monthly installment of tax estimates) and CP500 (bi monthly installments for individuals) will apply for taxpayers with business activities under the tourism, cinema and spa industries.

These taxpayers will be identified based on the business code from their latest income tax returns filed with the IRB.

The deferment will be provided automatically to the eligible taxpayers.

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#IRB

#LHDN

HRDF exemption 2021

HRDF Exemption

Exemption of HRDF levy payment extend to 31.12.2021 (6 months) only if .... otherwise to 30.06.2021 (1 month) exemption.

All registered employer under the scope is eligible for the exemption!

-

6 months exemption if you are registered under the expanded scope;

-

1 month if you are registered under the original scope.

Source:

1. Recap to our post - Pemerkasa 2021

https://www.facebook.com/.../pcb.../5612191385489776

2. PSMB Act 2001

https://hrdcorp.gov.my/.../PEMBANGUNAN-SUMBER-MANUSIA...

3. PSMB (Exemption of levy) (No.2) Order 2021

https://lom.agc.gov.my/.../outputp/1702270/PUA%20251.pdf...

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#HRDF

您对公司营业前的费用知道多少呢?

您对公司营业前的费用知道多少呢?

相信很多老板们在营业之前都需要准备一笔筹备费用. 然而,您是否对这些费用在账上面处理的方式有所困惑?

别担心,就让我们给您一个概念吧!

1. 含义- 营业前的费用

营业前的费用 (Preliminary Expenses/Pre-Operating Expenses)

在公司开始运作之前有些费用是务必要花的,这些费用在会计的角度就是营业前的费用。

这些费用基本包括(并不是每个费用将获得扣税资格):

· 市场调查与研究费用

· 律师与秘书费用

· 公司成立的专业的咨询费用

· 招聘与培训员工的费用

· 行政费用等等

2. 复式进账法

Debit 营业前的费用 (Income Statement - Expenses)

Credit 现金 (Balance Sheet - Current Asset)

3. 费用扣税资格与条件

一般上,公司营业前所产生的费用都是无法扣税的。但是某些费用在一定的条件下是可以扣税的。条件如下:

- 该公司必须成立与坐落于马来西亚,商业活动也必须获得财政部长的批准。

例如:市场调查与研究费用,以市场调查为目标的国外交通费与每日不超过四百令吉的国外生活花费都能扣税。

- 该公司的注册法定资本不可超过2,500,000令吉。

例如:注册公司的相关手续费,准备与打印公司章程费,印花税与公司印章费都是可扣税的。

- 生产业公司培训员工的费用可享有双重扣税的福利,但必须达到以下条件:培训费须在营业前发生,培训内容须与产品未来的生产相关,培训计划的机构须获得马来西亚工业发展局(MIDA)与财政部长的批准,培训的员工必须是马来西亚公民。

4. 例子

陈先生于2020年2月15日在马来西亚注册成立,法定资本为500,000令吉。他于2020年4月1日开始从事汽车零件零售业务,并于每年的3月31日作为年度结账。截至2021年3月31日, 该公司的营业前费用有:申请生意上的准证,文书注册,公司章程备忘录及印花税。这些费用总共是4,500令吉。

复式进账法:

Debit 营业前的费用 - 4,500令吉

Credit 现金 - 4,500令吉

这些费用在税务上可进行扣税,原因是这些费用属于可扣税费用与法定资本少于2, 500,000令吉。

欲知更多可参考以下网址:

IRB Public Ruling - PRE-OPERATIONAL BUSINESS EXPENDITURE PUBLIC RULING NO.11/2013

http://phl.hasil.gov.my/pdf/pdfam/PR_11_2013.pdf

Visit Us

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#irb

#lhdn

Remission of GST Penalty under MCO 3.0

Income Tax under MCO 3.0

Read the full story in our blog

https://www.ktp.com.my/blog/irb-faq-mco3/08june2021

MCO 3.0常问所得税8️问题

Read the full story in our blog

https://www.ktp.com.my/blog/irb-eot-part3/08june2021

马来西亚-延税攻略2

Read the full story in our blog

https://www.ktp.com.my/blog/irb-eot-part2/04june2021

𝐈𝐑𝐁 𝐰𝐢𝐥𝐥 𝐭𝐚𝐱 𝐲𝐨𝐮𝐫 𝐜𝐚𝐬𝐮𝐚𝐥 𝐢𝐧𝐜𝐨𝐦𝐞 𝐰Ү

👉Overview of casual profit/income

A casual profit is an income which, received by a person from an activity outside his ordinary trade or vocation, but which nevertheless is a profit or income item accruing to him by virtue of services rendered or a receipt payment from property not chargeable elsewhere.

👉Key takeaways:

You will understand: -

1. What is casual profit or income?

2. Tax treatment of casual profit or income based on real tax case.

👉Summary of learnings:

Casual profits or income is chargeable under section 4(f) of the Income Tax Act (ITA) 1967.

👉What is the casual profit or income?

Payments for services are income even where there is no repetition, such as the followings:

✅Commissions paid to a director for guaranteeing bank overdrafts or bank loans.

✅Brokerage fees

✅Introduction fees

✅Fees for the occasional hosting as the master of ceremony, fees for the occasional newspaper articles, or the giving ad-hoc lectures.

👉Tax treatment on casual profit or income based on real tax case ABM v. KETUA PENGARAH HASIL DALAM NEGERI (PKCP (R) 780/2017)

IRB raised a tax query of the source of income arose to purchase an asset under taxpayer and his wife. The source of income of RM750,000 is arriving from for introduction fees and this income was not reported.

Decision by The Court The final judgement is the income of RM750,000 are taxable under section 4(f) ITA 1967.

👉Sources: http://phl.hasil.gov.my/pdf/pdfam/ABM_v_KPHDN_21012021.pdf

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏 (𝐀𝐮𝐝𝐢𝐭,𝐓𝐚𝐱, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

Website www.ktp.com.my

Instagram https://bit.ly/3jZuZuI

Linkedin https://bit.ly/3sapf4l

Telegram http://bit.ly/3ptmlpn

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

Website www.thks.com.my

Facebook https://bit.ly/3nQ98rs

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (𝐎𝐮𝐫 𝐢𝐧𝐭𝐞𝐫𝐧𝐚𝐥 𝐜𝐨𝐦𝐦𝐮𝐧𝐢𝐭𝐲 𝐟𝐨𝐫 𝐨𝐮𝐫 𝐜𝐨𝐥𝐥𝐞𝐚𝐠𝐮𝐞𝐬)

Tiktok http://bit.ly/3u9LR6Q

Youtube http://bit.ly/3ppmjyE

Facebook http://bit.ly/3ateoMz

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (𝐎𝐮𝐫 𝐞𝐱𝐭𝐞𝐫𝐧𝐚𝐥 𝐣𝐨𝐛 𝐜𝐨𝐦𝐦𝐮𝐧𝐢𝐭𝐲 𝐟𝐨𝐫 𝐢𝐧𝐭𝐞𝐫𝐧𝐬, 𝐠𝐫𝐚𝐝𝐮𝐚𝐭𝐞𝐬 & 𝐞𝐱𝐩𝐞𝐫𝐢𝐞𝐧𝐜𝐞𝐝 𝐜𝐚𝐧𝐝𝐢𝐝𝐚𝐭𝐞𝐬 )

Instagram https://bit.ly/3u2PxHg

Facebook http://bit.ly/3rPxz9o

We are one-stop (2️⃣0️⃣years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

马来西亚-延税攻略

Extension of deadline under lockdown @ 02/06/21

SSM

Extension of time for a period of 90 days for fiancial year 31 October 2021 to 31 January 2021

IRB, EPF & Sosco

No news as at 02/06/21

Type of winding up and restructuring in Malaysia

Do you know the types of insolvency and restructuring in Malaysia?

Insolvency (winding up)

-

Volunatry winding up

- By members/sharesholders

- By creditors

-

Involuntary winding up

- By court

-

Voluntary restructuring

- Scheme of arrangement

- Corporate voluntary arrangement

-

Involuntary restructuring

-

Judicial management

-

Judicial management

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫

Tax matters under Pemerkasa

https://www.ktp.com.my/blog/tax-matters-pemerkasa/01june2021

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

WFH during lockdown 1/6-14/6

To All KTP THK Clients

In compliance with the nationwide lockdown requirements, KTP THK will close our premises from 1 –14 June 2021 and our colleagues will be instructed to work from home (WFH) pending further directives from the Government.

KTP THK will continue to closely monitor the situation, maintain close communication with our clients of any future developments.

Please follow our update in social media, email, whatsapp & etc..

We thank you for your understanding and patience and we hope that everyone will stay safe.

PS #1 Senior Minister (Security Cluster) Datuk Seri Ismail Sabri Yaakob on 30 May 2021 announced the SOPs for the nationwide lockdown that will be enforced from 1 - 14 June 2021. The full list of approved essential services and operations allowed as well as the permitted movement controls can be accessed here #1, while the list of prohibited services, operations and activities can be accessed here #2.

PS #2 It was also announced that essential activities in the Manufacturing and Manufacturing Related Sectors (MRS) will be allowed to operate during the nationwide lockdown, subject to approval from the Ministry of International Trade and Industry (MITI). For a full list of SOPs for sectors allowed to operate during the nationwide lockdown, please click here #3 . Effective 31 May 2021, all existing permission letters issued by MITI will no longer be valid and companies are required to refer to the relevant ministries regulating their sectors or the National Security Council (MKN).

Source :

Approved essential services and operation (here#1)

https://media.malaysianow.com/wp-content/uploads/2021/05/30184158/RINGKASAN-SOP-PKP-MKN-30-MEI-2021-DIBENARKAN-V4.pdf

Prohibited services and operation (here #2)

https://media.malaysianow.com/wp-content/uploads/2021/05/30190042/RINGKASAN-SOP-PKP-MKN-30-MEI-2021-TIDAK-DIBENARKAN-V3-1.pdf

SOP PKP (here #3)

https://www.mkn.gov.my/web/ms/sop-pkp/

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#lockdown

#covid19

Why?

Improve the quality of services to VIP taxpayer (aka more audit in the future) as per IRB press statement.

Read the full story in our blog

https://lnkd.in/gpGp6AA

Source

IRB press statement on Large Taxpayer Branch

https://lnkd.in/gEjVs-p

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

𝐊𝐓𝐏 (𝐀𝐮𝐝𝐢𝐭,𝐓𝐚𝐱, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

Website www.ktp.com.my

Instagram https://bit.ly/3jZuZuI

Linkedin https://bit.ly/3sapf4l

Telegram http://bit.ly/3ptmlpn

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

Website www.thks.com.my

Facebook https://bit.ly/3nQ98rs

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞

(𝐎𝐮𝐫 𝐢𝐧𝐭𝐞𝐫𝐧𝐚𝐥 𝐜𝐨𝐦𝐦𝐮𝐧𝐢𝐭𝐲 𝐟𝐨𝐫 𝐨𝐮𝐫 𝐜𝐨𝐥𝐥𝐞𝐚𝐠𝐮𝐞𝐬)

Tiktok http://bit.ly/3u9LR6Q

Youtube http://bit.ly/3ppmjyE

Facebook http://bit.ly/3ateoMz

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫

(𝐎𝐮𝐫 𝐞𝐱𝐭𝐞𝐫𝐧𝐚𝐥 𝐣𝐨𝐛 𝐜𝐨𝐦𝐦𝐮𝐧𝐢𝐭𝐲 𝐟𝐨𝐫 𝐢𝐧𝐭𝐞𝐫𝐧𝐬, 𝐠𝐫𝐚𝐝𝐮𝐚𝐭𝐞𝐬 & 𝐞𝐱𝐩𝐞𝐫𝐢𝐞𝐧𝐜𝐞𝐝 𝐜𝐚𝐧𝐝𝐢𝐝𝐚𝐭𝐞𝐬 )

Instagram https://bit.ly/3u2PxHg

Facebook http://bit.ly/3rPxz9o

We are one-stop (2️⃣0️⃣years+ history) audit, tax, secretarial, accounting, and payroll firms that commit to help and grow our client's business.

#ktplifestyle

#ktpcareers

#KTP

#Thk

#IRB

#LHDN

#largetaxpayerbranch