Blog

WFH during lockdown 1/6-14/6

To All KTP THK Clients

In compliance with the nationwide lockdown requirements, KTP THK will close our premises from 1 –14 June 2021 and our colleagues will be instructed to work from home (WFH) pending further directives from the Government.

KTP THK will continue to closely monitor the situation, maintain close communication with our clients of any future developments.

Please follow our update in social media, email, whatsapp & etc..

We thank you for your understanding and patience and we hope that everyone will stay safe.

PS #1 Senior Minister (Security Cluster) Datuk Seri Ismail Sabri Yaakob on 30 May 2021 announced the SOPs for the nationwide lockdown that will be enforced from 1 - 14 June 2021. The full list of approved essential services and operations allowed as well as the permitted movement controls can be accessed here #1, while the list of prohibited services, operations and activities can be accessed here #2.

PS #2 It was also announced that essential activities in the Manufacturing and Manufacturing Related Sectors (MRS) will be allowed to operate during the nationwide lockdown, subject to approval from the Ministry of International Trade and Industry (MITI). For a full list of SOPs for sectors allowed to operate during the nationwide lockdown, please click here #3 . Effective 31 May 2021, all existing permission letters issued by MITI will no longer be valid and companies are required to refer to the relevant ministries regulating their sectors or the National Security Council (MKN).

Source :

Approved essential services and operation (here#1)

https://media.malaysianow.com/wp-content/uploads/2021/05/30184158/RINGKASAN-SOP-PKP-MKN-30-MEI-2021-DIBENARKAN-V4.pdf

Prohibited services and operation (here #2)

https://media.malaysianow.com/wp-content/uploads/2021/05/30190042/RINGKASAN-SOP-PKP-MKN-30-MEI-2021-TIDAK-DIBENARKAN-V3-1.pdf

SOP PKP (here #3)

https://www.mkn.gov.my/web/ms/sop-pkp/

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#lockdown

#covid19

tax deduction on entertainment.

Confused over tax deduction on entertainment.

Let's refresh LHDN ruling on 100% tax deduction on entertainment

Please read full story in our blog

https://www.ktp.com.my/blog/100-tax-deduction-entertainment/28may2021

𝐊𝐓𝐏 (𝐀𝐮𝐝𝐢𝐭,𝐓𝐚𝐱, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫

what is capital statement in tax investigation

How IRB detect individual taxpayer’s under-reported income?

Overview

On 20.12.2020, Inland Revenue Board (IRB) published an article “Should Capital Statement be made law in Malaysia?” in The Star Malaysia. Most of the taxpayers will come with a doubt on how IRB determine whether individual has under-reported profit or income.

Key takeaway

You will understand:

1. What is capital statement

2. Why capital statement so important?

3. What we need to do?

Summary of learning

What is capital statement?

1. Capital statement is a statement to show the net worth of an individual.

2. It consists of:

- CP102 (Pin 10/80): Statement of Personal & Private Expenses (Equivalent to Income Statement)

- CP103 (Pin 5/96): Statement of Net Assets (Equivalent to Balance Sheet)

Why capital statement so important?

1. Capital statement is a tool used by LHDN to analyse individual taxpayer’s reported tax amount, and to detect any under-reporting or evasion of income.

2. The basic formula is Income = Saving + Spending

- It means each person earning should equal to their “Saving and Spending”.

- Individual tax payer has to be aware of any surplus of saving or spending as it will expose to LHDN as signal of unreported income.

3. All figures in the capital statement must be supported by documentary evidence.

4. LHDN has the power to raise additional tax payables based on “best judgement assessment” if taxpayer:

- unable to explain the surplus or deficit in the capital statement.

- fail to keep records or supporting documents.

What we need to do?

1. To prepare a capital statement earlier to avoid any uncertainty on the movement of funds.

2. To keep all the supporting documents / evidence on income and money spent.

3. To prepare on a yearly basis to avoid memory loss on income earned or expenses spent.

Reference:

http://phl.hasil.gov.my/pdf/pdfam/20201220_The_Star_Should_Capital_Statement_Be_Made_Law_In_Malaysia.pdf

https://www.thestar.com.my/news/nation/2020/12/20/should-capital-statement-be-made-law-in-malaysia

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#personaltax

#irb

#LHDN

Tax treatment on Investment Holding Company

𝐈𝐬 𝐦𝐲 𝐩𝐫𝐨𝐩𝐞𝐫𝐭𝐲 𝐝𝐞𝐯𝐞𝐥𝐨𝐩𝐞𝐫 𝐜𝐨𝐦𝐩𝐚𝐧𝐲 𝐛𝐞𝐜𝐨𝐦𝐞 𝐈𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐇𝐨𝐥𝐝𝐢𝐧𝐠 𝐂𝐨𝐦𝐩𝐚𝐧𝐲 (𝐈𝐇𝐂) 𝐦𝐚𝐜𝐚𝐦 𝐢𝐧𝐢? 𝐚𝐧𝐝 𝐤𝐞𝐧𝐚 𝐭𝐚𝐱 𝟐𝟒%

If

-

A property developer company completed and sold completed units,

-

Now only …receive interest income from fixed deposit

-

But ….the company has some vacant lands in its book

Our opinion :

-

The company is not dormant

-

The company has business operating expense.

-

The company has incurred capital expenditure (subdivision, submit plan…)

-

So …the company is not IHC.

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, legal or other professional advice. Please refer to your advisors for specific advice.

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#personaltax

#irb

#LHDN

平时注意这些行为,可能导致你被税收局盯上

Read the full story in our blog

https://www.ktp.com.my/blog/red-flag-tax/25may2021

Source :

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏 (𝐀𝐮𝐝𝐢𝐭,𝐓𝐚𝐱, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫

MACC arrest audit firm

Two senior staffs of an audit firm have been arrested for allegedly falsifying a company’s finances in a bid to cheat the taxman.

They were arrested at the Malaysian Anti-Corruption Commission (MACC) headquarters.

They were remanded to assist in the investigation under Section 16 (b)(A) of the MACC Act.

Full story in the link https://bit.ly/3fusChF.

Do you know they can be remanded under 113(1)(b) of Income Tax Act - Give any incorrect information in matters affecting the tax liability of a taxpayer or any other person?

Do you know they can be remanded under 114(1) of Income Tax Act - Wilfully and with intent to evade or assist any other person to evade tax?

Do you know they can be remanded under 114(1A) of Income Tax Act - Assist or advise (without reasonable care) others to under declare their income?

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#personaltax

#irb

#LHDN

#MACC

所得税罚款配套 Income Tax Offences Part 2

3分钟看完所得税罚款配套 Income Tax Offences Part 2

-

无法保留正确的记录和文档 - RM300.00至RM10,000.00 /监禁不超过1年/两者

-

无法遵守IRBM要求提供某些信息的通知 - RM200.00至RM20,000.00 /监禁不超过6个月/两者

-

在3个月内未通知地址更改 - RM200.00至RM20,000.00 /监禁不超过6个月/两者

-

4月30日之后交税 (non business) -10%罚款应纳税额

-

6月30日之后交税 (business)- 10%罚款应纳税额

-

在截止日期的30天后分期付款 - 10%罚款应纳税额

-

实际税款比修订后的税款估算高出30% - 实际税收余额和估计税收的差额的10%

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#personaltax

#irb

#LHDN

what is cp 204 ? how to pay cp 204 ?

What is CP204 Estimation of Tax Payable?

Overview

Every companies (a company, limited liability partnership, trust body or co-operative society) are required to determine the estimated tax payable and submit by using CP204 to IRB.

Key takeaway

You will understand:

1. What is CP204?

2. When is the due date for initial submission?

3. When to pay for the instalment?

4. How to determine the estimated tax payable for initial submission?

5. How to do for the revision of CP204?

6. What is the consequences for non-submission, late payment of CP204 and underestimated of tax estimation?

Summary of learning

1. What is CP204?

CP204 is the prescribed form for initial submission for estimated tax payable.

CP204A is the prescribed form for revision of estimated tax payable.

2. When is the due date for initial submission?

For existing company

The tax estimate must be submitted not less than 30 days before the beginning of the basis period.

For example, if the Company’s basis period is from 01.01.2021 – 31.12.2021, the initial submission of CP204 will fall on November 2020.

For newly incorporate company

The tax estimate must be submitted within 3 months after the commencement of business.

3. When to pay for the instalment?

The instalment payment must be made before 15th of the second month of the basis period.

For example, if the Company’s basis period is from 01.01.2021 – 31.12.2021, the payment for first instalment must be made before 15.02.2021.

4.How to determine the estimate of tax payable for initial submission?

For existing company

The tax estimate must not be less than 85% of the revised tax estimate or tax estimate for the immediately preceding Year of Assessment.

For example, if the Company’s last CP204/CP204A is RM10,000, the tax estimate for initial submission must not be less than RM8,500.

5.How to do for the revision of CP204?

The company is allowed to do the revision of an estimate of tax payable on 6th month or 9th month or both by using the Revised Estimate of Tax Payable Form (CP204A) through the electronic medium.

6. What is the consequences for non-submission, late payment of CP204 and underestimated the tax estimation?

Non-submission of CP204

Under subsection 120(1)(f) of the Income Tax Act 1967, taxpayer is liable to a fine of RM200 – RM20,000 or to imprisonment for a term not exceeding six months or both.

Late payment of CP204

A 10% penalty will be imposed on the balance of unpaid tax payable which the company fails to pay the monthly instalment before 15th of the month.

Underestimated for tax estimation

If the tax payable exceeds the estimation by more than 30%, the difference is subjected to a 10% penalty.

Source

Notification of change of accounting period of a company/ limited liability partnership/ trust body/co-operative society http://phl.hasil.gov.my/pdf/pdfam/PR_08_2019.pdf

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#personaltax

#irb

#LHDN

3分钟看完所得税罚款配套 Income Tax Offences Part 1

3分钟看完所得税罚款配套 Income Tax Offences Part 1

-

没有交 “所得税申报表” - RM200.00至RM20,000.00 /监禁不超过6个月/两者

-

纳税人未通知所得税- RM200.00至RM20,000.00 /监禁不超过6个月/两者

-

省略或低估收入来作不正确的所得税申报表- RM1,000.00 至RM10,000.00 / 200%的少收税款

-

提供任何不正确信息 - RM1,000.00 至RM10,000.00 / 200%的少收税款

-

逃避或协助任何他人逃税RM1,000.00 至RM20,000.00 /监禁不超过36个月/两者/300%的少收税款

-

协助其他人低估收入 - RM2,000.00 至RM20,000.00 /监禁不超过36个月/两者

-

尝试不缴税就离开国家 - RM200.00 至RM20,000.00 /监禁不超过6个月/两者

-

阻碍IRBM官员执行其职责 - RM1,000.00至RM10,000.00 /监禁不超过1年/两者

-

未完待续

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#personaltax

#irb

#LHDN

如何修改 CP500?

如何修改 CP500?

CP500是 Notis Bayaran Ansuran, 意思是“分期预付所得税” . CP500表格是对纳税人的税收分期付款计划.

How? 如何?

-

可以使用表格CP502对估计的分期付款税额进行修改.

-

在6月30日之前提交填妥的表格提.

-

可以从IRBM官方门户网站www.hasil.gov.my获得CP502表格

-

click Forms > click Download Forms > select Other Forms

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#personaltax

#irb

#LHDN

#cp500

个人纳税人的税务编号开头将从OG和SG修改成IG

个人纳税人的税务编号开头将从OG和SG修改成IG

个人纳税人的税务编号开头将从OG和SG 修改成IG. 税务编号则会继续保持不变.

从5月18日这项措施将分成2个阶段进行. 第一阶段是5月18日起登记的新纳税人, 第二阶段是现有的纳税人.

这项措施不会对报税的截止日期产生任何影响. 受薪族的报税截止日期是4月30日(hardcopy)和5月15日(E filing). 经商人士的报税截止日期是6月30日(hardcopy)和7月15日 (E filing).

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#personaltax

#irb

#LHDN

Delay on tax refund

Reasons of why fail to receive Tax Refund and the relevant solutions

Do you know the reasons why tax refunds fail to be processed?

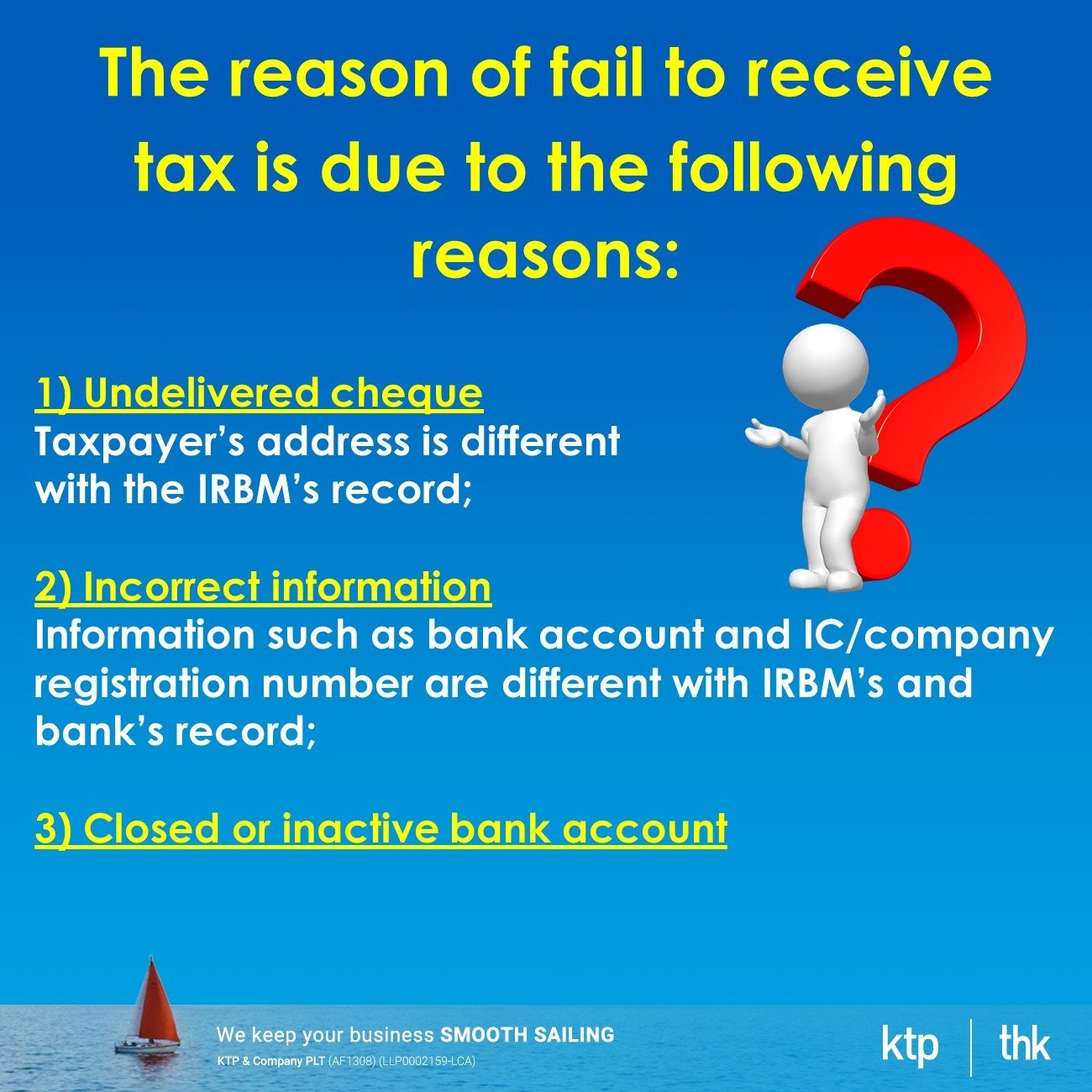

The reason of fail to receive tax is due to the following reasons:

i. Undelivered cheque -taxpayer’s address is different with the IRBM’s record;

ii. Incorrect information - Information such as bank account and IC/company registration no. are different with IRBM’s and bank’s record;

iii. Closed or inactive bank account

How to deal with delay in tax refund?

You are advised to:-

1. update the latest personal/company banking information in the annual Income Tax Return Form (ITRF)

2. update the information through MyTax application

3. write a letter and submit to LHDN branch

4. make an application through https://maklumbalaspelanggan.hasil.gov.my/MaklumBalas/en-US/

Besides, you can also opt to contra the tax refund with the following situation: -

1. Contra with the tax outstanding balance including any raise penalty might be imposed for the Year of Assessment.

2. Contra against with the tax instalment payment such as CP204 or CP204A or CP500 under section 107B and Section 107C of Income Tax Act.

3. Contra against with any tax instalments which before payment due date.

Source: IRB tax refund

http://phl.hasil.gov.my/pdf/pdfam/RANGKA_KERJA_PUNGUTAN_CUKAI_2021.pdf

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#taxrefund

#irb

#LHDN

Acounting standard on revenue

Read the full story in our blog

https://www.ktp.com.my/blog/accounting-for-revenue/11may2021

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏 (𝐀𝐮𝐝𝐢𝐭,𝐓𝐚𝐱, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫

We are one-stop (

How to record "tax borne by employer" in the account wisely?

Continue the full story in our blog

https://www.ktp.com.my/blog/tax-borne-by-employer/10may2021

Source :

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏 (𝐀𝐮𝐝𝐢𝐭,𝐓𝐚𝐱, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫

We are one-stop (

𝐌𝐈𝐃𝐀 - 𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐢𝐚𝐥 𝟒.𝟎 (𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲𝟒𝐖𝐑w

If you are SME manufacturers,

Read the full story

https://www.ktp.com.my/blog/mida-industrial-40/7may2021

𝐕𝐢𝐬𝐢𝐭 𝐮𝐬 :

𝐊𝐓𝐏 (𝐀𝐮𝐝𝐢𝐭,𝐓𝐚𝐱, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐓𝐇𝐊 (𝐒𝐞𝐜𝐫𝐞𝐭𝐚𝐫𝐢𝐚𝐥, 𝐀𝐜𝐜𝐨𝐮𝐧𝐭/𝐏𝐚𝐲𝐫𝐨𝐥𝐥, 𝐀𝐝𝐯𝐢𝐬𝐨𝐫𝐲)

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫

We are one-stop (

MIDA tax incentives on logistic

What is the Government Support for logistics services companies?

The Malaysian Investment Development Authority (MIDA) supports the growth of companies undertaking integrated logistics services (ILS) by offering tax incentives for 5 years as below:

1. Pioneer status (PS)

- Tax exemption of 70% of statutory income.

2. Investment tax allowance (ITA)

- 60% of qualifying capital expenditure*

*Qualifying capital expenditure means capital expenditure incurred on factory or any plant and machinery used in Malaysia in connection with and for the purposes of ILS.

Key takeaways:

You will understand: -

1. What is the integrated logistics services?

2. What are the qualifying criteria for ILS incentive?

3. How to apply?

Integrated logistics services (ILS)

ILS refers to a company that performs a variety of end-to-end logistics-related service activities like air, ocean, road and rail transportation, warehousing and other value-added services that make up a total logistics services package.

Main activities involved:

· Warehousing

· Transportation

· Freight Forwarding

· Distribution

· Other value added services (Example: break bulking, palletising, labelling, etc)

Qualifying criteria

1. Locally incorporated

i. Incorporated under Companies Act 2016 and resident in Malaysia; and

ii. 60% equity held by Malaysian.

2. Eligible services

Must undertakes 3 principal activities:

i. Freight forwarding

ii. Warehousing

iii. Transportation

and at least one of the following activities:

i. Distribution

ii. Supply chain management

iii. Other related and value-added services/activities

- Palletizing, product, assembly/installation, breaking bulk, consolidation, packaging/re-packaging, procurement, quality control, labelling/re-labelling, testing etc.

3. Minimum Infrastructure to be owned by applicant company

i. Commercial vehicles: 20 units

- Motor vehicle for the purpose of carrying goods.

ii. Warehousing facilities: 5,000 sq metres

- To provide various facilities and services covering small dock-off depots to large scale warehouses and distribution centers.

Procedure for application

1. Register an account under https://investmalaysia.mida.gov.my.

2. Submit the application online for MIDA approval.

3. Proceed to apply for tax incentive certificate after get approval from MIDA.

Reference

-

Guidebook of Integrated Logistics Services

-

https://www.mida.gov.my/wp-content/uploads/2020/07/20191220163458_BOOKLET-4-LOGISTICS-SERVICES.pdf

-

Guidelines for application for tax incentives for Integrated Logistics Services (ILS) (31.03.2021)

-

https://www.mida.gov.my/wp-content/uploads/2021/04/GD_ILS_31032021.pdf

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

如果您总是喜欢使用Director account支付费用

所得税 ..如何用这一招 超senang查您的account!

如果

-

您总是喜欢使用Director account支付费用

-

Dr Expense 费用

-

Cr Director account

-

-

您Director account 年末 balance 很高!

Why? 所得税

-

总是会看 Director account. .

-

会问您为什么要使用Director account支付费用 ?

-

将检查您的director 个人税 (personal income tax)

结果

-

根据《所得税法》第S140A条,所得税可以向Director 收取Deemed利息!

-

当您将来注销 (write off) Director account 时… 债务免税 (waiver of debt 可能中税的

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

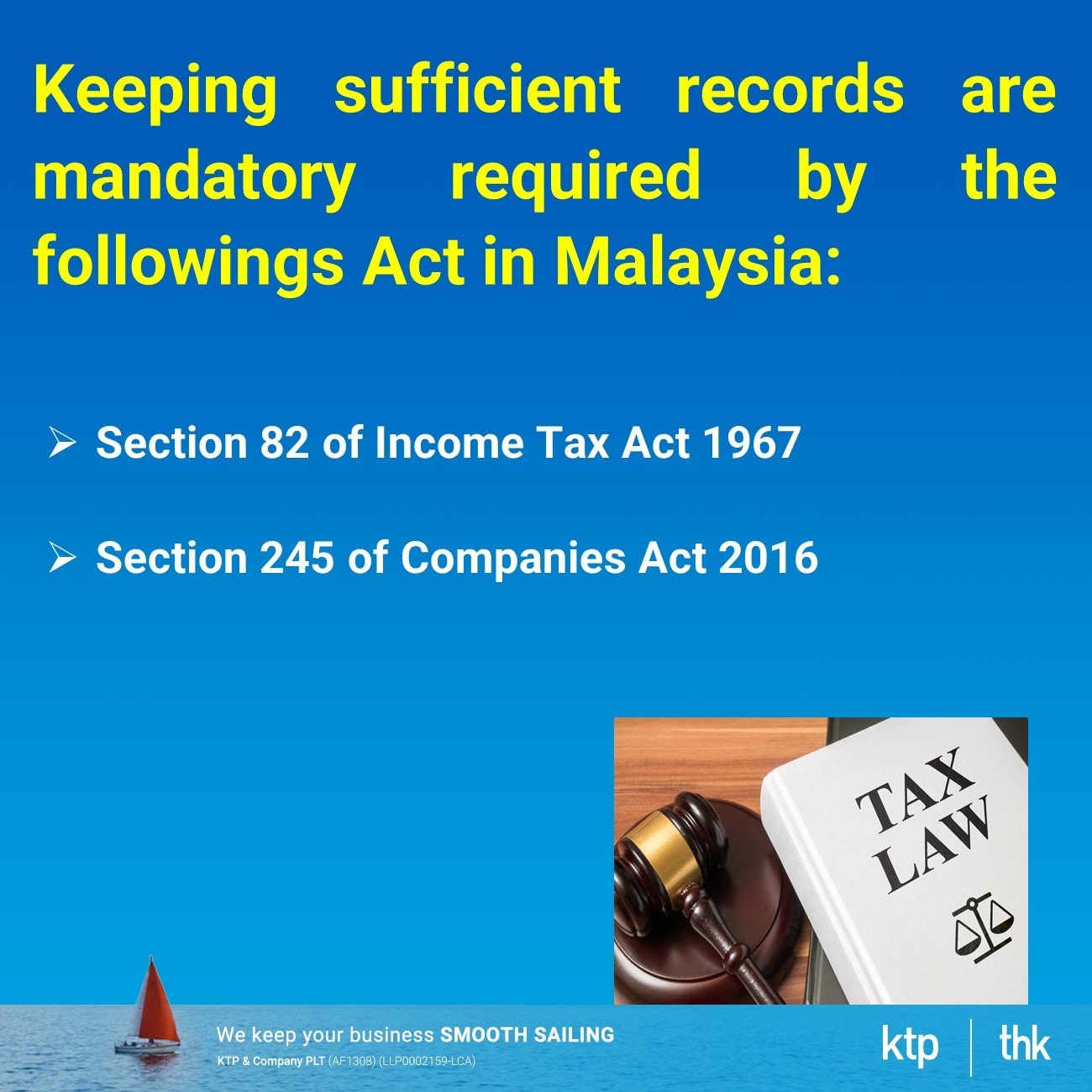

Record keeping 7 years Malaysia

Keeping sufficient records are mandatory required by the followings Act in Malaysia:

1. Section 82 of Income Tax Act 1967

2. Section 245 of Companies Act 2016

What are the records to be kept by company?

1. Accounting records - a cash book, a sales ledger, a purchases ledger and a general ledger

2. Supporting documents - invoices, bank statements, pay-in slips, cheque butts, receipts for payments, payroll records and copies of receipts issued should be retained.

3. Receipts issued should be serially numbered when sales of goods exceed RM150,000 or services performed exceeds RM100,000.

4. A valuation of the stock in trade or work in progress should be made at the end of each accounting period and the appropriate records maintained

5. Other documents necessary to verify entries in any books of accounts

What are the requirement under Income Tax Act 1967 and Companies Act 2016?

1. Accounting entries for each transaction should be recorded not later than 60 days after the transaction.

2. Records and books of accounts should be written in the national language or the English language.

3. The company is required to keep sufficient records for a period of 7 years.

4. All documents that relate to any income in Malaysia shall be kept and retained in Malaysia.

5. If the records and books of accounts are kept outside Malaysia, the records and books of accounts should be produced at the registered office or the business premises of the company.

What are the consequences if sufficient records are not kept?

1. Additional tax payables arise from:

i. The chargeable income of the taxpayer may be determined according to the best judgement of IRB and an assessment made accordingly.

ii. Deduction is not allowed If the taxpayer fails to provide supporting records.

2. The financial statement of the company is not reliable

i. It will affect the auditors’ opinion on financial statement and modified audit opinion will be issued according the effect of misstatement.

ii. A modified audit opinion will limit the company’s ability to borrow money from banker.

iii. The supplier might evaluate company’s creditworthiness through audited financial statement. If the company’s financial statement is not reliable, the supplier may reluctant to give longer credit terms.

3. It is an offence under the laws in Malaysia:

i. Section 119 of Income Tax Act 1967

- A fine of RM300 to RM10,000; or

- to imprisonment for a term not exceeding 12 months or to both.

ii. Section 245 (9) of Companies Act 2016

- A fine not exceeding RM500,000; or

- to imprisonment for a term not exceeding 3 years or to both.

Sources

1. Public Ruling No. 4/2000 (Revised) Keeping sufficient records (Companies & Co-operatives)

2. Public Ruling No. 5/2000 (Revised) Keeping Sufficient Records (Individuals & Partnerships)

3. Public Ruling No. 6/2000 (Revised) Keeping Sufficient Records (Persons other than Companies & Co-operatives)

4. Income Tax Act 1967

5. Companies Act 2016

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Extension/Renovation of factory building is allowed for tax deduction?

Extension/Renovation of factory building is allowed for tax deduction?

What is Industrial Building Allowances (IBA)?

IBA is allowed a person who incurred cost of factory building expenditure for the purpose of his business to claim allowances.

Eligibility to claim:

-

Initial Allowance (IA): 10%

-

Annual Allowance (AA): 3%

How do you know your factory building expenditure incurred is eligible for IBA?

A simple checklist

-

The building carry out manufacturing or processing operation?

-

The expenditure incurred is for production area?

-

The expenditure incurred is for the purpose of building improvement.

If all the question is “Yes”, then the expenditure is eligible for IBA claim

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Do you know IRB refund policy on excess tax payment?

Do you know IRB refund policy on excess tax payment?

-

30 working days after submission date for Return Forms submitted via e-Filing.

-

90 working days after submission date for Return Forms submitted by post or by hand.

Terms & Conditions :

The tax refund is only applicable on correct and complete information is provided in the Return Form.

Sometimes the only thing I can say is “Really”?

But you can

-

Contra against CP204 payment.

-

Wait for 2% compensation on IRB late refund since 2013… So far we have managed 1 case approved since 2013 !

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.