Tax

Agriculture Allowance

Agriculture Allowance

Are agriculture companies entitled to any tax incentives?

Agriculture allowance

A taxpayer who incurred Qualifying Agriculture Expenditure is entitled to claim Agriculture Allowance.

Qualifying Agriculture Expenditure

1. Clearing and preparation of land

2. New planting (exclude replanting) either:

a) new crop of any product

b) replace old crops with a crop of a different type

3. Construction on a farm of a road or bridge

4. Construction on a farm of a building either:

a) used in working of farm

b) welfare of persons

c) living accommodation

5. Schedule of Agriculture Allowance

Non-Qualifying Agriculture Expenditure

1. Cost of land

2. Cost of plant and machinery used in the farm

Agriculture Charges (Disposal)

1. If disposal within 5 years: agriculture charge equal = allowances claimed in prior years

2. If disposal made after 5 years: no agriculture charge will be made

Source

Reference: Public Ruling No. 1/2016 Agriculture Allowance

https://phl.hasil.gov.my/pdf/pdfam/PR_01_2016.pdf

This message was brought to you by KTP

Tax Deduction on Payment to Release Bumi Lot

Tax Deduction on Payment to Release Bumi Lot

Do you know there are 6 deciding case law in high court from 2020 to 2021 on the tax appeal regarding payment to release bumi lot.

Today we cover one recent Court of Appeal case namely DIRECTOR GENERAL OF INLAND REVENUE vs TAMAN EQUINE (M) SDN BHD which overturn High Court decision.

Lesson from Tax Case:

The tax treatment of application expenses incurred to release the Bumiputera quota units by a housing developer.

Background information

Taman Equine (M) Sdn Bhd (The Company) is a housing developer.

The Company has incurred expenses to apply to State Government to release the Bumiputera quota units.

Tax Issue:

Are expenses incurred for the release of the Bumiputera quote units allowable for tax deduction?

The Company’s opinion:

The application of the release the Bumiputera quota units is necessary else the Company would not be able to generate its income. Thus, the expenses incurred for the business expenses under section 33(1) ITA 1967.

IRB argument:

The expenditures in question were not eligible for deduction under Section 33(1) of the ITA for the following reasons:

a) the cost incurred is a penalty in nature and

b) not wholly and exclusively incurred for the purpose of producing the gross income.

The decision by The Court of Appeal

The Company expenses were not allowed for deduction due to the following reason:

a) the nature of the payment is a penalty for breach of a condition imposed by the State Government.

b) it does not form part of the taxpayer’s income-producing activity.

c) the expenses incurred are for the purpose of bringing into existence an advantage in terms of procuring permission/consent from the state authority for the permanent benefit of the business

d) it is capital in nature and prohibited under section 39(1) ITA 1967.

Source:

https://phl.hasil.gov.my/pdf/pdfam/KPHDN_v_TAMAN_EQUINE_17062022.pdf

This message was brought to you by KTP

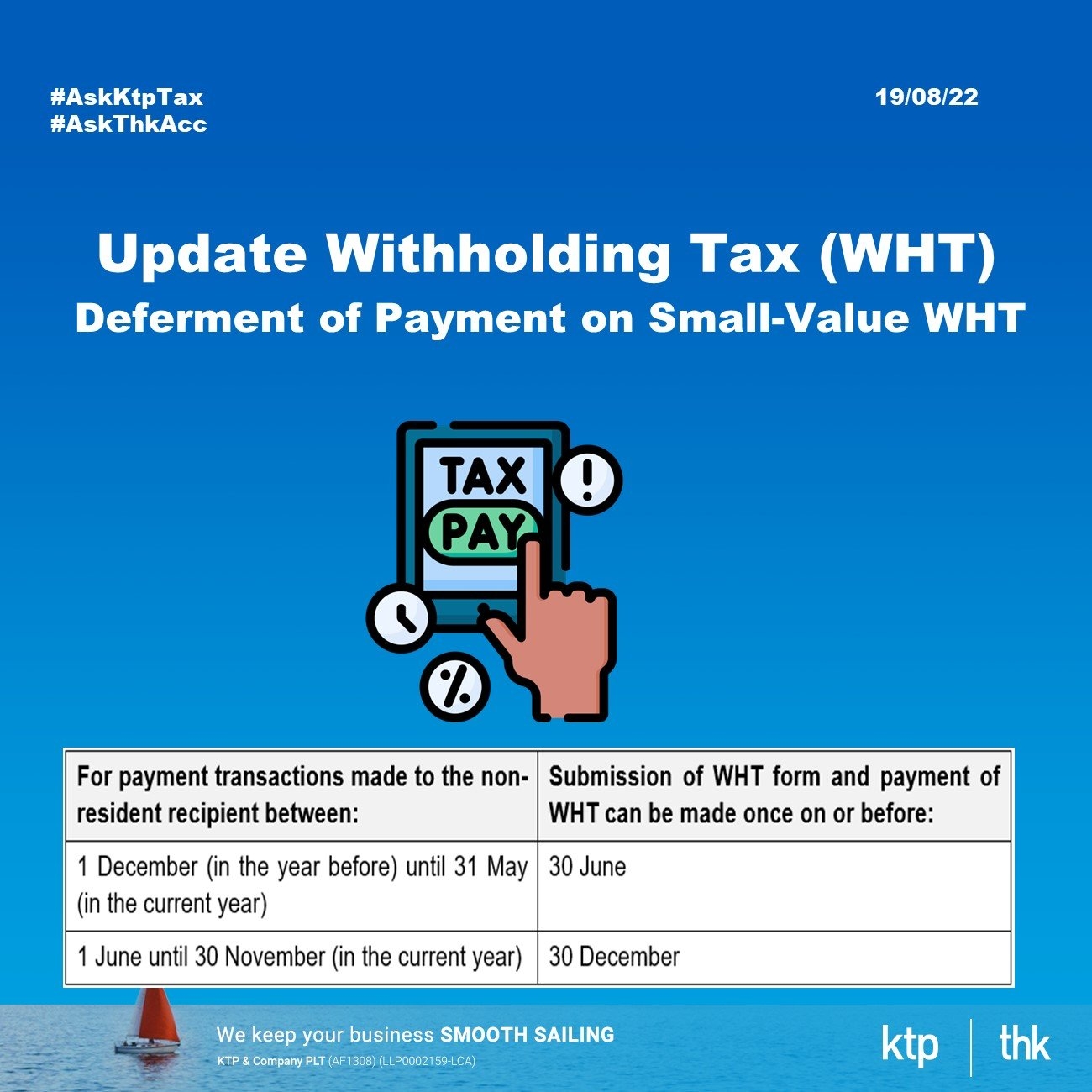

Small Value Withholding Tax Payment

Small Value Withholding Tax Payment

An individual/body resident in Malaysia or doing business in Malaysia that is required to pay WHT under S.109 or S.109B of the Income Tax Act 1967 that do not exceed RM500 per transaction for transactions that recur may submit the WHT form and pay the WHT as follows:

(See above)

-

S.109 = Royalty and Interest earned by non-resident

-

S.109B = Special class of income under Section 4A of the ITA including service and rental of moveable property

Others Operational Issue

The above will take effect from August 2022.

IRBM is in the process of preparing the special WHT forms for the purposes of the above.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

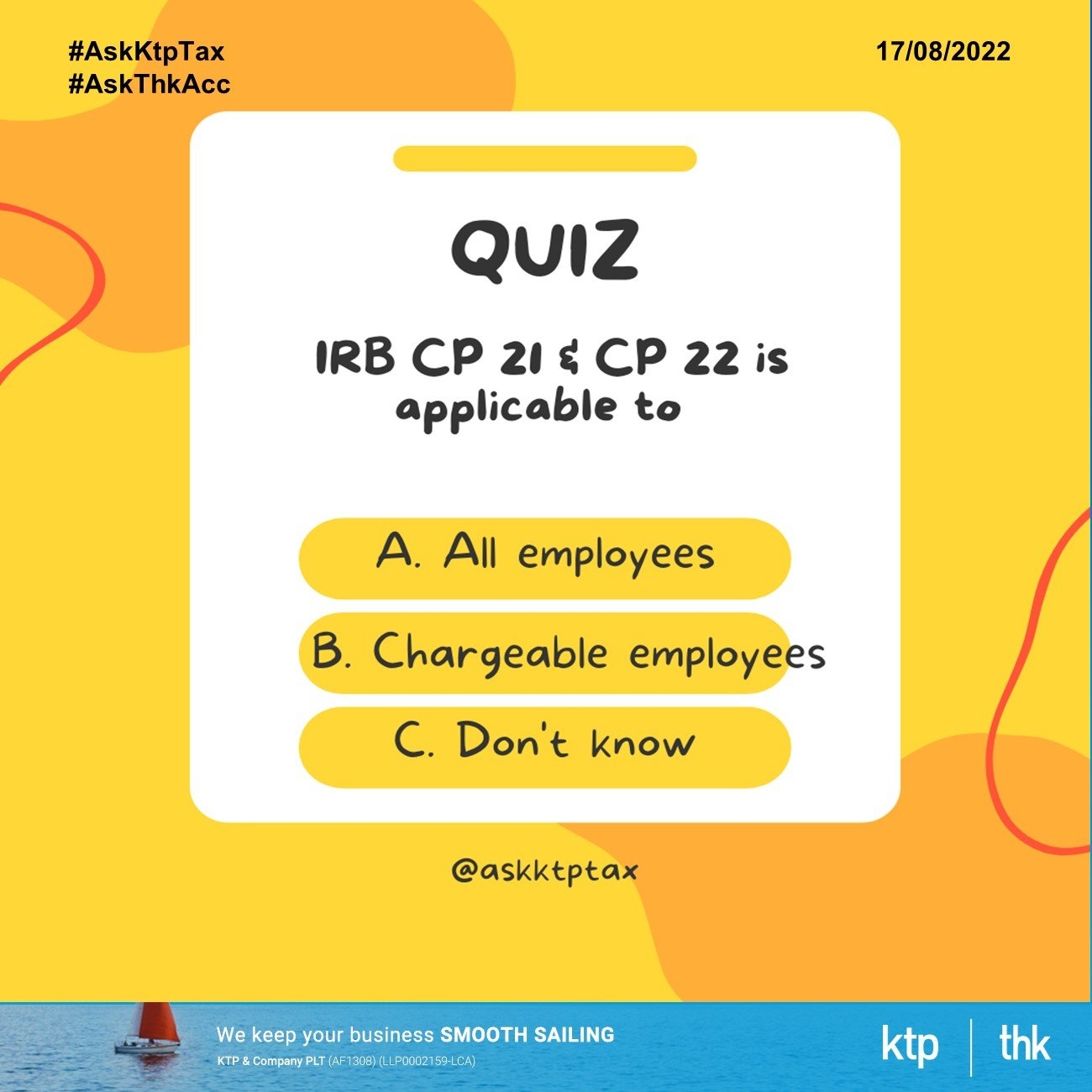

CP 21 Form LHDN

Update CP 21 form

Tax Quiz: IRB CP 21 & CP 22 is applicable to :

A. All employees

B. Chargeable employees

C. Don't know

Read our past social media posting on CP21 & CP 22 as below :

1. Tax Responsibility Employer – dated 14/04/2022

https://bit.ly/3QHAgpL

2. IRB Latest Operasi on CP 21, CP 22 & CP22A – 11/04/2022

https://bit.ly/3dkGbCQ

3. Calling HR/Account dated – 29/12/2021

Do it before 31 December 2021 on your newly recruited & resigned employees in your company as IRBM ...

https://bit.ly/3phhiuy

4. Are you ready for ''payroll'' tax from IRB? dated on 13/10/2021

https://bit.ly/3PoWFr3

5. 为什么所得税发布 2021 年 10 月 1 日 发布雇主审计框架 (Audit Framework for Employers) ? dated 7/10/2021

https://bit.ly/3QAcNHc

6. Beware taxpayers! Dated 23/7/21

https://bit.ly/3Pr4fRX

7. e-SPC via the MyTax link (by employers only) 23/2/21

https://bit.ly/3QrLOOr

8. With effect from 1/1/2021, IRB has changed new forms on 12/1/21

https://bit.ly/3QiNp97

9. 8 out 10 HR don’t do this for IRB (According to our experience) 21/12/20

https://bit.ly/3JVp07c

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

What is the tax treatment for income tax borne by the employer?

What is the tax treatment for income tax borne by the employer?

Perquisite

Perquisite, in relation to employment, means benefits in cash or in kind that are convertible into money received by an employee from the employer or third parties in respect of having or exercising the employment.

What does tax borne by employer mean?

Do employers pay income tax for employees?

No, employers do not pay income taxes for their employees. Employees are solely responsible for income tax payments, which employers must withhold.

What if? There is good employer who pays employee tax?

The agreement by the employer to pay the income tax of the employee does not relieve the employee from tax liability on the amount of income tax borne by the employer.

'Income Tax is borne by employer' is a form of income and is chargeable based on Section 13(1)(a) of the ITA 1967.

In short, tax borne by the employer is a taxable perquisite to the employee.

Source :

-

IRB Public Ruling 11/2016 - Tax Borne by Employer

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

IRB New Public Ruling 2022

IRB New Public Ruling 2022

Public Ruling 2/2022 - Tax Incentive for Organising Conference in Malaysia

This PR is the 1st edition and the objective of this PR is to provide an explanation on the tax incentive available to conference promoter promoting and organising conferences in Malaysia as its main activity and

Public Ruling 3/2022 - Taxation of Foreign Fund Management Company

This PR is the 3rd edition and it replaces the PR No.7/2019dated 3 December 2019 with new updates and amendments.

Source

PR 2/2022 Tax Incentive For Organising Conferences In Malaysia

https://phl.hasil.gov.my/pdf/pdfam/PR_02_2022.pdf

PR 3/2022 Taxation Of Foreign Fund Management Company

https://phl.hasil.gov.my/pdf/pdfam/PR_03_2022.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

What is tax corporate governance framework LHDN?

What is tax corporate governance framework?

A strong tax governance framework establishes the techniques and processes within the organisation to identify tax risks, assess risks and sets out the appropriate actions to mitigate the impact of those tax risks.

Objective of TCGF

The purpose of corporate governance is to facilitate effective, entrepreneurial and prudent management that can deliver the long-term success of the company. Corporate governance is the system by which companies are directed and controlled. Boards of directors are responsible for the governance of their companies.

Background

The Inland Revenue Board (IRB) has launched the Tax Corporate Governance (TCG) Framework during the opening ceremony of the IRB's 26th Hari HASiL celebration and has recently published the TCG Framework and the TCG Guidelines. The introduction of the TCG Framework is part of the IRB’s initiative towards adopting a co-operative tax compliance that is both fair and effective in Malaysia.

Benefits of TCGF

Organisations will be able to enjoy the following benefits upon their participation in the TCG Programme :

I. Reduced scrutinization of compliance activities.

-

Lesser tax audits will be conducted.

-

Higher materiality or reduced sample size.

II. Expedite tax refunds.

Accelerate tax refund process for compliant participants, provided no anomalies are

noted the best endeavour will be given to expedite refunds.

III. Appointment of a dedicated tax officer.

A single point of contact between the taxpayer and the IRBM.

IV. Expedite any ongoing dialogue on technical matters.

-

Priority consideration

-

Eligible to be granted priority consideration for compliant participants, which are:

- Consideration will be given accordingly in respect of tax penalty rates.

- Step down of compliance activities.

TCGF at a glance

TCG is suitable for all sizes and types of businesses that give priorities and resources to corporate governance matters.

TCG Programme is currently being implemented as a pilot project. However, the interested organisations are advised to adopt and execute the framework.

TCG in Malaysia is currently being implemented as a pilot project. Therefore, selected organisation will receive an invitation from IRBM to join the programme.

Other interested organisations may contact IRBM via tcg@hasil.gov.my to communicate their interest.

Once an organisation is accepted into the programme, the TCG status will be valid for 3 years subject to terms and conditions stated in the offer.

There will be no fees charged to participate in the programme.

These expenses are capital in nature and not allowable for tax deduction under subsection 33(1) ITA 1967.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Benefits of Malaysia Digital

MSC Malaysia is now rebranded to Malaysia Digital (MD) Part 3

Benefits of MD

MD Status companies are eligible to access orapply for, amongst others:

1. Foreign knowledge worker quota and passes;

2. Tax incentives (income tax exemption or investment tax

allowance);

3. Multimedia/ICT equipment import duty and sales tax exemption;

4. Competitive and ready infrastructure for business available at

MD Cybercities/Cybercentres;

5. Freedom of ownership by exempting from local ownership

requirements;

6. Flexibility to source capital and funds globally; and/or

7. MDEC as the one-stop agency for MD Status companies.

Other Benefits

MD Status companies are also eligible to access facilitation of other benefits

such as:

1. Access to local and international market and ecosystem;

2. Business matching and partnership;

3. Grant and funding facilitation; and/or

4. Participation in MD catalytic programmes.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

MSC Malaysia is now rebranded to Malaysia Digital (MD) Part 2

MSC Malaysia is now rebranded to Malaysia Digital (MD) Part 2

Eligibility Criteria

To be eligible to apply for the award of MD Status, a company is required to

meet the following criteria:

(a) Incorporated under the Companies Act 2016 and resident in Malaysia; and

(b) Proposing to carry out or is currently carrying out one or more of the

MD activities.

Approved Activities

MD activities are listed as below. The activities, upon approval of MD Status, will be known as “MD Approved Activities”

Research, development and commercialization of solution and/or provision of services in relation to any of the following technologies or areas:

1. big data analytics (BDA);

2. artificial intelligence (AI);

3. financial technology (Fintech);

4. internet of things (IoT);

5. cybersecurity (technology/software/design and support);

6. data centre and cloud;

7. blockchain;

8. creative media technology;

9. sharing economy platform;

10. user interface and user experience (UI/UX);

11. integrated circuit (IC) design and embedded software;

12. 3D printing (technology/software/design and support);

13. robotics (technology/software/design);

14. autonomous technologies;

15. systems/network architecture design and support;

16. global business services or knowledge process outsourcing;

17. virtual, augmented and/or extended reality;

18. drone technology;

19. advance telecommunication technology ; or

20. other emerging technologies deemed significant for the digital ecosystem subject to approval by the Approval Committee.

Conditions

Conditions to be complied within 12 months from date of award of MD Status:

1. Commencement of operation and undertaking of the MD Approved Activities in Malaysia.

2. Minimum 2 full-time employees (comprising knowledge workers) with minimum average monthly base salary of RM5,000.00, employed for the MD Approved Activities.

3. Minimum annual operating expenditure of RM50,000.00 incurred for the MD Approved Activities

4. Paid-up Capital Minimum of RM1,000.00

To be continued…benefits of MD

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

MSC Malaysia is now rebranded to Malaysia Digital (MD)

MSC Malaysia is now rebranded to Malaysia Digital (MD)

This new enhanced initiative serves to accelerate the sustainable growth of Malaysia’s digital economy and create substantial digital economic spill-over through equitable access to digital tools, knowledge, and income opportunities. Malaysia Digital will drive the digital transformation of focus areas that present high growth potential, opportunities and importance.

The Government of Malaysia, through Malaysia Digital Economy Corporation

(MDEC), awards MD Status to eligible companies that participate in and undertake any of the MD activities.

The grant of MD Status entitles eligible companies to a set of incentives, rights and privileges from the Government of Malaysia.

MSC Malaysia

Since its introduction in 1996, MSC Malaysia has catalysed and transformed

Malaysia into a knowledge-based economy. The strategic initiative was created to foster a conducive ecosystem driven by high-end infrastructure development and ICT companies’ catchment within the identified corridors.

MSC Malaysia, driven by the Malaysia Digital Economy Corporation (MDEC) as

the nation’s lead digital economy agency, has contributed immensely towards the growth of the nation’s digital economy.

Since 1996 Malaysia has attracted 2,794 active MSC-status companies.

Transition from MSC to MD

The existing MSC status and benefits would continue to subsist, subject to compliance of existing conditions by the companies, institutes of higher learning or incubators.

MD companies would soon have the flexibility to choose the benefits (with or without tax incentives) with applicable conditions with further details to be announced soon.

The existing companies are not required to reapply, but MD would be implied to existing MSC companies.

What new under MD

-

The bill of guarantees,

-

Non-location-based incentives

-

An expansion of locations for promoted activities.

To be continued…Conditions, status and benefits of MD

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Service Tax on the Goods Delivery Service

The service tax on the Goods Delivery Service

Royal Customs Malaysia Department announced on 30 June 2022 that Service Tax on Delivery Services Providers (including E-Commence Platform) which be effective on 1st July 2022 postpone to a later date.

Background Information

Budget 2022 announced that the scope of service tax be expanded to include goods delivery services regardless of the status of the service providers (licensed or not) but exclude delivery services for food and beverages as well as logistic services.

Source

Royal Custom Malaysia Department Announcement 30/6/2022

https://mysst.customs.gov.my/News#section14

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

LHDN foreign source income

Update taxability of foreign source income

On 31st December 2022, our government has agreed to exempt taxation on foreign source income (FSI) for resident taxpayers to ensure the smooth implementation of the tax initiative, said the Ministry of Finance (MoF).

The tax exemption is effective from Jan 1, 2022 to Dec 31, 2026.

Finally the following orders has been gazetted recently :

-

Income Tax (Exemption) (No. 5) Order 2022 - Exemption of FSI received by resident individuals.

-

Income Tax (Exemption) (No. 6) Order 2022 - Exemption of foreign-sourced dividends received by resident companies, limited liability partnerships (LLPs) and individuals in relation to a partnership business in Malaysia.

Key Salient Points on The Order

-

Exemption period 1/1/2022 to 31/12/2026 for resident individual

-

All sources of income under Section 4 of ICA 1967 for resident individual on FSI received in Malaysia from outside Malaysia.

-

Income arising from outside Malaysia which is bought into Malaysia.

-

FSI except for dividend income that is received in Malaysia from outside Malaysia for companies and LLPs will subject to :

-

Amounts received from 1/1/2022 to 30/6/2022 – 3%

-

Amounts received after 30/6/2022 – prevailing income tax rate

-

Past Blog

Read our past blog posting from FSI :

1. Confusion on the exemption of foreign source income dated on 30/05/2022

https://bit.ly/3yVOooj

2. 马来西亚对海外收入征税政策 dated on 18/03/2022

https://bit.ly/3csapUe

3. Foreign source income taxable in Malaysia 2022 dated on 11/01/2022

https://bit.ly/3KL1NUx

4. (u-turn update) foreign source income budget 2022 dated on 31/12/2021

https://bit.ly/3tXbici

5. FAQ on Special Income Remittance Programme (PKPP) dated on 27/12/2021

https://bit.ly/3CFoNBq

6. Special Income Remittance Programme (PKPP) to Malaysian Residents dated on 8/12/2021

https://bit.ly/35ObF0Z

7. 预算案 2022 dated on 19/11/2021

https://bit.ly/3tYpdPz

8. Budget 2022 - SME edition dated on 18/11/2021

https://bit.ly/3tRcq1i

9. Foreign source income taxable in Malaysia dated on 10/11/2021

https://bit.ly/3w5BG6y

10. Foreign Income Remitted Into Malaysia Taxable 2022 on 2/11/2021

https://bit.ly/3tTfJVI

11. 海外收入汇回大马时将被征税 dated on 2/11/2021

https://bit.ly/3Imb8k9

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

马来西亚 所得税 的 违法行为与刑罚

马来西亚 所得税 的 违法行为与刑罚

-

没有交 “所得税申报表” - RM200.00至RM20,000.00 /监禁不超过6个月/两者

-

纳税人未通知所得税- RM200.00至RM20,000.00 /监禁不超过6个月/两者

-

省略或低估收入来作不正确的所得税申报表- RM1,000.00 至RM10,000.00 / 200%的少收税款

-

提供任何不正确信息 - RM1,000.00 至RM10,000.00 / 200%的少收税款

-

逃避或协助任何他人逃税RM1,000.00 至RM20,000.00 /监禁不超过36个月/两者/300%的少收税款

-

协助其他人低估收入 - RM2,000.00 至RM20,000.00 /监禁不超过36个月/两者

-

尝试不缴税就离开国家 - RM200.00 至RM20,000.00 /监禁不超过6个月/两者

-

阻碍IRBM官员执行其职责 - RM1,000.00至RM10,000.00 /监禁不超过1年/两者

-

无法保留正确的记录和文档 - RM300.00至RM10,000.00 /监禁不超过1年/两者

-

无法遵守IRBM要求提供某些信息的通知 - RM200.00至RM20,000.00 /监禁不超过6个月/两者

-

在3个月内未通知地址更改 - RM200.00至RM20,000.00 /监禁不超过6个月/两者

-

4月30日之后交税 (non business) -10%罚款应纳税额

-

6月30日之后交税 (business)- 10%罚款应纳税额

-

在截止日期的30天后分期付款 - 10%罚款应纳税额

-

实际税款比修订后的税款估算高出30% - 实际税收余额和估计税收的差额的10%

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#personaltax

#irb

#LHDN

amended return form lhdn

Overview

Taxpayers are allowed to make amendment on the information or assessment for the submitted Tax Return Form(TRF) under Section 77B of the Income Tax Act 1967 (ITA 1967) or Section 30B of Petroleum (Income Tax) Act 1967 (PITA 1967) by using the Amended Return Form (ARF).

Key takeaway

You will understand:

-

Rules of submission

-

Terms for submission

-

Rate of increase in tax

-

Method of submission

Summary of learning

Taxpayers are allowed to make amendment when there is:

-

Understate of income / unreported income

-

Expenses over claimed

-

Capital allowances / incentives/ relief over claimed

The amendment limit to once for a year of assessment.

The amendment is disallowed if the Director General of Inland Revenue (DGIR) has made amended assessment for the submitted TRF.

What are the terms for submission ARF?

ARF must be submitted within 6 months from the due date of TRF

A duly completed ARF must state:

-

the amount / additional amount of chargeable income

-

the additional tax payables

-

the amount of tax payable on the tax which has or would have been wrongly repaid;

-

the increased sum ascertained in accordance with subsection 77B (4) of ITA 1967 or subsection 30B(4) of ITA 1967;

-

other contains required by the DGIR.

What is the rate of increase in tax?

The additional tax payable amount in ARF is subject to an increase in tax of 10%.

The formula = the amount of such tax payable or additional tax payable x 10%.

The total tax payable amount must be paid at the same date of ARF is submitted.

What are the methods for submission ARF?

ARF can be submitted in the following ways:

-

Online e-filing (only for corporate taxpayer: Form C)

To visit https://mytax.hasil.gov.my > click e-Filing > click e-Form > choose e-BNT C

-

Manual filing

- download ARF on Lembaga Hasil Dalam Negeri (LHDN) website:

To visit http://www.hasil.gov.my > Forms > Download Forms (in Malay Version) > Handle the completed ARF to LHDN branch

Sources

GPHDN 1/2020: - Procedure on submission of Amended Return Form

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

CP204 Deferment 2022

CP204 Deferment 2022 is Over

The deferment is over. Taxpayers continue CP204 monthly tax payment before 15th every month with effect from July 2022.

KTP have emailed & whatsapped our clients on the tax instalment notification recently. Please check your email/whatsapp otherwise contact KTP on urgent basis.

Background

The Postponement of Estimated Tax Payable (CP204) and Instalment Payment Scheme (CP500) will be given automatically to qualified taxpayers with the status of micro, small and medium enterprises (MSMEs or PMKS) from Jan 1 to June 30, 2022.

6 instalment deferment

The Inland Revenue Board (IRB) informed that qualified taxpayers are based on records or the latest Income Tax Statement Form received by the board.

CP 204 deferment

For CP204 payment, business criteria that qualify for the PMKS status are companies, cooperatives, trust bodies and limited liability partnerships with a paid-up capital of less than RM2.5 million for ordinary shares at the start of the basic period of an assessment year.

In addition, the entity’s gross business income of RM50 million or below for an assessment year.

The postponement of CP204 payment to the taxpayer who fulfils the criteria will be sent via registered email with HASiL (the IRB).

What if taxpayers don’t want the deferment?

Taxpayers want to maintain the current tax instalment scheme.

-

IRB is not required to be notified as qualified taxpayers are allowed to follow the original CP 204 or CP 500.

-

Any tax instalments paid during the deferment period will be treated as payments towards the tax instalments for those respective months and will not be allowed to be carried forward for settlement of tax instalments after the deferment period.

Tax estimation

No changes to existing eligibility to revise tax estimates in the 6th or the 9th month and the special 11th month revision (subject to existing conditions)

CP500 deferment

The IRB informed that the postponement of CP500 payment is allowed automatically to all taxpayers concerned for the 2021 assessment year payment (for the payable date of Jan 1, 2022) and the 2022 assessment year payment (for the payable dates of March 1, 2022 and May 1, 2022).

FAQ on deferment

Frequently asked questions (FAQ) on the postponement could be accessed via the link https://phl.hasil.gov.my/pdf/pdfam/SOALAN_LAZIM_PINDAAN_BAJET_2022_CP204.pdf and the public can contact the HASiL Recovery Call Centre (HRCC) at 03-8751 1000 for further information.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Intercompany Management Fee

Common Tax Mistakes -Intragroup Services on Management Fee

Intragroup Services

Intragroup services are services provided by one or more members of a multinational group for the benefit of the other members within the group. In general, the types of services that members of a multinational group can provide to each other include, but are not limited to, management services, administrative services, technical and support services, purchasing, marketing and distribution services and other commercial services that typically can be provided with regard to the nature of the group's business.

The costs of such services, initially borne by the parent or other service companies within the multinational group, are eventually recovered from other associated persons through intragroup arrangements.

Non Chargeable Intragroup Services

Shareholder activities

Shareholder activity refers to an activity that one group member (usually the parent company) performs solely because of its responsibility as a shareholder due to its ownership interest in one or more members of the group.

Examples of non-chargeable shareholder activities include:

-

Costs pertaining to the juridical structure of the parent company such as meetings of shareholders of the parent company, issuing of shares in the parent company and costs of the supervisory board;

-

Costs relating to the reporting and legal requirements of the parent company such as producing consolidated accounts or other reports for shareholders, filing of prospectuses; and

-

Costs of raising funds for the acquisition of new companies to be held by the parent company (distinct from fund raising on behalf of its existing subsidiaries).

Duplicative services

Duplicative services are services performed by a group member that merely duplicates a service that another group member is already performing in-house, or that is being performed by a third party.

In such instances, any duplicative claim will be automatically disallowed. The ability of a group member to independently perform the service (for instance in terms of qualification, expertise and availability of personnel) shall be taken into account when evaluating the duplication of services performed.

Example 1

A subsidiary has qualified personnel to analyse its capital and operational budget. This analysis is then reviewed by the parent company's financial personnel. The review by the parent company is considered duplicative.

However, there are exceptions in which duplication of services can be charged such as:

-

Special circumstances where duplication is only temporary. For example in implementing a new system, a company may simultaneously continue to operate an existing system for a short period, in order to deal with any unforeseen circumstances that may arise during the initial implementation; or

-

To reduce the risk of a wrong business decision such as by getting a second legal opinion on a particular project

Services that provide incidental/passive association benefits

This refers to services performed by one member of a multinational group, such as a shareholder or coordinating centre, which relates only to specific group members but incidentally provides a benefit to other members of the group.

Incidental benefit may also arise as a consequence of an associated person being part of a larger concern and not because of a service that has actually been provided. Such incidental benefits would not warrant a charge to the incidental recipient because the perceived benefit is so indirect, and remote, that an independent person would not be willing to pay for the activities giving rise to the benefit and therefore should not be considered as intragroup service to the incidental recipient.

Example 2

An enterprise that had obtained a higher credit rating due to it being a member of a multinational group should not be charged for its mere association with the group. However, if the higher credit rating is due to a guarantee provided by another group member, then an intragroup service can be considered to have been rendered

On-call services

An on-call service is where a parent company or a group service centre is on-hand to provide services such as financial, managerial, technical, legal or tax advice to members of the group at any time.

This service is considered non-chargeable under the following circumstances:

-

Service is easily and promptly available even without any standby arrangement;

-

The potential need for such service is remote;

-

Where there is no/negligible benefits derived from the service.

If there are exceptional circumstances which require on- call services to be considered as chargeable services, it must be proven that an independent person in comparable circumstances would incur such charges to ensure availability of the services when the need for them arises

Source : IRBM Chapter VI-Intragroup Services

CHAPTER VI - Intragroup Services | Lembaga Hasil Dalam Negeri Malaysia

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

(Update) 2% Withholding Tax on Commission to Agents

(Update) 2% Withholding Tax on Commission to Agents

Payer:

• Company pays monetary commission to the individual agent, dealer and distributor

• Company remits the withholding tax to IRB w̴i̴t̴h̴i̴n̴ ̴3̴0̴ ̴d̴a̴y̴s̴ ̴f̴r̴o̴m̴ ̴p̴a̴y̴m̴e̴n̴t̴ ̴d̴a̴t̴e̴ by end of following month

Payee:

• Individual resident

• Received more than RM100k of commission whether in monetary or otherwise (such as accrual) from the same company in the calendar year 2021

• Exclude the commission of employees reported in Form E

• Income tax payable can be deducted by withholding tax

Payments of Withholding Tax

The payments must submit

1. Form CP107D — Pin 2/2022 in PDF form and

2. Appendix CP107D(2) in Excel format via email to the payment centres before making the payments.

This email submission is compulsory for payments via payment counters or post.

-

Kuala Lumpur Payment Counter

pbkl-cp107d@hasil.gov.my

-

Kuching Branch

pbkc-cp107d@hasil.gov.my

-

Kota Kinabalu Branch

pbkk-cp107d@hasil.gov.my

Penalty:

• 10% penalty if the payer fails to remit 2% to IRB within 30 days

• Commission is not allowed for tax deduction

Further Reference

Read our past post on withholding tax on commission to agents :

1. (Latest update) Withholding Tax on Payments to Agents dated on 21.04.2022

https://bit.ly/3uFIQNj

2. Withholding Tax on Payments to Agents dated on 17.03.2022

https://bit.ly/3L3JzOB

3. 2% withholding tax on commission dated on 30.12.2021

https://bit.ly/3hRrk20

4. 预算案 2022 dated 19.11.2021

https://bit.ly/3tKU7dM

5. Budget 2022 - SME edition dated on 18.11.2021

https://bit.ly/3IWhAiR

Source

IRBM PEMAKLUMAN PINDAAN PENGOPERASIAN POTONGAN CUKAI 2%

OLEH SYARIKAT PEMBAYAR KEPADA EJEN, PENGEDAR ATAU

PENGAGIH (INDIVIDU PEMASTAUTIN) MULAI JULAI 2022 Dated 9/7/2022

https://bit.ly/3apJqrL

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

unabsorbed business loss carried forward 10 years

How many years can unabsorbed business losses can be carried forward?

Public Ruling 1/2022 - Time limit on unabsorbed adjusted business losses carry forward

IRB has produced the first public ruling of 2022 !

The objective of this Public Ruling (PR) is to provide an explanation on the time limit for unutilised or unabsorbed adjusted business losses arising from a business of a person to be carried forward.

Background

Effective year of assessment 2019, unabsorbed adjusted business losses carried forward for a period of 7 consecutive years of assessment.

But…subsequently.

The time limit for unabsorbed adjusted business losses carried forward arising from a relevant year of assessment change from a 7 consecutive years of assessment to 10 consecutive years of assessment through the Finance Act 2021 [Act 833] effective year of assessment 2019.

Tax Implication

Any balance of unabsorbed adjusted business losses after the

end of the period of 10 consecutive years of assessment is to be disregarded (ie lost).

T & C on Dormant Companies Solely

There has been no substantial change in the company’s shareholding.

By shareholding, Compare the last day of last YA and the first day of next YA on shareholding.

-

More than 50% of the paid-up capital.

-

More than 50% of the nominal value of the allotted shares.

Sections 44(5A) to (5D) – shareholder continuity rules

In a nutshell, where the shareholding of a company was changed substantially during a basis period, any unabsorbed loss and capital allowance brought forward were disregarded – ie were effectively lost forever.

These provisions have been somewhat suspended or deferred as it has been confirmed by the tax authorities that these rules are only applicable in the case of a substantial change of shareholding in dormant companies.

This is further validated via

-

Form C guidebook page 8

-

Post budget technical

-

LHDN dasar dan garis panduan untuk menbenarkan kerugian terkumpul dan elaun modal yang tidak diserap dibawa ke hadapan

https://phl.hasil.gov.my/pdf/pdfam/GP_Membenarkan_kerugianterkumpul.pdf

Source

Public Ruling 1/2022 Time limit on unabsorbed adjusted business losses carry forward

https://phl.hasil.gov.my/pdf/pdfam/PR_01_2022.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Investment Tax Allowance Incentive Malaysia

Tax Incentives For The Manufacturing Sector : Investment Tax Allowance

The major tax incentives for companies investing in the manufacturing sector are the Pioneer Status and the Investment Tax Allowance.

Qualifying Criteria

Eligibility for Pioneer Status and Investment Tax Allowance is based on certain priorities, including the level of value-added, technology used and industrial linkages.

Eligible activities and products are termed as “promoted activities” or “promoted products”. (See Appendix I: List of Promoted Activities and Products – General)

The company must submit its application to MIDA before commencing operation/production.

(i) Investment Tax Allowance

As an alternative to Pioneer Status, a company may apply for Investment Tax Allowance (ITA). A company granted ITA is entitled to an allowance of 60% on its qualifying capital expenditure (factory, plant, machinery or other equipment used for the approved project) incurred within five years from the date the first qualifying capital expenditure is incurred.

The company can offset this allowance against 70% of its statutory income for each year of assessment. The remaining 30% of its statutory income will be taxed at the prevailing company tax rate.

Any unutilised allowance can be carried forward to subsequent years until fully utilised.

Applications should be submitted to MIDA.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Case Study : Tax incentives on the manufacturing of animal feeds from MIDA ?

How to apply tax incentives on the manufacturing of animal feeds from MIDA ?

Tax Incentive Application for Animal Feed Ingredients

Under the Promotion of Investments Act 1986, Small Scale Manufacturing Companies are eligible for the following tax incentives for manufacturing promoted products or activities:

a) Pioneer Status with a full tax exemption for 5 years, or

b) Investment Tax Allowance can be offset against 100% of statutory income for 5 years of assessments.

Besides, the Company needs to full fill the SME definition as follows to apply this tax incentive:

a) Companies with shareholders’ funds of up to RM500,000 with at least 60% Malaysian equity

b) Companies with shareholders’ funds of above RM500,000 and not exceeding RM2.5 million with 100% Malaysian equity.

Scenario

XYZ Sdn Bhd (Name changed to protect the privacy of the Company) is a new transfer client to the KTP Group of Companies. During the discussion with directors, we understand that the Company has the intention to manufacture animal feed supplements. The supplements will help the cows to produce more milk.

Thus, we have studied and identified the tax incentive for this business nature. Manufacturing animal feed is one of the promoted activities listed under Small Scale Manufacturing Companies (Appendix III).

Struggles

Firstly, we have contacted the MIDA officer to confirm manufacturing of animal supplements is fall under animal feed ingredients.

Following that we have arranged a virtual meeting with the MIDA officer and the Company directors. Prior to the meeting, the MIDA officer asks for some details as follows for an initial discussion with the client.

The information required such as:

a) shareholders fund and

b) employment,

c) project cost,

d) raw materials and

e) process flow chart.

Solution

After providing the details, the officer has further studied in detail and guided us on the application of the tax incentive to the next steps.

Source:

http://www.ctim.org.my/file/news/15/00141_Tax%20Incentive%20for%20Small%20Scale%20Manufacturing%20Companies.pdf

https://www.mida.gov.my/wp-content/uploads/2020/12/20200425151042_Appendix20III20Small20Company.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks