Tax

Should I declare rental income in Malaysia

What happen if you don’t declare rental income?

Omission of Rental Income

Any person who makes an incorrect return by omitting or understating any income.

Penalty

S113(1)(a) of the Income Tax Act

Make an incorrect return by omitting or understating any income

RM1,000 to RM10,000 and 200% of tax undercharged

S113(1)(b) of the Income Tax Act

Give any incorrect information affecting the tax liability

RM1,000 to RM10,000 and 200% of tax undercharged

S114 of the Income Tax Act

Wilfully and intent to evade or assist any other person to evade tax

RM1,000 to RM20,000 or imprisonment not exceeding 3 years and 200% of tax undercharged

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

The exemption of foreign source income - what next

Confusion on the exemption of foreign source income

On 31st December 2022, our government has agreed to exempt taxation on foreign source income (FSI) for resident taxpayers to ensure the smooth implementation of the tax initiative, said the Ministry of Finance (MoF).

The tax exemption is effective from Jan 1, 2022 to Dec 31, 2026.

Subject to Inland Revenue Board criteria and guidelines, income tax exemption on dividends will be given to companies or limited liability partnerships while individuals will be tax-exempted for all types of income.

Exclusion on the exemption

The exemption on foreign source income does not apply to company that receives income from renting properties overseas, interest income and royalty income.

These incomes will be subjected to Malaysia tax upon remittance into Malaysia.

Double Tax Relief

Relief from double taxation can be provided under two ways namely exemption method and tax credit method. Under the exemption method, specific income is taxed in one of the two countries and exempted in another country.

If the Malaysian company suffered tax on the rental/interest/royalty income which is remitted into Malaysia, a taxpayer can claim double tax relief under Section 132 or single tax relief under Section 133.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Changes of Form C Year Assessment 2022

(Update) Changes of Form C Year Assessment 2022

1. Income from the source of business(es) and partnership(s) outside Malaysia received in Malaysia effective from 01.07.2022 – Item A2, A7, A20

Aggregate statutory income from sources of business(es) and partnership(s) outside Malaysia received in Malaysia effective from 01.07.2022

Effective from 1 January 2022, the exemption given to Malaysian residents on income from sources outside Malaysia received in Malaysia under paragraph 28, Schedule 6, ITA 1967 has been withdrawn. Income from sources outside Malaysia which is remitted to Malaysia by a resident whether active or passive other than from sources arising from operations carried on in Malaysia, is subject to income tax.

Special guidelines related to tax treatment for income from sources outside Malaysia received in Malaysia will be published on the IRBM Official Portal.

This item must be filled in by a resident company that remits business and/or partnership income from sources outside Malaysia to Malaysia effective from 1 July 2022.

2. Apportionment of Chargeable – Item B2a – B2g

Cukai Makmur – 33% - Companies with taxable income exceeding RM100 million for the basis period for the year of assessment 2022 other than companies subject to the tax rate under paragraph 2A of Part I of Schedule 1.

3. Particulars of Schedule 7A allowance – Item C3 & C4

The company is eligible to claim RA PENJANA and extension of RA PENJANA if it incurred an eligible expenditure during the Year of Assessment 2020 to 2024 in accordance with the provisions of paragraphs 2B and 4C of Schedule 7A of ITA 1967.

Eligible expenditure incurred in the Year of Assessment 2019 (if any) is not entitled for RA in Year of Assessment 2019.

Nevertheless, a separate calculation needs to be made between the RA PENJANA and the ordinary / extension of RA ending in the Year of Assessment 2018. The calculation of the seven (7) year restriction of unabsorbed RA PENJANA will commence in the Year of Assessment 2025 and will end in the Year of Assessment 2031. Balance of unabsorbed RA PENJANA will be disregarded from the Year of Assessment 2032.

4. CLAIM FOR LOSSES – Part E

From 7 consecutive years to 10 consecutive years.

With effect from the Year of Assessment 2019, unabsorbed current year losses are only allowed for carrying forward to be absorbed for a maximum period of up to ten (10) consecutive years [Subsection 44(5F)].

5. Carries out controlled transactions under sections 139 and 140A – Item F8

More information need to fill in

6. Made payments in the basis period which are subject to withholding tax under sections 107A, 107D, 109, 109A, 109B, 109E, 109F and 109G – Item G2

Tax deduction of 2% under section 107D - Payments made in cash by the paying company to appointed agents, dealers or distributors who are resident individuals.

Withholding tax rate:

Tax deductions at a rate of 2% is applicable for payment made in the form of cash to agents, distributors or distributors in the current year.

Such tax deduction is only applicable if the total amount of payment, whether in cash or non-cash, made by the paying company to the agents, dealers or distributors in the previous year exceeds RM100,000.

7. Carry on e-Commerce – Item G4a

A company is considered to be engaged in e-commerce business if the business operations are included in the e-commerce business model as in the table below.

This business model is a general guide for taxpayers.

For more information, please refer to the Guidelines on Taxation of Electronic Commerce Transactions dated 13th May 2019

guidelines_e_commerce_13052019.pdf (hasil.gov.my)

8. Website / social media address – Item G4b

Previously mention “Website/blog address (if any). Now change to “address of the website / social media that is used to conduct the business (if any)”.

9. Particulars of auditors – Item Part H

Income tax no. of the firm - Income tax number of the audit firm as registered with IRBM.

10. Particulars of the Tax Agent and signature of the person who completes this return form.

Income tax no. of the firm - Income tax number of the tax agent’s firm as registered with IRBM..

11. Declaration - Amendments in the declaration

If this return form is prepared based on the liquidator’s account in accordance with the requirements under the Companies Act 2016 (If item 6 = 3), fill in ‘3’ in the relevant box.

Tax Information Collection Program Malaysia

IRBM Information Collection Program

Overview

Do you know that LHDNM has a program called Information Collection Program?

This program is to collect the data of multiple sources of income, purchases, and ownership of assets, association/club memberships, and others.

Therefore, if you have received the notice/letter under Section 81 of the Income Tax Act 1967, it is compulsory to submit the information to LHDNM within 30 days from the date of the notice/letter.

Key takeaways:

You will understand the objective and consequence as follows: --

1. What is the objective of the program?

2. Who is required to submit the information?

3. What types of information are to be provided?

4. When is the deadline for submission?

5. What are the consequences of non-compliance?

Summary of learning

1. What is the objective of the program?

- To provide the information for tax base expansion and support the enforcement and compliance activities conducted by LHDNM.

2. Who is required to submit the information?

- Government agencies, private companies and individuals.

3. What types of information are to be provided?

- Information on payment to insurance agents/distributors/wholesalers/broker, part-time authors/ stringers/ instructors and etc

- License or rental payment made for liquor business, day/night market, tenants/ owners of retail space/lots and etc

- Petrol stations business: total sales and supply of fuel in quantity (in Litre) and value (in RM).

- Buyer information on acquiring services such as vacation packages, luxury vehicle rental, spa and beautician services and others.

- Information of members of associations and organizations

- Information on real-estate assets owners

- Information on the owner of new buildings/homes (residential or shop houses, office buildings or etc)

- Buyer information on acquiring cars or vehicles

4. When is the deadline for submission?

- 30 days from the date of the notice.

- If a longer time is needed, an application to extend the submission time can be made to the relevant LHDNM Branch.

5. What are the consequences of non-compliance?

- A RM200.00 – RM20,000.00 fine or imprisonment for a term not exceeding six months of both.

Sources

Information Collection Program - https://bit.ly/3sO7xX1

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

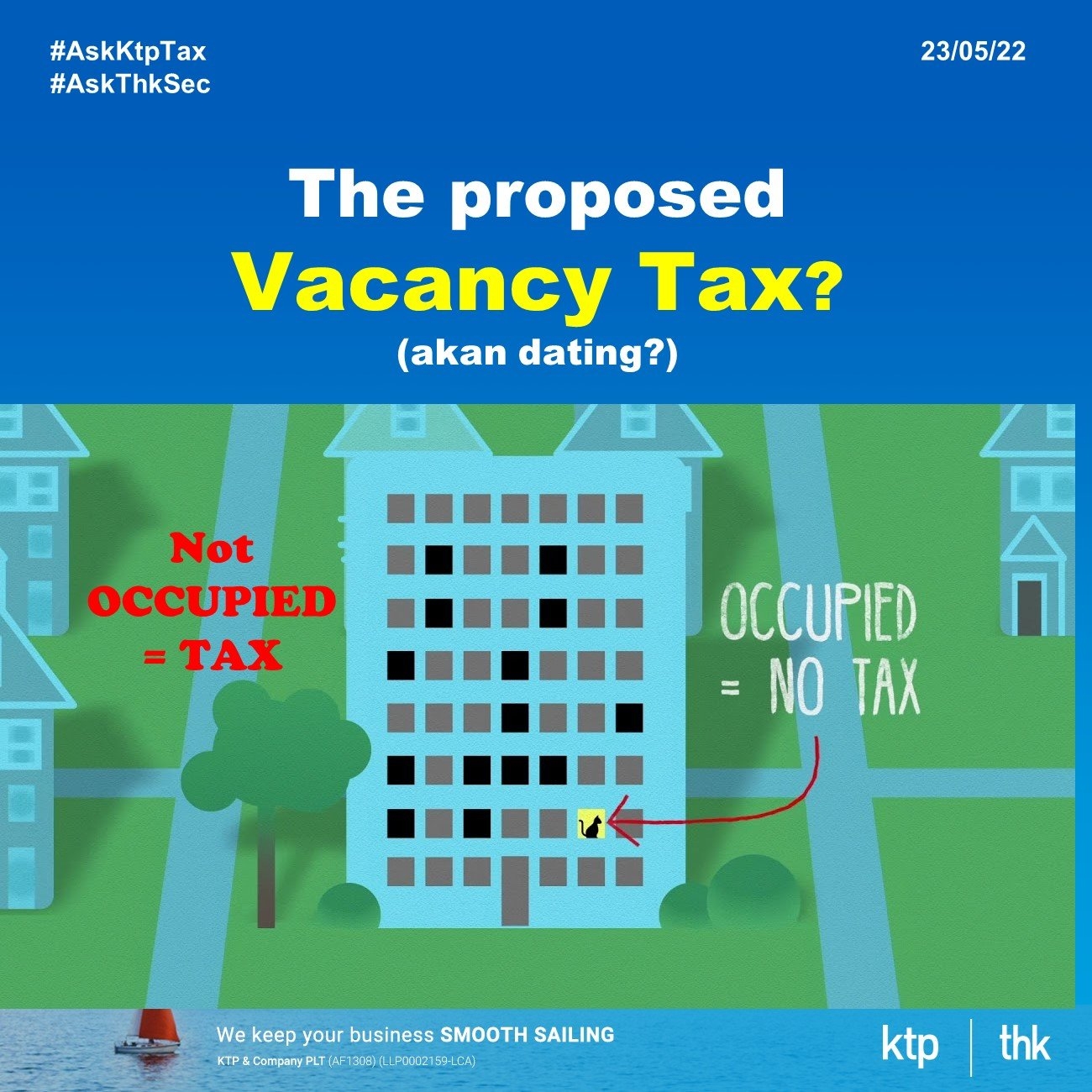

A vacancy tax on unsold properties Malaysia ?

What is the ''proposed'' vacancy tax Malaysia ?

A vacancy tax is a tax levied on properties that have been left vacant and unused for a period of time.

Its objective is to deter speculators and developers from “hoarding properties” with the aim of making a profit when the price rises.

A vacancy tax is to resolve high unsold units in the market

Proposed Mechamism

A vacancy tax could be levied as a percentage of the gross selling price of the unit?

The proposed tax is applicable to properties above RM500,000 selling price.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

What is the minimum tax penalty under the revised tax audit framework?

What is the minimum tax penalty under the revised tax audit framework?

What Is Tax Audit Framework

The tax audit frameworks are to ensure that tax audits are carried out fairly, transparently, and impartially. appeals, etc.

The frameworks outline the rights and responsibilities of audit officers, taxpayers, and tax agents.

This includes sections on the objectives of a tax audit, the selection of cases, the tax audit implementation, offenses and penalties, complaints and appeals, etc

Revised Offences and Penalty

The main changes in the latest tax audit frameworks are in regard to the section on offenses and penalties.

Under the previous frameworks, an initial penalty of 45% applied, with an increase to 55% for repeated offenses.

The penalty is revised and reduced as follows:

-

15% for the first offense;

-

30% for the second offense; and

-

45% for the third and subsequent offenses.

Guideline on offenses

The determination of the tax penalty rate for the first offence or the second offence is referred to the taxpayer’s record on the penalty which has been imposed under subsection 113(2) of the ITA from 1 January 2020 to 30 April 2022.

If the taxpayer has not been penalised under subsection 113(2) of the ITA during the period from 1 January 2020 to 30 April 2022, any audit findings from 1 May 2022 involving the imposition of penalties under subsection 113(2) of the ITA shall be considered the first offence (15%).

If the taxpayer has been penalised under subsection 113(2) ITA during the period from 1 January 2020 to 30 April 2022, any audit findings from 1 May 2022 involving the imposition of penalties under subsection 113(2) of the ITA shall be considered the second offence (30%).

Technical Adjustment

No penalty will be imposed under subsection 113(2) of the ITA for any underpaid or omission of income in respect of the audit findings involving technical adjustments.

Technical adjustments refer to cases which involve different interpretations of the legislation, according to the facts and issues of the particular case.

It does not apply to cases where public rulings, guidelines, practice notes, income tax regulations, income tax exemption orders or income tax rules have been issued by the IRB.

Fraud

If a taxpayer intentionally makes an incorrect return, the penalty to be imposed under Section 113(2) of the ITA will be at the rate of 100%.

Voluntary Disclosure

The penalty rate under Section 113(2) of the ITA for voluntary disclosures is 15%.

However, in cases where a taxpayer has made a voluntary disclosure, and subsequently makes an additional voluntary disclosure within six months from the due date of the submission of the return form, the penalty rate for the additional voluntary disclosure will be 10%

Others

Audit Meja (Desa Audit) renamed to Semakan Umum

Audit Luar (Field Audit) renamed to Semakan Seluruh

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

How to apply International Integrated logistics service (IILS) from MIDA

How to apply International Integrated logistics service (IILS) from MIDA

What is an International Integrated logistics service (IILS)?

In Malaysia, the company must obtain an International Integrated Logistics Services (IILS) status from MIDA (Malaysian Investment Development Authorities) before acquiring the Freight Forwarding Agents/Customs Agent Licence from the Royal Malaysian Customs Department (RMCD).

The IILS status company is required to be involved in the following activities:

• Warehousing

• Transportation

• Freight Forwarding

• Distribution

• Other value-added services (Example: break bulking, palletising, labelling, etc)

And to fulfil the following criteria:

• Owned 20 units of commercial vehicles and 5,000m2 warehouse space;

• Employ majority of Malaysians;

• Use Malaysia as a hub for logistics supply chain services;

• Substantial usage of ICT infrastructure

Client’s Challenges

ABC Sdn Bhd is an existing logistic service provider. The company is planning to expand its business by providing freight forwarding services.

However, ABC Sdn Bhd has no ideas on how to get the Freight Forwarding Agent licence from the RMCD. The company is also not familiar with the procedure to obtain IILS status from MIDA.

How KTP help our client?

KTP conducted a meeting with the company’s directors. After understanding the business plan from the directors, we advised the company to apply for the IILS status with MIDA.

KTP advised and assisted the company throughout the application:

• To ensure the criteria are fulfilled by the company

• To advise the information or documents required for the application

• To assist the company in forecasting the revenue and costs

• To ensure the completeness of the information and documents required before submitting the form

• To liaise with the MIDA officer on the issues raised from the application.

Impacts

The company successfully obtained IILS status from MIDA. The company is eligible to proceed with the application for Freight Forwarding Agents/Customs Agent Licence from the RMCD.

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

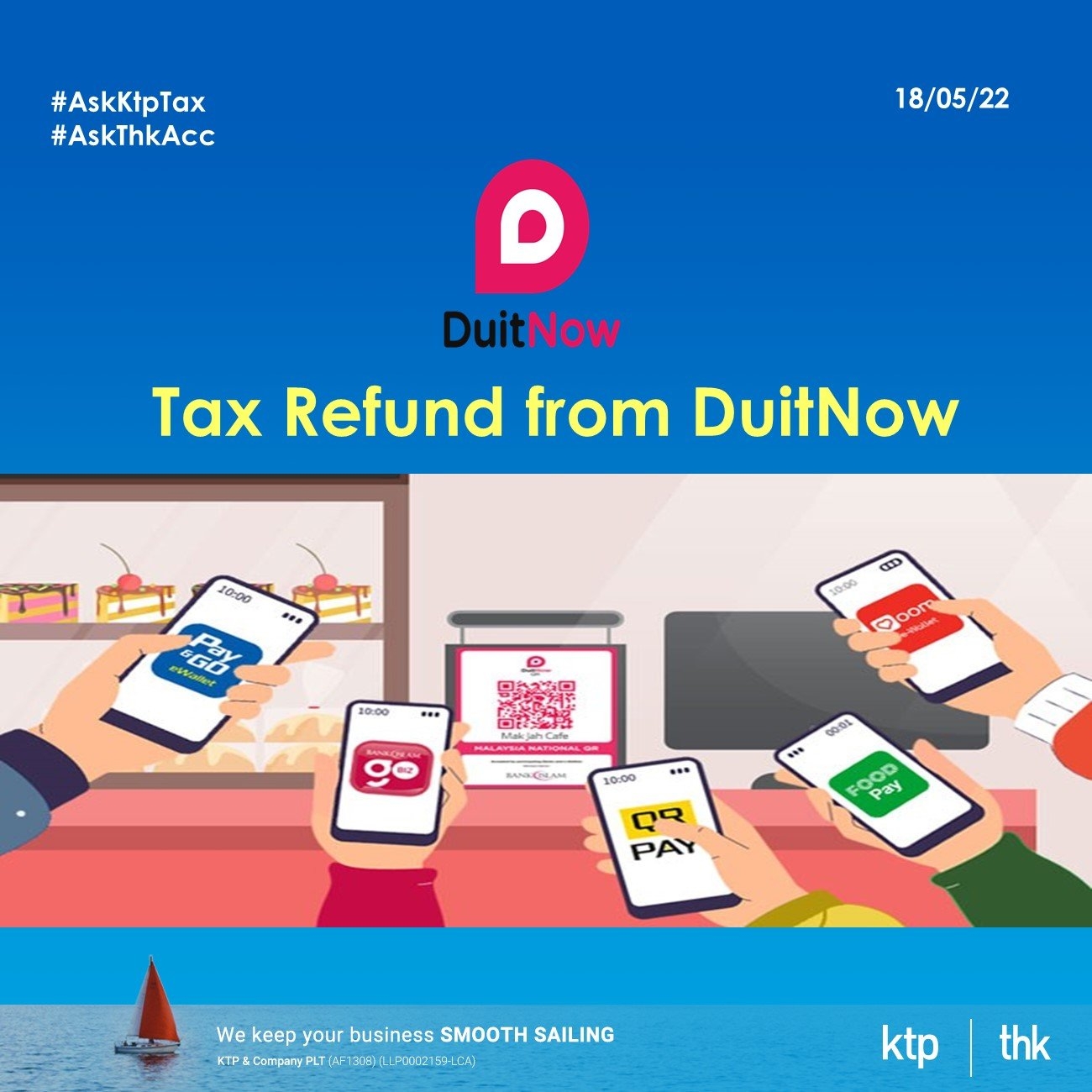

DuitNow Tax REfund

DuitNow Tax Refund

DuitNow is now a refund option for taxpayers without having to provide their bank account details to IRBM.

i. What is the additional channel for a tax refund?

With effect from 1 March 2022, Inland Revenue Board Malaysia (IRBM) allows individual taxpayers to choose to receive their tax refund via Duitnow,

It is applicable to those who have submitted their Income Tax Return Form for the YA2021.

ii. What is DuitNow?

- DuitNow is a latest inter-bank money transfer method.

- It uses only MyKad Number or Passport Number as an ID

iii. Why DuitNow?

- Easy and safe

- Real-time transfer

- No transaction limits

iv. How to Use DuitNow for Tax Refund?

• To register DuitNow with the respective banks by using MyKad Number or Passport Number as Identity Number.

• However, DuitNow registration using a mobile phone number will not be accepted by IRBM for tax refund purposes

• The taxpayer is required to choose this method during the e-filing submission or manual submission of their income tax return form.

• Taxpayers are not required to provide their bank account details.

• If the tax refund made via DuitNow fails, the refund will automatically be made via Electronic Fund Transfer by using the taxpayer’s bank account number and name that is registered with the IRBM.

Source:

DUITNOW AS A MEDIUM FOR TAX REFUND

HASiL_MR_28_March_2022_LAUNCHING_OF_DUITNOW_AS_A_MEDIUM_FOR_TAX_REFUND.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Double deduction for scholarships provided by companies

Why Companies Should Pay for Employees to Further Their Study

Overview:

On 7 March 2022, the Malaysian government gazette the “Income Tax (Deduction for the Sponsorship of Scholarship to Malaysian Student Pursuing Studies at Technical and Vocational Certificate, Diploma, Bachelor’s Degree, Master’s Degree or Doctor of Philosophy Levels) Rules 2022 (P.U.(A) 49/2022).

The rules, which encourage talent development in Malaysia will allow the company to claim the double deduction for any qualifying expenditure incurred.

Key takeaways:

1) Who is eligible for the deduction?

2) Who is the “student”?

3) What is a qualifying expenditure?

4) Qualified Course provider

Summary of learnings:

1. Who is eligible for the deduction?

The company: -

- Which incorporated under Company Act 2016 and resident in Malaysia; and

- Which sponsors a scholarship to a “qualified student” pursuing a full-time course of study: and

- Which executes a scholarship agreement with a student on or after 1 January 2022 but not later than 31 December 2025.

2) Who is the “student”?

A student means an individual: -

- Who is a Malaysian citizen and resident in Malaysia;

- Who has no means of his own

- Whose parents or guardians’ monthly income does not exceed RM10,000.

- Who pursuing a full-time course of study

3) What is qualifying expenditure

Qualifying expenditures are: -

- payment required by relating to the course of study

- educational aid and reasonable cost of living expenses throughout the student’s period of study

4) Qualified Course provider

The course provider must be recognized by the

- Malaysian Qualification Agency or Skills Development Department; or

- Universities and Universities College Act 1971, University Technology MARA Act 1976 or the Private Higher Education Institutions Act 1996

Sources & Relevant Links:

-Income tax deduction for the sponsorship of scholarship rules 2022 (P.U.(A) 49)

https://lom.agc.gov.my/ilims/upload/portal/akta/outputp/1718318/PUA49.pdf

-Malaysian Qualifications Agency

https://www.mqa.gov.my/pv4/index.cfm

- Universities and University Colleges Act 1971

https://www.utm.my/legal/files/2020/08/AUKU-PINDAAN-2019-BM.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Special Tax Deduction Rental Reduction

Special Tax Deduction Rental Reduction IRBM FAQ (Revised 22 March 2022)

Key salient points on the revised FAQ :

1. Deduction for rental reduction period has extended to:

SME: from April 2020 extend to Jun 2022 (P.U.(A) 479/2021) (Previously is until December 2021)

Non-SME: January 2021 extend to Jun 2022 (P.U.(A) 480/2021) (Previously is until December 2021)

2. Eligible person for deduction has extended to include Micro, previously only for Small and Medium Enterprise (SME)

3. SME Certificate issued by SME Corporation Malaysia from Apr 2020 to Dec 2020 can be used as verification of the SME status for rental reduction until 30.06.2022.

4. The supporting document needs to be kept as follows:

-

Stamped tenancy agreement (new/renewal)

-

Statement of rental income

-

Certificate issued by the SME Corp. Malaysia for SME

(only for the rental period: April 2020 – December 2020 need the certificate for verification)

-

Need to furnish the Worksheet

HK-C16B – Sdn Bhd, LLP and business trust

HK-4E – Other than Sdn Bhd, cooperatives, LLP, and business trust

Read our past Facebook postings on the special tax deduction on rental reduction :

1. Great News to Landlords! The special deduction on rental reduction with at least 30% to Small and Medium Enterprise (SMEs) and Non-Small and Medium Enterprise (Non-SMEs) has been gazette on 02 September 2021 (Publication date on 08 September 2021). dated on 23.09.2021

https://www.facebook.com/www.ktp.com.my/posts/6183426361699606

2. 中小企业租金特别扣除 dated on on 15.01.2021

https://www.facebook.com/www.ktp.com.my/posts/4948113128564275

3. 没有宪报的命令 (gazette order ) @ 29/11/20, 这些税收优惠只能视为 ''真的假不了,假的真不了''. dated on 30.11.2020

https://www.facebook.com/www.ktp.com.my/posts/4752532264789030

4. We, as approved tax agent, cannot claim these two tax incentives namely dated on 30.11.2020

https://www.facebook.com/www.ktp.com.my/posts/4752610054781251

5. 我的店主和我拿SME Status Certificate!! dated on 3.7.2020

https://www.facebook.com/www.ktp.com.my/posts/4046044398771157

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Is director’s medical expense tax-deductible in Malaysia?

Is director’s medical expense tax-deductible in Malaysia?

In general, medical fee for the employee is tax-deductible under S 33 of the Income Tax Act 1967.

However …

Public Ruling No. 11/2019 - Benefits In Kinds.

Under section 13(1) b Income Tax 1967, medical and dental benefits are exempted from income tax for employees

Under paragraph 8.3.1 , if the employee receiving BIK from the employer has control over his employer (company) there is no exemption on the medical fee on the director in control company.

What is control?

For a company, the power of an employee to control is through :

-

The holding of shares or

-

The possession of voting power in or

-

By virtue of powers conferred by the articles of association or another document.

Question on tax deductibility

So what is your tax position on director’s medical fee (allowable vs not-allowable expenditure) in Sdn Bhd (controlled company)?

-

If the medical fee on the director is BIK and PCB is deducted accordingly on the director’s remuneration. Or

-

If medical fee is DEEMED as tax exempted BIK !

What is your tax position on this taxing issue?

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Applicability Of Section 140 Of The ITA 1967 on Transfer Pricing Adjustment

Applicability Of Section 140 Of The ITA 1967 on Transfer Pricing Adjustment

SECTION 140 – POWER TO DISREGARD CERTAIN TRANSACTIONS

Section 140 of the Act provides wide and general powers to the Director

General of the Inland Revenue (DGIR) to combat tax avoidance by disregarding certain transactions and computing or re-computing tax liability of a taxpayer.

Where the DGIR has reason to believe that any transaction produces the effect

of:

• altering the incidence of tax

• relieving from a tax liability

• evading or avoiding tax, or

• hindering or preventing the operation of the Act

he may disregard or vary such a transaction to counteract its intended effect.

In particular, DGIR may invoke Section 140 in respect of transactions between:

• related parties – ie persons, one of whom has control over the other or both are under common control, or

• individuals who are relatives (parent, child, sibling, uncle, aunt, nephew,

niece, cousin, grandparent, grandchild)

on the grounds that such transactions are not on par with transactions

between independent parties dealing at arm’s length.

Transfer pricing adjustment

Whilst the Revenue is empowered to counteract any tax avoidance scheme via Section 140(1) of the ITA, this provision does not extend to transfer pricing adjustments.

We examine a recent decision by the Special Commissioner of Income Tax in OMSB v KPHDN where the Revenue’s transfer pricing adjustments were set aside.

RDS analysis on OMSB v KPHDN

Read the full story on the RDS blog on “Transfer Pricing Adjustments: Applicability Of Section 140 Of The ITA”

https://www.rdslawpartners.com/post/transfer-pricing-adjustments-applicability-of-section-140-of-the-ita

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsourcing bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancies in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

How to amend tax return after filing under S 131 of the Income Tax Act 1967

How to amend tax return after filing under S 131 of the Income Tax Act 1967

Overview

Inland Revenue Board (IRB) allows taxpayers to file an Amended Return Form (ARF) if taxpayers need to fix an error or mistake and result in under-payment of taxes.

However, how about if the taxpayer has overpaid the taxes because forgot to claim a tax credit or deduction in Income Tax Return Form (ITRF)? Don't worry, the taxpayer can make an application for relief under Section 131 and 131A of the Income Tax Act 1967 (ITA).

Let's see the conditions and procedure to be satisfied with the application.

Key takeaway:

You will understand:

1. What is considered an error or mistake in ITRF?

2. What are the time frames for the application?

3. What are the conditions for application?

4. How to apply for relief?

Summary of learning:

What is considered an error or mistake in ITRF?

The taxpayer had paid excessive tax because of the following reason:

- Error or omission to deduct an allowable expense

- Arithmetical error

- Misleading of laws

- Income for the previous YA is reported in current YA

- Other non-error or mistake, for example, approval of tax exemption under Promotion of Investment Act 1986.

What is the conditions for application?

The conditions under Section 131 and Section 131(A) of ITA are:

1. To take note that the application will not be considered if the ITRF is in accordance with known stand, rules and practices the DGIR prevailing at the time when the assessment is made.

o Example of the known stand, rules and practices are private ruling or advances ruling, guidelines by IRB, case law and any other written evidence.

2. Taxpayer must pay all the taxes for the relevant year of assessment.

3. Taxpayer must make an application within the time frames after the year assessment.

What are the time frames for the application?

The application for the relief can be made within the following time frames:

i. Within 5 years after the end of the year:

o The errors or mistakes found after the end of the year of assessment in which the assessment is deemed.

o Approval of any exemption, relief, remission, allowance or deduction is granted after year assessment in which the ITRF is furnished; or

o Deduction is granted under ITA or written law gazetted after the ITRF is furnished;

ii. Within 1-year after the end of the year:

o Deduction on expenses is allowed after the payment of withholding tax and related increased taxes.

How to apply for relief?

Taxpayers can make an application for relief by a letter or Form CP15C by stating the reason in detail relating to the application.

Sources:

Public Ruling 7/2020 Appeal Against An Assessment And Application For Relief

https://phl.hasil.gov.my/pdf/pdfam/PR_07_2020.pdf

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

(Latest update) Withholding Tax on Payments to Agents

(Latest update) Withholding Tax on Payments to Agents

With effect from Jan. 1, 2022, a 2% withholding tax (WHT) will be imposed on monetary payments made by companies to their authorized agents, dealers or distributors, arising from sales, transactions or schemes carried out by the Agents.

A new Section 107D of the Income Tax Act 1967 (ITA) was introduced under the Finance Bill 2021 following the Budget 2022 announcement on 29 October 2021.

The WHT is applicable on in-scope payments made to resident agents, dealers or distributors who are individual residents and who have received more than RM100,000 of such payments in monetary form and/or non-monetary form from the same company in the immediately preceding year of assessment (YA)

The tax withheld is to be remitted to the lRBM within 30 days from date of payment or crediting the payment to the agent, dealer or distributor.

Companies which fail to comply with this requirement will be subject to an increase in tax equivalent to 10% of the outstanding WHT and the underlying gross expenses which are subject to the WHT would be denied a tax deduction

Key salient points from IRB Response to Chartered Tax Institute of Malaysia Comments on 15/4/2022

1. LLPs are excluded from the definition of a payer company.

2. The definition of “Cash” includes transactions via payment vouchers, prepaid credit and e-wallets.

3. The WHT is applicable on the amount before the any contra transactions are made. Hence, the earlier comment in the FAQ that credit notes are excluded from the WHT.

4. Section 107D is applicable on ADD who receive the commissions based on the achievement of sales or services rendered for the payer company.

5. The WHT is not applicable to the payer company’s staff who are ADD if the commission is subjected and the commission is reported in the Form EA.

6. Out-of-pocket expenses incurred by the ADD have to be specifically identified in advance. If the expenses arise from sales, transactions or schemes carried out, then the WHT is applicable on the out-of-pocket expenses.

Source

IRBM has issued a Frequently Asked Questions (FAQ) dated 28 February 2022 (only available in Bahasa Malaysia) on the application of the above Section 107D.

https://phl.hasil.gov.my/pdf/pdfam/Soalan_Lazim_Seksyen_107D_ACP_1967.pdf

Reference :

Read our past posting on withholding tax on payment to agents in our blog

1. Withholding Tax on Payments to Agents dated on 17.03.2022

https://bit.ly/3L3JzOB

2. 2% withholding tax on commission dated on 30.12.2021

https://bit.ly/3hRrk20

3. 预算案 2022 dated 19.11.2021

https://bit.ly/3tKU7dM

4. Budget 2022 - SME edition dated on 18.11.2021

https://bit.ly/3IWhAiR

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Bookkeeping, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource bookkeeping, and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

没有资格获得退税2%的补偿

没有资格获得退税2%的补偿

-

根据 ITA 在到期日之后提交的纳税申报表

-

根据 ITA 第 110 条抵销的税款超过应缴税款

-

IRB 根据 ITA 第 90(3)、91、91A、92 和 96A 条提出的评估。

-

纳税人申请延长报税时间。

-

有人对评估提出上诉

-

在提交截止日期后的 90 或 120 天内,IRB 审计需要缴纳额外的税款

-

支付的超额税款不是根据 ITA 第 107,107B 和 107C 条分期付款

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

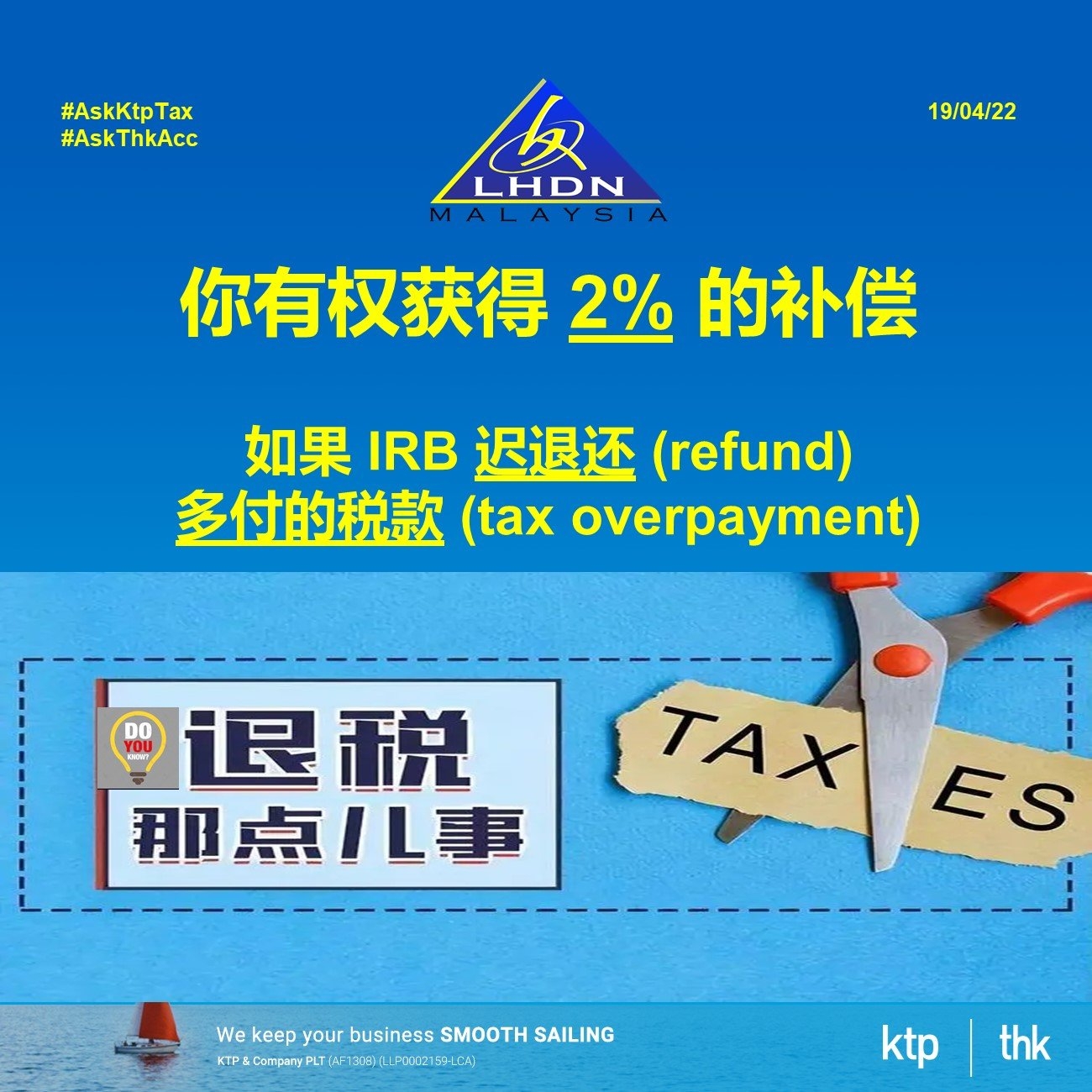

退税2%的补偿

退税2%的补偿

你有权获得 2% 的补偿. 如果 IRB 迟退还 (refund) 多付的税款 (tax overpayment)

Terms & Conditions :

1. 在截止日期前提交所得税申报表. 所得税申报表必须按时,完整和正确提交.

2. 可退税的纳税类型

-

PCB:每月减税

-

CP500:分期付款通知书

-

CP204/CP205:估计公司/有限责任合伙企业/社会应缴税款

计算公式

2%的赔偿金按照以下公式支付:

𝑻𝒂𝒙 𝒓𝒆𝒇𝒖𝒏𝒅 × (𝑻𝒐𝒕𝒂𝒍 𝒏𝒐.𝒐𝒇 𝒅𝒂𝒚𝒔 𝒍𝒂𝒕𝒆 )/(𝟑𝟔𝟓 𝒅𝒂𝒚𝒔 ) × 2%

-

通过电子填写, 自提交截止日期起 90 天后赔偿计算时间计算

-

通过邮寄/快递,自提交截止日期起 120 天后 赔偿计算时间计算

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

Tax Responsibility of Employer

Tax Responsibility of Employer

Overview

As an employer, are you aware of the responsibilities and deadlines you have to adhere to? To make sure that you do not miss the deadline, here is the summary to help you.

Key takeaways:

You will understand the responsibility and consequences as follows: --

1. Who is the employer?

2. What are the employer’s responsibilities?

3. What are the consequences of failing to comply?

Summary of learning

1. Who is the employer?

- The employer has included Company, Limited Liability Partnership, Partnership, Enterprise and etc.

2. What are the employer’s responsibilities?

a) Register an Employer’s number (E)

The E number can be registered through https://edaftar.hasil.gov.my/.

b) Monthly Tax Deduction (MTD)

The MTD must be calculated based on the employee’s monthly remuneration and remitted to IRBM on or before the 15th of the subsequent month.

c) Employee’s Statement of Remuneration (Form EA)

Form EA has to be prepared and provided to employees on or before the last day of February of the following year.

d) Return Form of Employer (Form E)

Complete and submit the Form E with C.P.8D on or before 31 March of the following year via e-Filing.

e) Notification of New Employee (CP22)

To notify IRBM who is or is likely to be chargeable to tax within 30days after commencement of employment and submitted to any IRBM office.

f) Notification of cessation of employment or cessation by reason of death for an employee in private section (CP22A)

To notify IRBM who is or is likely to be chargeable to tax not less than 30days before the cessation of employment and submitted online via e-SPC or at IRBM office which handles the employee income tax number.

g) Notification of cessation of employment or cessation by reason of death for an employee in the public sector (CP22B)

To notify IRBM who is or is likely to be chargeable to tax not more than 30days after being informed of the death and submitted online via e-SPC or at IRBM office which handles the employee income tax number.

h) Notification of employee leaving Malaysia for more than 3 months (CP21)

To notify IRBM who is chargeable to tax not less than 30days before the expected date of departure and submitted online via e-SPC or at IRBM office which handles the employee income tax number.

i) Statement of monetary & non-monetary incentive payment to an agent, dealer or distributor pursuant to Section 83A of the Income Tax Act 1967 (CP58)

- To prepare the CP58 for its agents, dealers, and distributors.

- To render the CP58 by 31 March of the following year to its agents, dealers, and distributors, if the amount of incentive (monetary and non-monetary) exceeds RM5,000 during the calendar year.

- If LHDN requests for a listing of CP58 information, the employer shall include all information of the agent, dealer or distributor even if the amount is below RM5,000.

j) Withholding Tax (WHT) on Payments to agent, dealer or distributor

Effective from 1 January 2022, the 2% WHT will be imposed on monetary payments made by companies to their authorized agents, dealers or distributors, arising from sales, transactions or schemes carried out by the Agents.

3. What are the consequences of failing to comply?

a) Failure to furnish a Return Form

- Shall be liable to a fine of RM200 - RM20,000 or imprisonment for a term not exceeding six months of both.

b) Late payment

- 10% shall be imposed on the amount unpaid without any further notice.

Sources

Employer Responsibility

https://www.hasil.gov.my/en/employers/responsibility-of-employer/

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

What is the tax treatment for the income received by medical practitioners (Specialist Doctors)?

What is the tax treatment for the income received by medical practitioners (Specialist Doctors)?

IRB has produced a guideline on tax treatment for specialist doctors again.

Summarised below are the key salient points :

Case study 1

A specialist doctor with a Sdn Bhd has an agreement with a private hospital.

- Doctor has received consultation fees from the hospital.

- Patient was referred by the private hospital and paid to the hospital directly.

- Facilities in the private hospital have been used during medical treatment.

Tax treatment: The consultation fee received shall be reported under S4(a) of ITA 1967 as individual business income.

Case study 2

A specialist doctor with a Sdn Bhd has been involved in consultation services and medical-related fields (i.e. medical goods trading, pharmaceuticals, and health aids).

Tax treatment: As there are two types of income, it shall be declared with separated sources of income.

a) The consultation fee received shall be reported under S4(a) of ITA 1967 as individual business income.

b) The medical goods trading income shall be reported under S4(a) of ITA 1967 as individual or company business income.

*** Form B: S4(a) of ITA 1967 as individual business income

*** Form C: S4(a) of ITA 1967 as company business income

Case study 3

A specialist doctor with a Sdn Bhd owns a clinic in a private hospital.

- Patient visits the clinic directly without any referral by the private hospital.

- No facilities in the private hospital are being used during medical treatment.

Tax treatment: The consultation fee received shall be reported under S4(a) of ITA 1967 as company business income.

Case study 4

A specialist doctor under an employment contract with a private hospital.

- Doctor has received director remuneration from the hospital.

Tax treatment: The director remuneration received shall be reported under S4(b) of ITA 1967 as employment income.

Expenses can be claimed against S4(a) business income of ITA 1967

Condition: The expenses incurred are wholly and exclusively in the production of gross income.

Example for expenses:

-

Professional indemnity insurance

-

Seminars, workshops or conferences approved by CPD Review Committee

-

Rental of equipment/ operating room in a private hospital

-

Medical practitioner license and etc.

Capital allowance can be claimed against S4(a) business income of ITA 1967

Persons Eligible to Claim Capital Allowances

-

A person who is carrying on a business;

-

Has incurred capital expenditure on an asset for the business;

-

The asset is used for business purposes.

Source:

Garis Panduan Layanan Cukai Ke Atas Pendapatan Pengamal Perubatan (Doktor Pakar) Di Hospital Swasta Sama Ada Ditaksir Di Bawah Individu Atau Syarikat

https://bit.ly/37bHJfQ

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

Tax clearance Malaysia LHDN

Tax clearance Malaysia LHDN

Latest tax audit operasi

IRB has initiated tax audit on the following

1. CP21 - Notification by Employer on Employee's departure from Malaysia

http://phl.hasil.gov.my/pdf/pdfborang/CP21_Pin.1_2021.pdf

2. CP22 - Notification of New Employee

http://phl.hasil.gov.my/pdf/pdfborang/CP22_Pin.1_2021.pdf

3. CP22A - Notification of Cessation of Employment

http://phl.hasil.gov.my/pdf/pdfborang/CP22A_Pin.1_2021.pdf

Penalty on non-compliance on CP21, CP22 & CP22A

Delay in submitting the application for tax clearance may be subjected to penalty. The penalty will be in the form of fines between MYR 200 and MYR 20,000 and imprisonment for up to six months.

LHDN may take legal action against the employer who fails to pay the outstanding tax as per the Tax Clearance Letter.

How to submit CP21 + CP 22A online via IRB e-SPC.

STEP 1: Go to LHDN Website: https://ez.hasil.gov.my (网站)~ Key in New IC number

STEP 2: Key in password

STEP 3: Select e-SPC

STEP 4: Key in Employer’s number

STEP 5: Select Form and Key in accordingly

-

CP22A – Private (私人公司)

-

CP22B – Government (政府)

-

CP21 – Foreign Leaver (外国人)

STEP 7: Select Log Out

What documents IRB ask for?

Basically these are the documents required in a typical tax audit on employer on CP21, CP22 & CP22A :

•Staff listing

•Form E – Return of C.P.8D

•Form 22

•Form 21

•Form 22A

•Payroll System Data

•Latest of Form 9, 24,49 and 13

•Borang D(Kaedah 13)and Borang A(Maklumat Perniagaan)

•Form EA/EC

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks

New e-Telegraphic Transfer (e-TT) System for Tax Payments

New e-Telegraphic Transfer (e-TT) System for Tax Payments

Following the Inland Revenue Board (“IRBM”)’s media release on 3 March 2022, the IRBM has rolled out the new e-TT system which will generate a unique Virtual Account Number (VA) as a payment identification.

This will assist the IRBM to trace the electronic transfer of funds by taxpayers to its accounts and identifying the taxpayers.

Effective from 1 April 2022, taxpayers who wish to make payments through Telegraphic Transfer, Electronic Funds Transfer and Interbank Giro from within and outside Malaysia, are required to obtain a Virtual Account Number.

Key summary of the new e-TT system for tax payment

1. Virtual Account (VA) number is required as a payment identification identity from IRBM for tax payment with effect from 1st April 2022.

2. Taxpayer will receive the e-TT notification in your email from IRBM.

3. Each VA number is limited to one transaction.

4. In case of withholding tax (WHT) payment, do remember to email the FULL documents to WHToperasi@hasil.gov.my on the day of payment.

5. & more

Type of tax payments

The Virtual Account Number generated under the e-TT system caters for the following types of taxes:-

(i) Income tax

(ii) Withholding tax

(iii) Petroleum income tax

(iv) Compound

(v) Public entertainer

(vi) Real Property Gains Tax – Section 21B retention sum payment

Each Virtual Account Number can only be used for one transaction.

Withholding Tax Payment operational issues

In case of WHT payment, do remember to email the FULL documents to WHToperasi@hasil.gov.my on the day of payment.

Full documents :

-

Completed CP tax payment form

-

Invoice

-

Proof of payment

-

Virtual Account No.

Source

1.Read the media release from IRBM on e-TT

Click https://bit.ly/37ptnID

2.How to generate a Virtual Account Number (VA) as a payment identification identity from IRBM?

Click https://bit.ly/3JhHe0K

Visit Us

-

Wisma KTP, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma THK, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

An approved audit firm and licensed tax firm operating under the KTP group based in Johor Bahru providing audit, tax planning, advisory and compliance services to clients

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

THK (Secretarial, Account, Payroll, Advisory)

A licensed secretarial firm in Johor Bahru providing fast reliable incorporation, secretarial services, corporate compliance services, outsource booking, accounting and payroll services to clients

-

Website www.thks.com.my

-

Facebook https://bit.ly/3nQ98rs

KTP Lifestyle

An internal community for our colleagues on work and leisure.

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

KTP Career

An external job community on vacancy in Johor Bahru for interns, graduates & experienced candidates.

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

#Ktp #Thks