Blog

���ʦ��ǰ;��?

���ʦ��ǰ;��? ���������ձ����б������ʦ����������ȡ��?

����ͬ�ⱨֽ����...רҵ���ʦ���Dz���Ա.

���� technical ֪ʶ�������� soft skill ����������Ҳ����Ҫ.

��ס..�ɵ�ͼ��Զ�Ҳ���������. ��ԶҪ���� lifelong learning. #staystrong

�����������Ϊ�б��ϵ���ҵ֮һ�����Բ��ټҳ�����������ӿ�ȡרҵ���ʦ�ʸ�. Ȼ���������˹����ܿƼ�Խ�����죬���ʦҲ��˱�Ԥ����δ�����п��ܸ�����ȡ��.

��Թ�ҵ4.0��Ϯ���������ľ�ҵ���Ƿ�����Ӱ�죿

�����Ǿ��úûõ�ʱ����Ҫ�������ʦ��Э����ҵ������������跢չ����. �κ������������ʦ��һ������.

Now…ֻ�����������������ʲ��ߣ����Կ�ȱ���࣬���²��ֱ�ҵ���ڻ�ȡ�����ϻ���Щ������

����˲��ָþ߱������ļ��ܣ���Ӧ�������˲Ϣ��䣿

��ס…רҵ���ʦ���Dz���Ա.

רҵ���ʦ�����п��ܳ�Ϊ��ϯ����Ա����ϯִ��Ա����Ҫ��ְ����Э����ҵ��������������ӯ����ҵ��չ�����Ǹ����������ϡ�

���� technical ֪ʶ�������� soft skill����������Ҳ����Ҫ.

-

��ͨ������Ӣ�������������뷨����.

-

���Լ��ܼ��������ֹ���..

-

���ܸı��Ԥ֪���Ƶ�����.

-

������˼��, ������, ս�Ժͷ������� & ս�Ժͷ�������

Source :

�����ձ� 12/07/21 ���ʦ����������ȡ��?

https://www.sinchew.com.my/content/content_2510414.html

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

Extension of time for submission of SST return and payment of tax due on 30 June 2021

RMC announcement -Extension of time for submission of return and payment of tax due on 30 June 2021

The Royal Malaysian Customs Department (RMC) has recently allowed extension of time until 31 July 2021 for submission of SST-02 form and payment of SST to SST registered persons/manufacturers affected by the MCO 3.0.

The extension of time for submission of SST-02 form and payment of SST is done by waiving the penalties arising from the late submission of SST-02 form and payment of SST.

Registered persons/manufacturers who are late in the submission of their SST-02 returns and payment of SST due to the MCO3.0 can now apply to their respective zone/state RMCD offices for waiver of penalties on the late submission returns and payment SST.

In other words, the waiver of penalties require application in writing to RMC.

It is not automatic given to register persons/manufacturers.

Source

RMC announcement on 9/7/21

http://www.mysst.customs.gov.my/assets/document/Annoucement/Penghantaran%20dan%20pembayaran%20CJ%20dan%20CP%20bagi%20tempoh%20bercukai%20April%20Mei.pdf

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

��δ��� �⼮Ա��

Stamp duty for transfer of shares Malaysia

Stamp duty for transfer of shares Malaysia

Section 105(1) of the Companies Act 2016 required any shareholder or debenture holder may transfer all or any of his shares or debentures in the company by a duly executed and stamped instrument of transfer and shall lodge the transfer with the company.

What is IRB’s STAMPS?

Stamps is an Electronic Stamp Duty Assessment and Payment System via internet.

STAMPS will be replacing the manual franking system in LHDNM’s counter with effect from 01/07/2021.

Who can register for STAMPS ?

1. Company

2. Agent (Lawyer, Real-properties Agent, etc)

Stamp duty computation

According to the item 32(b) First Schedule of Stamp Act 1949:

“On sale of any stock, shares or marketable securities, to be computed on the price or value thereof on the date of transfer, whichever is the greater –

For every RM1,000 or fractional part of RM1,000 RM3.00

Method #1 – Net Tangible Asset (NTA)

Formula:

= Total Asset – Intangible Asset – Total Liability

NTA per share

= NTA / Number of shares issued

Method #2 – Consideration

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

����˰�ؿ�

Auditor ���������Ĵ���� ... �ϰ�˵�����ѽ�

�ϰ�����˵�µ�����˾ got ����˰�ؿ� (Tax Rebate) RM20,000 x 3��! �ϰ������������һ���е�ͨ! ���� double entry !

KTP �������µ�����˾����˰�ؿ�

https://www.facebook.com/512614135447552/posts/4707812805927643/

KTP Ӣ�İ���µ�����˾����˰�ؿ�

https://www.facebook.com/512614135447552/posts/4707820429260214/

Auditor ���������Ĵ���� �ռ���

https://www.facebook.com/512614135447552/posts/5750415295000717/

KTP auditor ���� ��� auditor �ռ���

https://www.facebook.com/512614135447552/posts/5755618914480355/

PS : ������ͬ �����ɺ�

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

Casual worker vs Part-timers

Casual worker vs Part-timers

How to identify “Part-Timers”?

Whose average working hours between 30% -70% of the normal working hours per week of full time employees.

How to identify “casual worker”?

Whose average working hours not more than 30% of the normal working hours per week of full time employees.

Part-Timer

• Governs by employment laws - Employment (Part-Time Employees) Regulations 2010

• Perform works in business premises

• Entitles Annual Leave & Sick Leave

• Wages subject to EPF, SOCSO, EIS & PCB

Casual Worker

• Does not govern by employment laws

• Perform works at their own home / business premises

• Does not entitle Annual Leave & Sick Leave.

• Wages do not subject to EPF, SOCSO, EIS & PCB

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

��Ҫ�������� ?

��������ǣ��������ݹ���������ְ?

����ְһ�乫˾��ֻ�Ǿ����ϰ岻�Ǻܺá��ϰ�칫�ҵ�һ�ж��dz��ϸ�.

-

�������˾?

-

�����뿪��˾?

-

Ϊʲô�Է�����5����?

-

Ϊʲô�ϲ�����ô���?

-

Ϊʲô��˾�� Milo ���������?

-

Ϊʲô�˷������� papers?

Anyway �����ұ� ҵ���1�ݹ���, ������Թ loh..

ֻ��������ֵ�����, ����Ķ���˳��....WFH ���˳���һ����, û��û��, ѹ���ܴ�.

�ϰ�ǰ�����ҽԺ, �Դ�����, Loh ���. ��ȥҽԺ֮ǰ, �ϰ��н� HR �� Memo. ���ߴ�Ҳ�Ҫ����.

�����Һܽ���, ������Ϊ�ϰ��ҽԺ.

������̫�� casesҪ�ϰ���. ������̫������Ҫ�ϰ�ָʾ. �ϰ岻֪�������� Peak Period ��?

Senior �����, Manager ���Ǹ�. ��! ��ĺ���! С����ʲôҲ����! �ܶ�ʱ�� follow last year! ���� follow ��˾ sop! �����ޱȵ�ʹ��.

���˼���, �ϰ��ֳ� Memo. �ϰ�˵�����ȶ�������Ժ. ��˵8��1�Ųſ��� staff meeting.

������乫˾���� ? ������乫˾��ǰ;�� ?ֻ�Ǿ����ϰ岻�������� !

��Ҫ�������� ?

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

deferment of tax instalment payment under Pemulih

IRB has issued an updated FAQ on Deferment of Tax Instalment Payment under PEMERKASA dated 28 June 2021.

The updated FAQ to allow companies which are not in the tourism sector to also apply for deferment of instalment payments.

The FAQs refer to the application for deferment of CP204 (a monthly instalment of tax estimates) and CP500 (bi-monthly instalments for individuals) for taxpayers whose business codes fall outside of the specified business codes which relate to tourism.

Taxpayers which businesses are affected, may submit an application for deferment to the IRB, supported with the relevant documents to:

-

cp204pemerkasa@hasil.gov.my for applications for deferment of CP204 instalment payments for the months of April 2021 to December 2021

-

cp500pemerkasa@hasil.gov.my or to the IRB branch handling the case, for applications for deferment of CP500 instalment payments for the months of May, July, September and November 2021.

-

Or talk to us if we are your tax agent

Applications will be considered based on the merits of each case.

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

MTD as final tax LHDN

Key takeaway

You will understand:

1. What is Monthly Tax Deduction (MTD)?

2. Who is eligible to treat MTD as Final Tax?

3. What is the requirement?

4. Any application needed?

5. What is the consequence of non-compliance?

Summary of learning

1. What is Monthly Tax Deduction (MTD)?

Monthly tax deduction is also known as “Potongan Cukai Bulanan (PCB)”.

This is a deduction mechanism for employer to deduct the employee's monthly remuneration for the purpose of paying the employee's income tax.

2. Who is eligible to treat MTD as Final Tax?

Taxpayers who have employment income only and MTD has been deducted are given an option for not to submit the Income Tax Return Form (ITRF) via e-Filing or manually.

3. What is the requirement?

· There is only employment income received in the current year including any previous year’s employment income.

· Served with the same employer.

· Taxes are not borne by the employer.

· Husband or wife does not make the choice to be assessed jointly under Section 45 of the Income Tax Act 1967.

· MTD is deducted in accordance with the Income Tax (Deduction From Remuneration) Rules 1994 and included Benefit in Kind(BIK) and Value of Living Accommodation (VOLA).

4. Any application needed?

Taxpayer who meets the requirements and does not submit the ITRF after the due date:-

· will be deemed to choose not to file the ITRF

· the MTD will be deducted against the tax payable for the year of assessment

· no tax refund can be claimed if there is any excess of tax paid in his MTD

5. What is the consequence of non-compliance?

The Director General of Inland Revenue (DGIR) retains the power to disregard the total amount of MTD deducted as the final tax payable and raise a deemed assessment or an additional assessment penalty as followings: -

· Imposed the penalty under subsection 112(3) of the Income Tax Act 1967

· Raise an estimated assessment under Subsection 90(3) of the Income Tax Act 1967

Sources

Layanan Cukai Ke Atas Cukai Muktamad - http://phl.hasil.gov.my/pdf/pdfam/NA_1_2021.pdf

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

��������-��˰���� 3

��˰���� - �ռ��� 2021

Read the full story in our blog

https://www.ktp.com.my/blog/tax-deadline-extension-2021-chinese/27june2021

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

Tax extension 2021

Extension of time (EOT) for tax filing and payment

Inland Revenue Board Malaysia (“IRBM”) has updated the 2021 Return Form Filing Programme on 26 June 2021.

A 2-month grace period has been given for the submission of the tax returns for the following group of taxpayers:-

Personal tax

For the submission of Forms B, P, BT, M, MT, TF, TP and TJ (individuals, partnerships, associations, deceased persons’ estate and Hindu Joint Families who carry on business) as well as for the payment of the balance of tax payable (if any) for the year of assessment (“YA”) 2020 :

Statutory deadline : 31/06/21

Extended deadline : 31/08/21

Company tax

For the submission of Forms C, C1, PT, TC, TA, TR and TN (companies, cooperative societies, limited liability partnerships and trust bodies) as well as for the payment of balance of tax payable (if any) for the accounting periods ending 1 October 2020 to 31 January 2021

Kindly refer to the below for the extended deadline.

Source :

IRB anncoucement http://phl.hasil.gov.my/pdf/pdfam/ProgramMemfailBN_2021_Pin.3_2.pdf

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

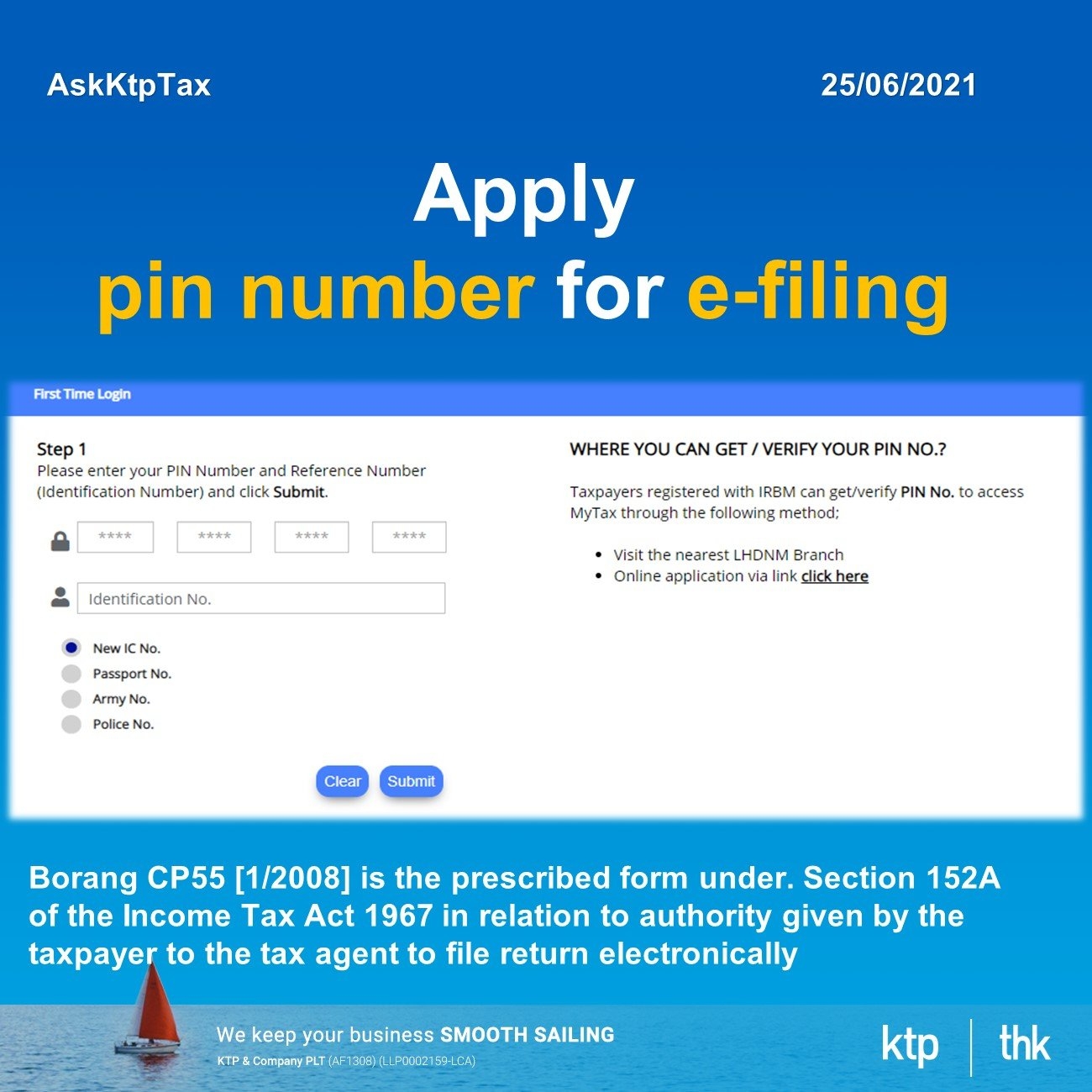

LHDN E-Pin Application

How to apply pin number for e-filing?

Step 1:

Visit LHDN customer feedback via https://maklumbalaspelanggan.hasil.gov.my/MaklumBalas/en-US/

Step 2:

Select “Application”

Step 3:

Download the form

-CP55D for individual registration

-CP55B for organization registration

Step 4:

Click “Next”

Step 5:

Fill in the information required:

a) Sender information

b) Taxpayer information

Step 6:

a) Fill in the info at “Feedback category”

b) Upload CP55D (individual) or Upload CP55B (organization)

Step 7:

Click “Submit”

Step 8:

Receive “Submission Number”

Step 9:

Check the “feedback status” with the submission no. and NRIC after 7 working days

Step 10:

Received the “No.Pin e-Filing” by email

Step 11:

Select the link and Click “Log kali Pertama” https://ez.hasil.gov.my/ci/Login.aspx?page=14

Step 12:

Fill in the “No Pin e-Filing” and NRIC No.

Step 13:

Click “Hantar” and you will need to reset your own “password”

You can log in to LHDN website through your password now!!

Source:

Applying for the e-Filing pin number http://lampiran1.hasil.gov.my/pdf/pdfam/TatacaraPermohonanNoPineFiling_2.pdf

User Manual No. Pin Application & First Time Login https://ez.hasil.gov.my/ci/Panduan/PanduanCI_PermohonanNoPIN_e%20V1.2.pdf

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

How to amend tax return submitted

Overview

Taxpayers are allowed to make amendment on the information or assessment for the submitted Tax Return Form(TRF) under Section 77B of the Income Tax Act 1967 (ITA 1967) or Section 30B of Petroleum (Income Tax) Act 1967 (PITA 1967) by using the Amended Return Form (ARF).

Key takeaway

You will understand:

-

Rules of submission

-

Terms for submission

-

Rate of increase in tax

-

Method of submission

Summary of learning

Taxpayers are allowed to make amendment when there is:

-

Understate of income / unreported income

-

Expenses over claimed

-

Capital allowances / incentives/ relief over claimed

The amendment limit to once for a year of assessment.

The amendment is disallowed if the Director General of Inland Revenue (DGIR) has made amended assessment for the submitted TRF.

What are the terms for submission ARF?

ARF must be submitted within 6 months from the due date of TRF

A duly completed ARF must state:

-

the amount / additional amount of chargeable income

-

the additional tax payables

-

the amount of tax payable on the tax which has or would have been wrongly repaid;

-

the increased sum ascertained in accordance with subsection 77B (4) of ITA 1967 or subsection 30B(4) of ITA 1967;

-

other contains required by the DGIR.

What is the rate of increase in tax?

The additional tax payable amount in ARF is subject to an increase in tax of 10%.

The formula = the amount of such tax payable or additional tax payable x 10%.

The total tax payable amount must be paid at the same date of ARF is submitted.

What are the methods for submission ARF?

ARF can be submitted in the following ways:

-

Online e-filing (only for corporate taxpayer: Form C)

To visit https://mytax.hasil.gov.my > click e-Filing > click e-Form > choose e-BNT C

-

Manual filing

- download ARF on Lembaga Hasil Dalam Negeri (LHDN) website:

To visit http://www.hasil.gov.my > Forms > Download Forms (in Malay Version) > Handle the completed ARF to LHDN branch

Sources

GPHDN 1/2020: - Procedure on submission of Amended Return Form

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

������Ϸ������� : �������KTP �빤������� ACCA

������Ϸ������� : �������KTP �빤������� ACCA Բ������ with 100%.

����� ��6��23��

ʱ�� ��11.15am to 12.15pm

�ص� ��𝐙𝐎𝐎𝐌 ����ѧϰ

�ۿ�������Ƶ������ KTP �� Youtube Ƶ����

�ܰ��� 60 ��������ѧϰ with our speaker Ms. Cyma & Mr. Arthur Yong. ���Ǽ������� :

• Ϊʲôѡ��ACCA��

• ��ACCA �γ̵�Ŀ����ʲô��

• ʲô������ʹ��Ҫ�� ACCA?

• �㻨�˶���ʱ������� ACCA�γ̣�

• ��һ�� ACCA ��Ŀ����Ϊ��ֵģ�

• ���y�� paper ����һ�������N������

• ÿ�츴ϰ����Сʱ��

• �����������ڿ���ǰ���������Ч�ĸ�ϰ��

• ������������ξ���Ҫ�������� optional paper ����(p4 -p7)��

• ��������������ڿ���ʧ����������������ȥ���أ�

• ������ʲô������־�������Dz����� ACCA ����fail�˼���?

• ���ʿ���ʧ��֮�����м��� register �γ� / revision class �������ѡ���Լ���ϰ֮���ٱ��������أ���

• ����ô������빤�����ʱ�䣿

• ��ι���������ѧϰ֮���ѹ����

• ������������ ACCA�����а�����

• ��� ACCA �γ̺���ʲô��ı��Ӱ����

• ACCA ��û�а�������Ĺ���?

• ��Ὠ��߹�����ѧϰ ACCA��

��Ȼ�����ǵ� Moderator ���ϰ�Ҳ���˼������� :

• �ҵ�Ӣ�ﲻ���ҿ���ͨ��ACCA��?

• ����ҵ� ACCA �������ҵ���һ���ж���ʲô?

• ��������ͨ��ACCA�Ƕ��٣�

• KTP û�е�����������ΰ���ѧϰʱ��ģ�

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

������Դ�����Ƴ���һ���ֻ�Ӧ�ó��� APP Working For Workers (WFW)

������Դ�����Ƴ���һ���ֻ�Ӧ�ó��� APP Working For Workers (WFW)

�����Ƴ����APP����Ϊ�˱�����ٽ�����Ա����Ȩ���븣����Ա��һ�������������������Դ�ʱ���ܹ�ֱ����APP�����������(TK)�ٱ�.

Working For Workers (WFW) Ӧ�ó�ʽ����Ա��������Թ�������Υ�����������ɵ���Ϊ������������Ͷ��.

WFW��14��Ͷ����𣬰�������֪ͨ�½�͡���Աн��δ�����н�������������н������١���Ƹ�ͺ�Լ�����١��Ӱ�ѡ���������, ������֧����ͽ�, ���������� 1990 �깤��ס������ʩ���� (The Workers' Minimum Standards of Housing and Amenities Act 1990) ����ͱ�, ���������� 2012 ������������䷨��, �Ƿ��ۼ����ʵȵȣ����ٱ���ѡ��.

Google Play����Apple Store��ѰWFW���APP�����ذ�װ���ܸ��ݲ���ȥ�ٱ�����.

���APP������Ա������ȥ�ٱ�����Ա�ڲ��ص������ֱ�¶�½���Ͷ��.

�����ڽӻ�Ͷ����Ԥ��3��7���ھͻ�����Ͷ��.

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

Ա����ʱ���� report �ϰ� ����ϰ岻����Щ

������ʱ�����ϰ�, ����ϰ岻����Щ HR ��...

��ʵ���������кܶ���ڹ����ķ���, �ϰ����֪�� & ��.

���� Sosco

ǿ����Ҫ���������ᱣ�ջ�������ע��. ΪԱ���Ǽdz�Ϊ���ջ�Ա.����ΪԱ�������ջ������ɱ���.

��ᱣ�ջ��������йع�������500��4000��ķ�������������������߲����ɷ���������Ա����Ϸ�ͥ����������ͥ�ж���������������ÿһ��Ա���������1����Ĵ��֣����ط��������5�������������5��.

���ɾ�ҵ����EIS

��ҵ���ռƻ�����2018��1��1��ʵʩ. Υ��������ᱻ����������5000�����. ������ʱ���壬���������ͥ��������1���� ��������������2�������ʩ���̷���

���ɹ�����EPF

1991���Ա���������43(2)���ģ��÷���涨���й���������ÿ��15�ջ�֮�ɹ�Ա������һ����ɣ����д�������������1����ķ��������ʩ��

������

��2020�꿪ʼ��ȫ��56����Ҫ���е����н��Ϊ1200�.

�����н��(����)�����£�Υ���Ĺ�������ɣ��ɱ��������1���(ÿλ��Ա). ����������Υ�棬����ÿ�տɱ��������1000������⣬�������ٷ�����������������2�������������5��.

�����������ֽ�֧��Ա��нˮ

������������1955��������25A(1)���������Ĺ涨������н�����ͨ�����л�ͷ����Ա���������ֿн����Υ����

���Ҫ���ֽ�н����Ա����ǩ��һ��Ҫ���ֽ�н���Ÿ����������õ�������������ִ�1955��������25A(1)����.

���� HRDF ������Դ��չ����

Human Resource Development Fund (HRDF) �����ʽ���Ա����н�� 0.5-1%. ��Ŀ����Ϊ����������ʱ������ʣ�����һ����Ա��.

Visit us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#valuation

#valuationservices

#IACVS

Effect of voluntary winding up

- Company ceases to carry on business except where liquidator thinks otherwise for the benefit of the winding up.

- Any transfer of shares or alteration of members status is void unless permitted by liquidator.

- Assets of company applied equally in satisfaction of the debts and distributed among the members according to respective right and interest.

- Company shall dissolve after 3 months liquidator submitted the account.

When can you write off a bad debt for tax purposes?

Sad to see so many companies close down with many people are retrenched and unemployed in this pandemic. Is it right?

With the implementation of conditional movement control MCO 3.0, one of the key tax concerns that businesses will face during this period is the tax treatment of bad debts.

This tax question has become increasingly common “Should taxpayers use legal action to recover any debts for tax purposes?”.

Let’s talk about the bad debts written off in a tax perspective :

What is debts

Debts that are allowed as a deduction in ascertaining the adjusted income of a business is a trade debt that is irrecoverable either wholly or partly. Such debt is written off as bad. Trade debt is a debt that arises from the sales of goods or services and has been included in the gross income of the business.

Reasonable consideration under S34(2) of the ITA

Reasonable consideration should be taken before writing off a trade debt as bad and then allowed as a deduction in ascertaining the adjusted income of a business.

Reasonable steps to recover the debt should be taken before any decision is made to write off the debt. Subsection 34(2) of the ITA allows a trade debt which is reasonably estimated to be irrecoverable either wholly or partly, to be deducted from gross income in computing the adjusted income of the business

Inland Revenue Board Malaysia Public Ruling 4/2019 Tax Treatment of Wholly and Partially Irrecoverable Debts & Debt Recovery

Public Ruling No 4/2019 states bad debt is defined as a debt that is considered not recoverable after appropriate steps have been taken to recover it.

Public Ruling No 4/2019 described the basis of writing off a debt as bad and the actions to be taken to recover the debt as well as the evidence to prove such actions have been taken.

Determination Of Bad Debt

The bad debts written off are allowed as deduction, if:

* The debt is a debt that arises from the course of carrying on a business (i.e. trade debt).

* Trade debt shall be included in the gross income prior to the relevant YA.

Circumstances when a debt can be considered as irrecoverable

Debts which are irrecoverable become bad (either wholly or partly) when all reasonable steps have been taken to recover such debt. As long as there are any other reasonable steps for recovery , such debt cannot be written off as bad.

After reasonable steps for recovery as in paragraph 5.3.1 have been taken, a debt can be considered as wholly irrecoverable or bad on the occurrence of any one of the followings:

* Trade debt cannot be recovered.

* The debtor has died

* The debtor is a bankrupt

* The debt is statute-barred

* The debtor cannot be traced despite various attempts

* Any other circumstances where there is no likelihood of cost effective recovery

Reasonable steps have been taken to recover the trade debt:

All reasonable steps based on sound commercial considerations should be taken to recover the debt.

To support a claim for deduction of a bad debt written off for tax purposes, there should be sufficient evidence of such steps taken, including one or more of the following:

* Issuing reminder notices

* Debt restructuring scheme

* Rescheduling of debt settlement

* Negotiation or arbitration of a disputed debt

* Legal action

Visit Us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#irb

#lhdn

Tax case on bad debts write off

Frustrated when IRB adds back your bad debts in a tax audit.

Time is bad, pandemic cause bad debts to rise. Learn IRB official guidelines on bad debt tax treatment.

Why?

Bad debt is always our tax authority focus area. 100% guarantee !

Let’s learn this tax case on IRB fight on bad debts: Quality Concrete Holdings Berhad vs Ketua Pengarah Hasil Dalam Negeri.

In YA 2004, Quality Concrete Holdings Berhad (QCHB) claimed for tax deduction on bad debts of RM608,731.25 (balance of value work done: RM950,000.00). IRB disallowed the deduction on bad debts written off and imposed a penalty under Section 113(2) of the Income Tax Act 1967 (ITA 1967).

IRB argued that:

QCHB did not recognised the value of work done (i.e. RM950,000.00) as gross income for the year of assessment (YA) 1999 up to YA 2004.

Therefore, the deduction of bad debt should be disallowed according to Section 24 and 34 of ITA 1967:

“The amount of the debt shall be treated as gross income of the relevant person from the business

for the relevant period.”

QCHB argue …

The claim amount had been reported under the trade debtors account in the Balance Sheet as at 31.01.1998 for YA 1999.

The claim for the bad debt should be allowable according to Section 24(1)(b) of ITA 1967:

“any services rendered at any time in the course

of carrying on a business.”

QCHB argued it is a trade debt arising in respect of carrying on a business irrespective of where and how the sum of RM950,000.00 was entered and described in the account.

QCHB had acted in good faith and the impugned assessment involved technical interpretation. Thus, penalty should not be imposed.

The decision from the court :

Agreed with IRB tax treatment on deduction of bad debt is disallowed under Section 34(2) of the ITA 1967.

Technical interpretation and good faith are not valid defenses for penalty under Section 113(2) of ITA 1967.

Thus, the penalty imposed under Section 113(2) of ITA 1967 is correct because QHCB had filed an incorrect return and gave incorrect information.

Visit Us

-

Wisma 𝐊𝐓𝐏, 53 Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

-

Wisma 𝐓𝐇𝐊, 41, Jalan Molek 1/8, Taman Molek, 81100 Johor Bahru

KTP (Audit, Tax, Advisory)

-

Website www.ktp.com.my

-

Instagram https://bit.ly/3jZuZuI

-

Linkedin https://bit.ly/3sapf4l

-

Telegram http://bit.ly/3ptmlpn

𝐊𝐓𝐏 𝐋𝐢𝐟𝐞𝐬𝐭𝐲𝐥𝐞 (Our internal community for our colleagues)

-

Tiktok http://bit.ly/3u9LR6Q

-

Youtube http://bit.ly/3ppmjyE

-

Facebook http://bit.ly/3ateoMz

-

Instagram https://bit.ly/3jZpKLo

𝐊𝐓𝐏 𝐂𝐚𝐫𝐞𝐞𝐫 (Our external community for interns, graduates & experienced candidates )

-

Instagram https://bit.ly/3u2PxHg

-

Facebook http://bit.ly/3rPxz9o

𝐓𝐇𝐊 (Secretarial, Account/Payroll, Advisory)

-

Website www.thks.com.my

-

Facebook http://bit.ly/3duvQ5z

We are one-stop (20 years+ history) audit, tax, secretarial, accounting and payroll firms which commit to help and grow our clients business.

#KTP lifestyle

#KTPcareers

#irb

#lhdn